In September 2009, leaders of the G20 nations got together in Pittsburgh. It was the third such summit in close succession following the devastating events of the monetary crisis, ostensibly so that each head of state could share strategies with the others as to how to avoid blame. Solutions weren’t in good supply, obviously.

Populism was a bit different in those days, even the most unwise politician knew that at minimum someone somewhere needed to address TBTF (too big to fail). Banks were simultaneously the cause of the disaster and its biggest beneficiaries (according to many people’s perceptions). While millions upon millions of workers were being laid off all over the planet at the same time the official sector was handing out trillions to the ultimate in reckless behavior.

They decided to appeal to the Financial Stability Board despite the fact this FSB organization performed so poorly it had only months before required rebranding (it was first known as the Financial Stability Forum throughout the grave global instability of the crisis). The FSB was tasked with first designating who might be TBTF and then burdening whichever bank with whatever additional bureaucratic rules to placate the stirred masses.

Like capital ratios, the concept of Global Systemically Important Bank (G-SIB) or Systemically Important Financial Institution (SIFI in other supranational contexts) is smoke and mirrors; a layer of almost random mathematics applied haphazardly to the biggest banks. Buckets are big to these people, as are the arbitrary mathematics that go into creating them.

The FSB focuses on five criterion and then assigns each bank a weighted score.

The methodology gives an equal weight of 20% to each of the five categories of systemic importance, which are: size, cross-jurisdictional activity, interconnectedness, substitutability/financial institution infrastructure and complexity. With the exception of the size category, the Committee has identified multiple indicators in each of the categories, with each indicator equally weighted within its category. That is, where there are two indicators in a category, each indicator is given a 10% overall weight; where there are three, the indicators are each weighted 6.67% (ie 20/3).

Why is everything equal weighted? Showing their hand a little too much here. Why not more specific thoughts on how each category might idiosyncratically contribute to systemic distress? Surely different characteristics mean different things at different firms (and at different times)? They don’t really want to get too deep on these topics, though, they just want to output some complicated-looking numbers to the public.

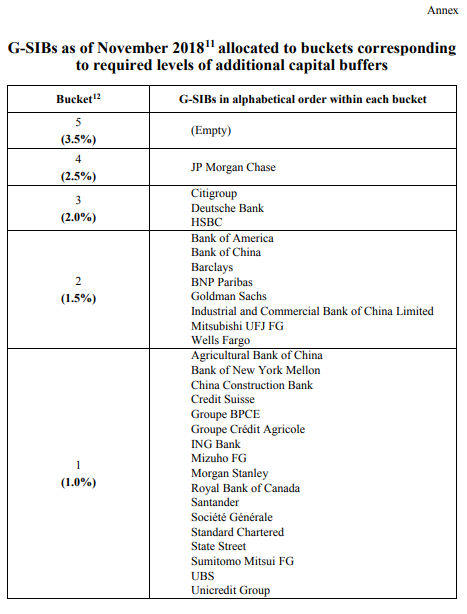

Furthermore, banks placed into these “buckets” are assigned another arbitrary burden. The top bucket as it currently stands (November 2018) is #5 and is empty. Any bank that falls into it in the future (these scores are changed with conditions) would be required to hold an additional 3.5% capital adequacy “buffer” (defined as additional common equity above what is already required of any bank as percentage of risk-weighted assets) – because capital ratios worked so well for SIFI’s like Bear Stearns, Royal Bank of Scotland, or AIG (which didn’t have one because it technically wasn’t a bank).

Here’s the latest list:

Again, not much real thought went into this process. The end result was simplicity by design; politicians via bureaucratic regulators identified those banks who are too big to fail and made them safer, so here’s the numbers that show it. Why a 2.5% additional capital buffer and not 4.6893% or some non-numeric maybe even common sense sanction? Arbitrary.

Apart from the disingenuous nature of the enterprise, the real problem is the approach. Regulators are still looking at the banking system as a collection of individuals, some of whom could turn out to be “bad” banks. If we weed out the bad banks the good ones who are left will keep the system afloat in times of trouble. Or, better still, if we force bad banks into becoming good banks, pace Yellen, there will never be another financial crisis in our lifetimes. That’s the theory behind everything.

What if instead the problem wasn’t bad banks but a rotten system that contains them all alike? The nature of the 2008 problem wasn’t Lehman Brothers, it was all of them together doing things they shouldn’t have (and I don’t mean subprime). If the system is flawed, then assigning arbitrary scores to good or bad banks is…arbitrary nonsense.

