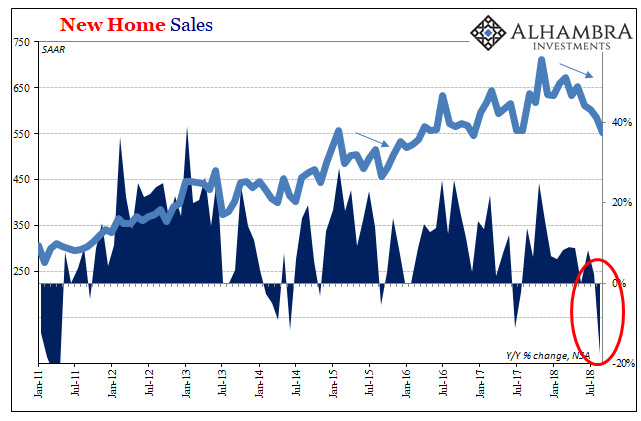

The housing slump accelerated in September. Matching the poor performance of resales, sales of newly constructed houses tumbled last month, too. According to the Census Bureau, there were 41k (unadjusted) single-family units sold. That’s down an alarming 18% from the same month last year. At a seasonally-adjusted annual rate of 553k in September, the construction market is down for now six months and counting.

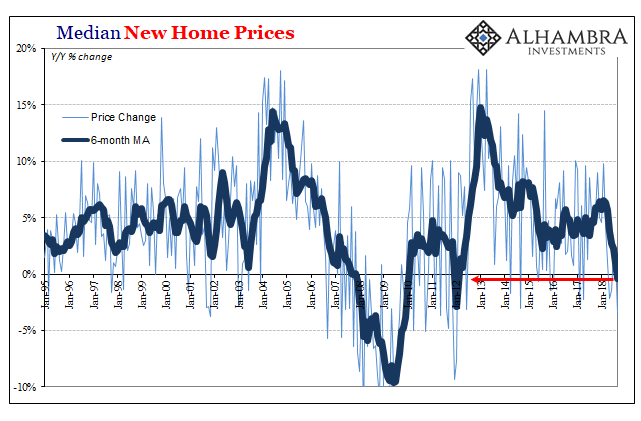

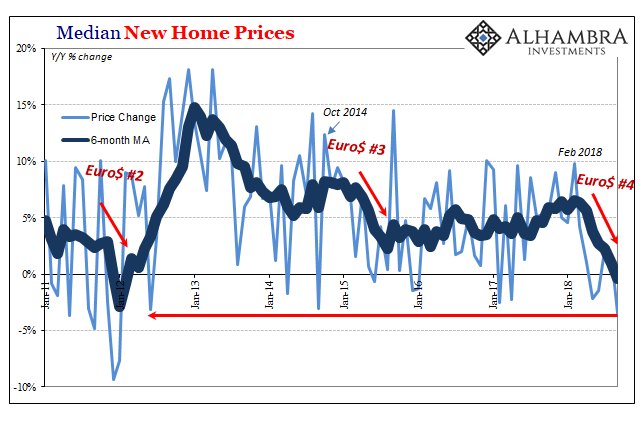

With demand softening, inventory begins to pile up and builders who had been counting on the “strong” economy everyone keeps talking about are forced to discount prices. The Census Bureau estimates that the median sales price for new homes sold in September was $320k (unadjusted), 3.5% lower year-over-year. Though this estimate may be revised in the months ahead as more comprehensive surveys come back, for now it is by far the largest monthly price decline since the bust.

With the median price lower in three out of the past five months, the 6-month average rate of change is now negative for the first time in almost seven years.

