One soft indication of how far things have gone is Bloomberg. Six or eight months ago, its newsfeed was filled with uniformly apocalyptic hyperbole over inflation. The tight labor market, according to the Federal Reserve, was going to lead to a faster and farther rate trajectory. Sparked by quickening confidence in the short part of the curve, there was just no way the long end could resist.

Then it did.

Such inflation hysteria has almost entirely subsided. Yield curve flattening will do that. Even those who never pay attention to curves are suddenly gripped by them. One has inverted already (eurodollar futures), at the very least sparking a global conversation rather than BOND ROUT!!!! where no discussion would have been necessary.

For places like Bloomberg, the one-sided hysteria has been replaced by near schizophrenia. Take individual stories whichever way, my view is more of a big data type perspective. They sound much less confident over there these days. Economists and Federal Reserve central bankers can ignore curves at their leisure, but Bloomberg has to cater to people in the markets who might wish they could but in reality cannot.

In other words, unlike for Jay Powell’s assessments there has to be some grounded basis.

Yesterday, they published the familiar kind of story pointing again toward the BOND ROUT!!! It was not uncommon late last year and for several months this year for them to dig up some somewhat familiar financial name from the past and place their optimistic views (on the economy) as if stacking another anecdote onto a fortress of rising nominal interest rates. This recent one pulled Goldman’s dot-com era analyst Abby Joseph Cohen from out of the ether.

Why Cohen? Who knows, except in the common fallacy of appeal to authority. If enough Bill Gross types all say the same thing at the same time then it can’t possibly be wrong. That’s the intentionally simplistic idea, anyway, though like wage inflation it looks more desperate in the absence of actual data. If you can’t find this awesome economic trajectory reflected in market prices (at the long end where it matters), then why not make a bid deal out of Abby Joseph Cohen?

Her message was as simple as it was comfortably conforming:

Goldman Sachs Group Inc. senior investment strategist Abby Joseph Cohen sees pain ahead for bond investors.

Got it. Ignore the flattening yield curve.

Except today Bloomberg reports that some Federal Reserve Branch Presidents are beginning to worry about…the flattening yield curve.

Some Fed regional bank presidents want the central bank to be cautious in raising interest rates to prevent short-term Treasury yields from rising above long-term ones — providing a kind of comfort that Greenspan gave equity investors. Those policy makers argue that such a yield-curve inversion has proven to be a reliable harbinger of past recessions.

Still another of today’s Bloomberg feed professes, however, that the yield curve isn’t even flat. At least when you subtract the “risk premium” from it.

Alarms about the flattening Treasury yield curve are probably overblown, considering how much tamer a move there’s been once risk premiums are stripped out, according to Standard Chartered Plc.

“The adjustment makes the flattening of the yield-curve slope much less dramatic, and shows that it has quite a bit more room to go before it hits the lows of previous cycles,” the bank’s global head of G-10 foreign exchange research, Steven Englander, wrote in a note to clients. More importantly, this version “more or less matches conceptually” what the Federal Reserve looks at with regard to yield-curve indicators, he said.

The last thing anyone should care about is “what the Federal Reserve looks at with regard to yield-curve indicators” given its unimpeachable track record of awfulness in all things related to curves.

The flattening yield curve is making these people do strange things, things they clearly wish they wouldn’t have to. Inflation hysteria is being replaced by curve crazy, especially this last one. The first article is the usual straightforward BOND ROUT!!! stuff. The second is acknowledging the complications of markets that don’t agree it is at all straightforward, but the third is an interesting if ham-fisted attempt to put a positive spin on those complications.

It really is a ridiculous idea, too. If you take out the thing that is causing the yield curve to flatten, risk premium, then the yield curve isn’t really flat. Genius. If we blindfold Captain Smith so that he can’t see any icebergs ahead, the Titanic isn’t in any danger of hitting an iceberg?

