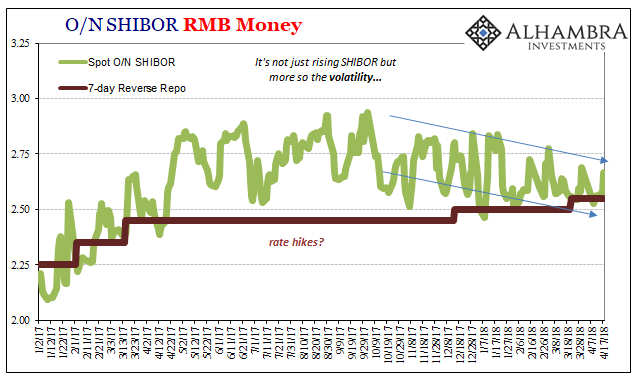

Throughout much of last year, we were told repeatedly that the PBOC was tightening monetary policy. China’s central bank had raised its reverse repo rate twice early on, and then once more last December (and would do so again just last month). These moves coincided with Federal Reserve “rate hikes”, seemingly in line with the whole idea.

Not only that, a “hawkish” PBOC would tend to confirm globally synchronized growth. Shifting stances from the way it had conducted monetary policy during the “rising dollar”, a new directive apparently prioritizing inflation rather than deflation risks is exactly how this central bank would respond to a boom – if it was real.

The narrative, as is usual, contained more inference than evidence. It started with the premise, globally synchronized growth, and then worked backward to find “evidence” of itself. There was never a pickup in Chinese growth, there still isn’t any today, and the PBOC was doing the opposite of tightening particularly later in 2017.

I wrote about these reverse repo theatrics last December under the title Chinese Are Not Tightening, Though They Would Be Thrilled If You Thought That:

It is mere symbolism, which from the Western perspective might seem a bit silly in a “why bother” kind of way, but on that side of the Pacific it is viewed officially as worth the charade so little margin is left in China. For one, PBOC officials know all-too-well that the media will characterize Chinese monetary policy as shifting to, or going further toward, “tightening.” As with both prior “hikes”, the mainstream has dutifully done just that.

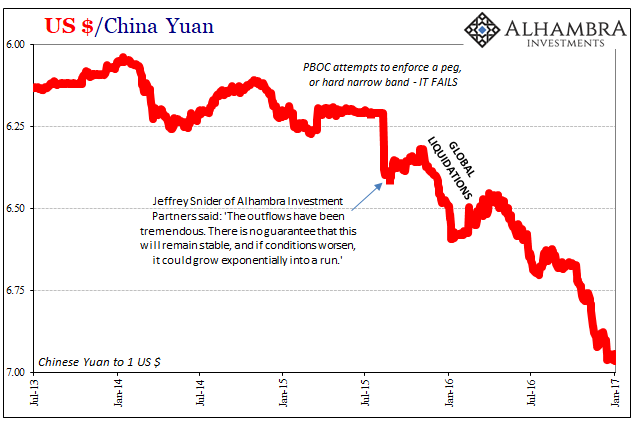

And did so again in March. Contrary to all that, there has been a clear downward bias in RMB markets dating back to last October.

What changed in October isn’t exactly clear, but clear enough. Prior, both secured and unsecured funding were being driven by illiquidity not of the policy rate variety but of the more organic kind owing to bank reserve growth that continues to be hugely constrained. The central bank contrary to the Western narrative began to increase liquidity in those markets. Though it may not seem like it by convention, even the PBOC has to face trade-offs.