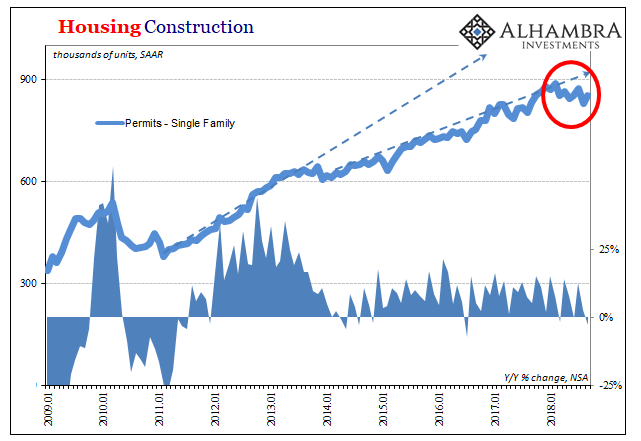

If new homes aren’t selling and builders are being forced to reduce prices to get inventory to move, you can bet that they aren’t going to be enthusiastic about building more single-family structures. Sure enough, the Census Bureau reported last week that the real estate slump has worked its way into construction. The number of permits filed to build single-family homes was a seasonally-adjusted annual rate of 851k in September.

While that was up from a revised estimate of 827k in August, the trend is clearly downward dating back to February. Something has changed in the housing market this year.

It’s the Fed, they say. The central bank in its considered approach to this very strong economy is pushing up short-term interest rates so as to make sure what’s really good doesn’t become even better. The buzzword thrown about this entire year is “overheating”, which is ironic given the last time the same term was used in the same context it worked out pretty much the same way – no overheating, not even a minimally functioning economy.

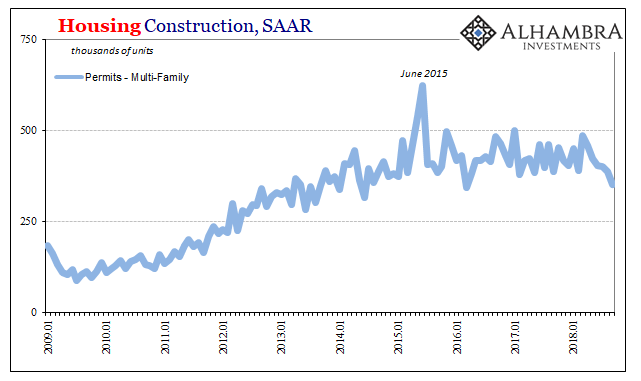

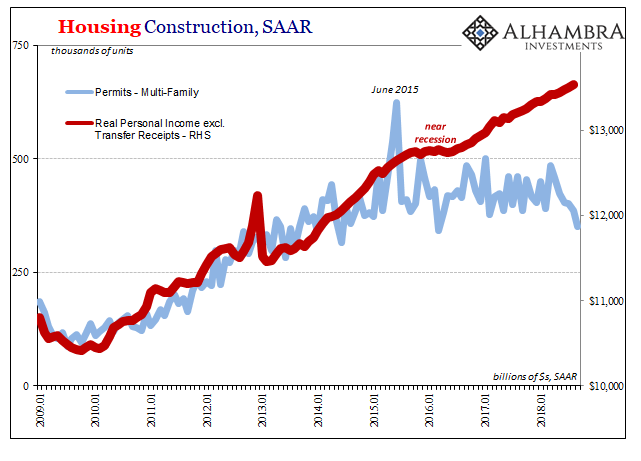

If the economy is roaring and the Fed is forcing mortgage rates into the area of unaffordability in housing, then why is apartment construction slumping to an even greater degree than the single-family segment? The one you can understand, plausible even. Multi-family doesn’t follow.

The Census Bureau also reported last week that the number of permits filed for construction of multi-family units tumbled to a seasonally-adjusted annual rate of just 351k in September. That was the lowest in almost three years going back to the last downturn in early 2016. Permits were, unadjusted, 14% less in September 2018 despite the comparison to September 2017 when hurricanes had reduced permits in that month by 25% from September 2016.