This is a small sample (anecdotal, really) of the works being produced by this one media outlet. I think it representative enough anyway, especially as they follow one after another.

On June 17, 2010, one unheard of PhD working before quietly on the staff of the Federal Reserve Bank of Richmond wrote, and published, the following:

So far, I’ve claimed something a bit obnoxious-sounding: that writers who have not taken a year of PhD coursework in a decent economics department (and passed their PhD qualifying exams), cannot meaningfully advance the discussion on economic policy. Taken literally, I am almost certainly wrong. Some of them have great ideas, for sure. But this is irrelevant. The real issue is that there is extremely low likelihood that the speculations of the untrained, on a topic almost pathologically riddled by dynamic considerations and feedback effects, will offer anything new. Moreover, there is a substantial likelihood that it will instead offer something incoherent or misleading. Note also that intelligence is not the issue. Many of those I am telling you not to listen to will more than successfully be able to match wits, in any generalized sense, with me. This is irrelevant. The question is: can they provide you, the reader, with an internally consistent analysis of a dynamic system subject to random shocks populated by thoughtful actors whose collective actions must be rendered feasible? For many questions, I and my colleagues can, and for those that the profession cannot, the blogging crowd probably can’t either.

How’s that working out now eight years, three additional QE’s, and no recovery later? What the good PhD wrote back in 2010 remains the basis for inflation hysteria as well as this curve crazy. As he claims, it does take a lot to obtain a doctorate in Economics, but so what? That doesn’t mean you are an expert in anything other than statistics. It is Economics that is the problem. Mastering its coursework to the most advanced level means nothing other than you’ve mastered its coursework to the most advanced level it offers.

Maybe the blogging crowd can’t answer your questions. Economists, apologies to Dr. Athreya, have proven not only that they can’t, either, but more importantly that they won’t maybe ever.

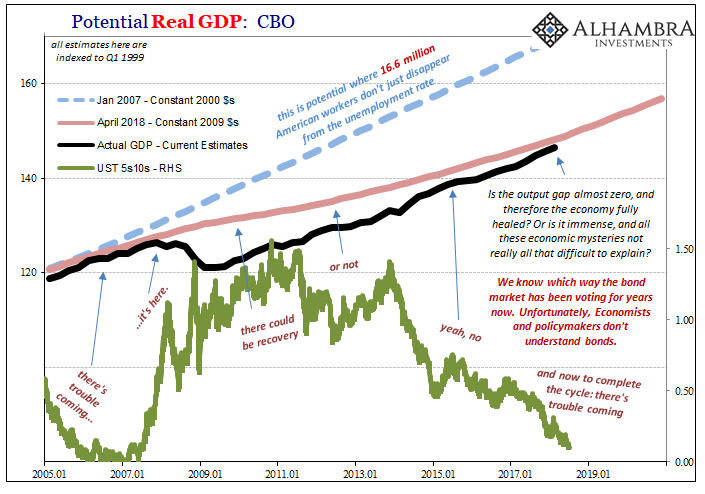

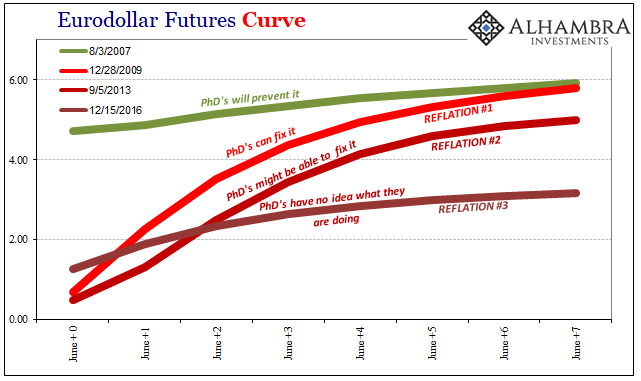

Curves, on the other hand, have done it all. Three times so far. Working on #4. And it’s driving them crazy.

Stay In Touch