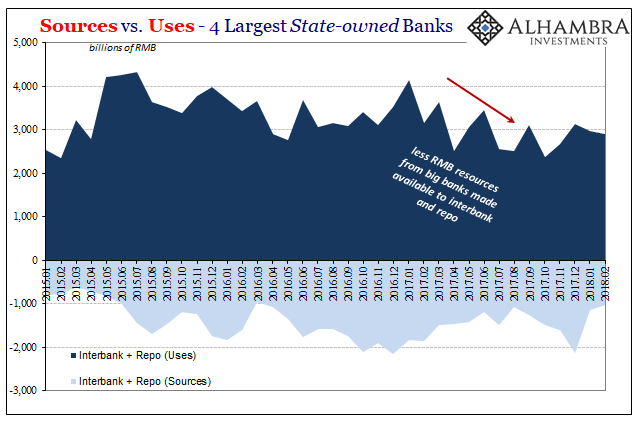

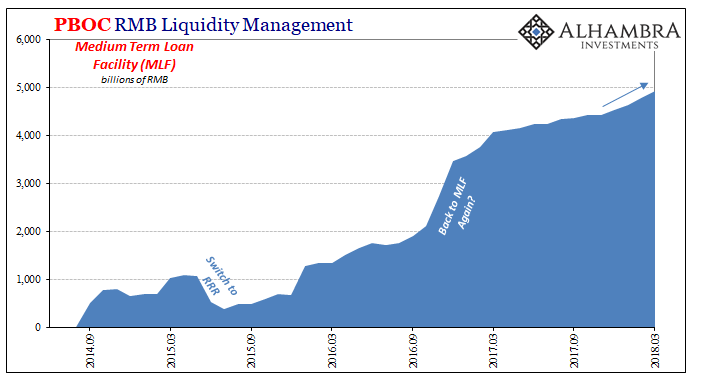

They did not, however, use the MLF to the same degree as they had been doing in 2016. The MLF was meant as a targeted gesture, an intentional funneling of funding into only the largest of Chinese banks. It was believed that rather than flood the system with RMB willy nilly, this targeted approach would be more discerning as China’s biggest institutions would take care in how new funding was productively used in the real economy.

It doesn’t seem to have worked out quite in that way. Instead, the big banks began to hoard liquidity for reasons that also aren’t immediately clear (though we can reasonably speculate). Left out of this “reflation” in RMB were smaller and medium-sized real-economy firms.

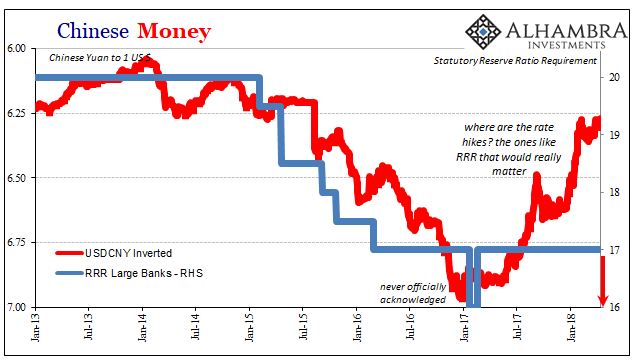

If the PBOC had been serious about tightening, it would have done a whole lot more than raise its reverse repo 5 bps at a time. I also wrote in December, “If economic and financial conditions were really improving, [RRR] is where monetary policy would respond (you know, like every other time in the past).” Today, they did – only not tightening.

Starting next week, the RRR for large firms will be cut by 100 bps. This isn’t going to be an isolated maneuver, however, as the PBOC is ordering those banks to use reserves freed up by the reduction to repay MLF borrowings!

We’ve seen this before, in the middle of 2015. This is different, though, and in several important ways.

At root, I continue to believe, is CNY. Beginning early last year, there was a clear choice made to prioritize the currency over every other consideration. Unlike the media, Chinese officials very early on realized the overriding factor in everything (globally) – the “dollar.” Thus, they knew CNY DOWN = BAD.

But how does one reverse that devastating equation? It’s not an easy thing, as it turns out. Authorities tried several times throughout the “rising dollar” period with little success (as noted last week). As a result, they blew through a huge chunk of so-called reserves and the currency dropped anyway as it became self-reinforcing (a run).

To figure out what to do differently, ask yourself, what is it that made CNY a primary target in eurodollar dysfunction? The answer is always risk; prior to 2013, it was widely believed that though China was racking up debt at an alarming rate it would in the end prove entirely manageable made so by a recovery of pre-crisis growth levels. That’s what really changed in early 2014, the realization that maybe there would be no return to that economic state and therefore financial risks were much more than previously believed.

The result was “outflows.”

To combat this perception of risk is therefore two parts simultaneously. China’s economy needs to be at least stable even if there is no longer any plausible path back to the 2006 economy. Second, the financial system must also be steady so as to buy time in order to try and manage some degree of deleveraging (to stay Japan 1987 rather than have the doomsday debt clock tick far too close to Japan 1989).

The second part is tricky as it almost turns into a loop of circularity; CNY must be stable so that the financial system can be stable so that CNY can be stable. What it means in practice is to reduce all the factors that might be perceived as contributing to its downfall.