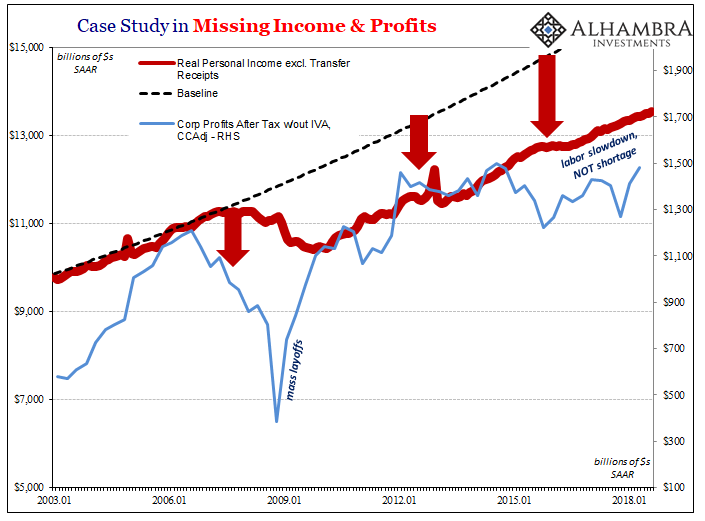

This is not about interest rates, or at least interest rates alone. Consumers, meaning workers, are becoming more and more uneasy about everything. In sentiment survey after sentiment survey, they may parrot the official narrative drawn from the unemployment rate but in practice they are behaving very differently.

Economists would say this is irrational behavior but it is Economists who are emotional about the economy. They are desperate for vindication, and if the recovery does actually happen then the last decade might be forgotten.

It starts with that last downturn almost three years ago; they still haven’t ever accounted for it. But the rest of the economy has had to no matter if it ever gains entry into the “official” record. This includes the housing market, especially apartment construction.

If mortgage rates are making home buying relatively too expensive, then in a growing economy apartments would be in high demand. That’s the only alternative for workers who are truly doing so well with rapidly expanding income opportunities (which wouldn’t make sense for why mortgage costs are too much).

Should the economy be in some other state beside “strong”, then renewed uncertainties especially in the labor market would make (or keep) workers shy about housing in any form. Rekindled revenue and therefore profit concerns, unexpected as always, sure do filter down to the rank and file.

You can’t even explain this by rising interest costs for builders who have to finance construction and inventory. Even if their liquidity expense was rising, they wouldn’t cut back on their business if the economy therefore prospective opportunity in real estate was truly robust. Builders would merely accept the higher interest expense and then easily pass it along to their future customers (in terms of rent).

That’s not what we see here.

There was no connection to rising interest rates in 2015-16 except for the confusion as to why the Federal Reserve hadn’t begun its exit regime earlier and with more confidence and aggressiveness. Even the history of median sales prices for new homes sold shows the effects of actual economy rather than the modern myth of Greenspan.

The only connection to the Fed in this spreading housing slump is its forecast error. Economists claim to believe that the economy is so strong that it requires monetary “tightening” at about half the pace when compared to the last “rate hike” cycle. The Fed is going noticeably slower than was projected just four years ago because the economy has swung so far toward robust?

Nope. Officials are merely hoping in the absence of full-blown recession that time was the final factor in their favor. Instead, the more time passes the more actual economic conditions deviate further from the narrative incorrectly set by the unemployment rate. People say the economy is like that but act as if it isn’t real.

Now in 2018, like in 2015, there is the sudden and unexpected appearance of “overseas turmoil”, “rising global tension”, or whatever other term someone will invent to try and dismiss what is a very real economic shift. Think about it from the perspective of a worker who has heard about this booming economy but doesn’t see it, and now feels more negative factors building up that no one is accounting for – especially Jay Powell.

If you, like far too many others, felt like you were in danger of being left out of the “boom” before, how about this year? Rising consumer/worker/home buyer/renter caution is nothing to do with the Federal Reserve except that it had long ago abandoned its one job and left the global economy to suffer these regular ups and downs. The upswings are never really that much, and the downswings aren’t downswings according to central bankers (“transitory”).

The economy goes nowhere and nobody knows why or that in the big picture this is exactly what has happened, and keeps happening.

Stay In Touch