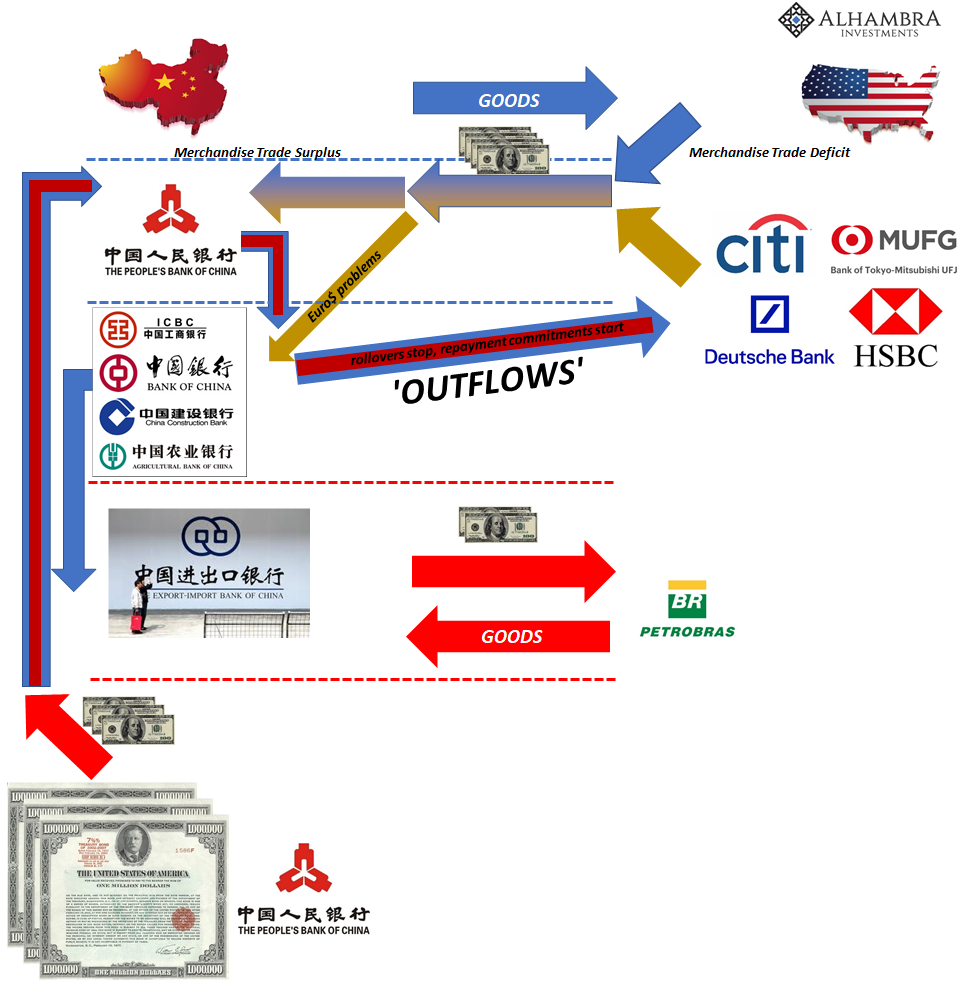

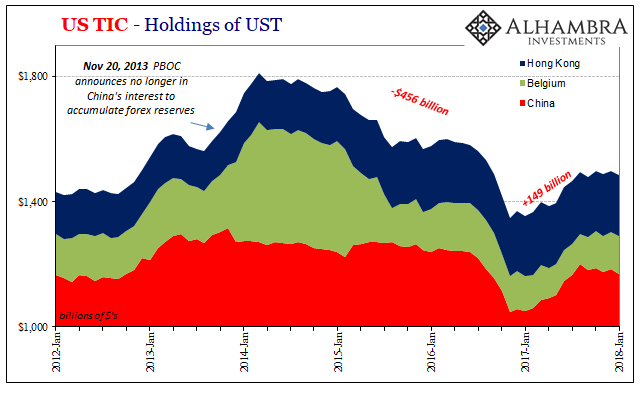

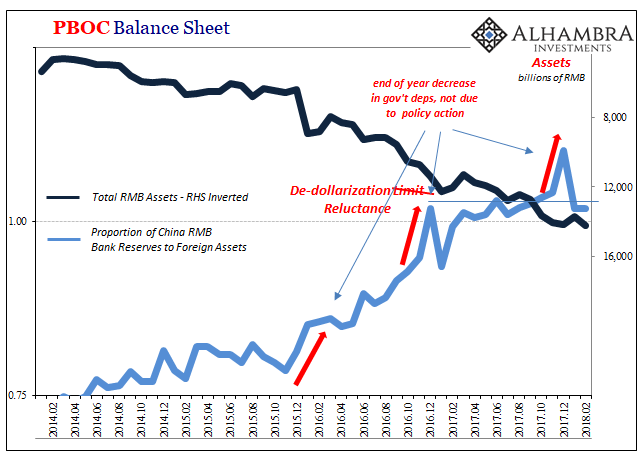

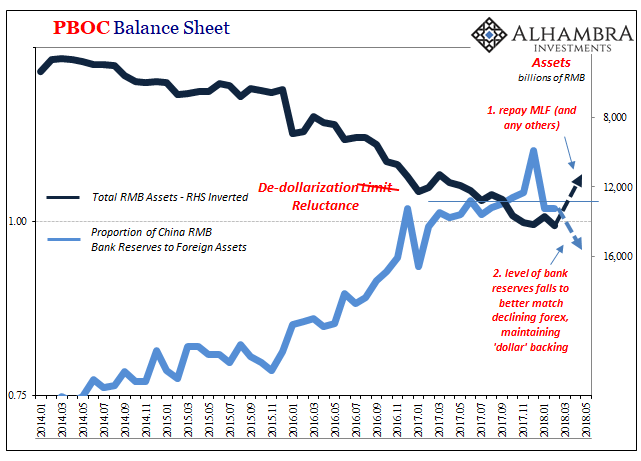

Among them, no more “selling UST’s” as the most visible sign of distress (if possible). Instead, the currency is to be given the rock-solid treatment, which given CNY’s history means continuing its “dollar” backing. De-dollarization is, at this juncture, being judged as too risky of a proposition.

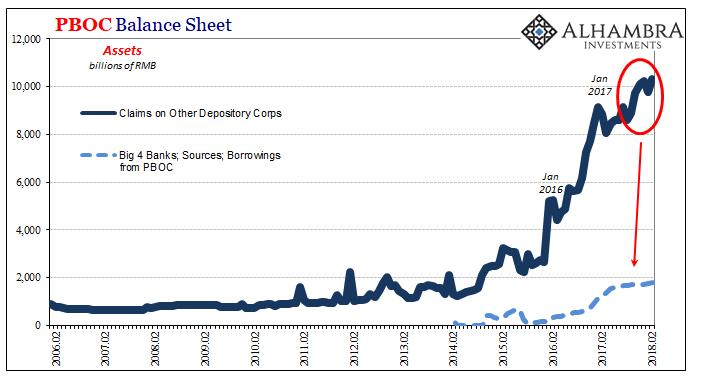

That would mean great(er) attention to the asset side of the PBOC balance sheet which continues to bleed forex “reserves.” In other words, increases in RMB lending to the market via the MLF or anything else absent an actual increase in forex leaves Chinese RMB more and more unbacked on the money side. Unless forex starts to rise again, which appears very unlikely (CNY rose for months, and they still bled), there is only so much the PBOC can do through these RMB windows without breaking what sure looks like an imposed (policy?) limit (shown above).

So, you don’t want to destabilize CNY by leaving RMB (bank reserves) more and more unbacked, so why not then make big banks pay down the MLF? That would create more margin for the central bank to deal with the prospects for further forex drawdowns in the months ahead.

The obvious downside to withdrawing bank reserves is immediate liquidity. To address what would otherwise be an acute shortfall, shift the burden onto large bank private balance sheets by cutting the RRR. They’ve been hoarding it anyway. The central bank reduces its RMB footprint to better align with “dollar” levels, leaving the private banking system to pick up the liquidity slack in a way that doesn’t endanger CNY. Since you just hiked the reverse repo rate for a fourth time last month, it will leave the “experts” wholly confused.

I believe that’s the theory, anyway. It’s a further lesson in how to continue to loosen RMB while making the rest of the world think you’re doing something else (at worst neutral). China has a sustained money problem it cannot by definition fix. Next best thing? Hide it. Why?

There is no recovery coming.

Stay In Touch