In other words, if the system as a whole becomes unstable there are no such things as “good” banks – they are all screwed, only to different degrees. That’s how 2008 unfolded. It wasn’t that Lehman was in the “bad” category, rather Lehman like AIG or Wachovia was the most exposed to massive faults across the whole thing.

What actually is TBTF isn’t an individual member, it is eurodollar!

Given all that, there is much about the last year that G-SIB’s can tell us about how things are going. Perhaps counterintuitively, these banks as a group show just how badly mainstream convention misunderstands the role of central banks.

Briefly, it is presumed that when a central bank like the Fed “raises rates” it has a restraining effect on all banks. The basic bank model in conventional reckoning is maturity transformation; that is, a bank borrows funds short-term and lends out long-term. The profitability of each is therefore determined by that spread. Raising the short-term rate should therefore lower bank profitability, reducing the appetite to engage in credit creation.

The economy slows predictably.

But that’s not how it really works, at least outside the Economics classrooms of Ivy League institutions working exclusively with statistical models. When economic opportunity is real, meaning sustained robust conditions, banks tend to do quite well because the way they put together their balance sheets aligns with that factor (the short-term rate is just one input among many more important ones).

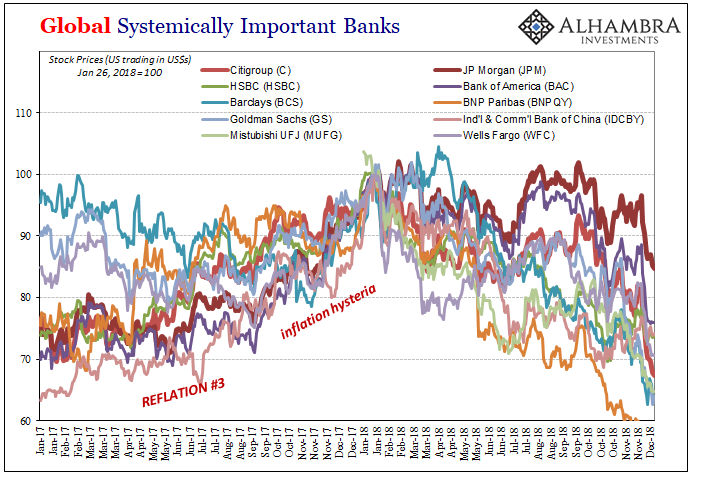

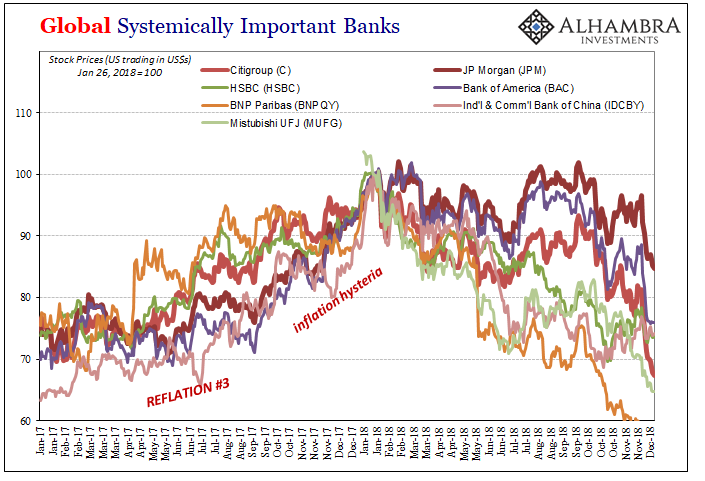

Late last year, many markets including stocks were gripped by hysteria of a specific kind – inflation. It was widely believed that the global economy the US in particular was about to enter a period of boomingly strong growth. The key features were the low and lower unemployment rate suggesting building wage pressures that would unleash inflationary forces for the first time in a decade, requiring a more robust response on the part of Yellen now Powell.

More even aggressive “rate hikes” on the horizon.

Not just in the US, but eventually it would lead to those in Europe and many thought Japan, too. For the first time in forever, people were actually thinking the BoJ had pushed that poor country out of its “deflationary mindset” nightmare. Globally synchronized growth would’ve meant higher short rates across-the-board, across the globe.

Bank stocks performed poorly because the anticipated shift toward belligerent tightening? Nope. Like other stock classes, shares of financial firms including G-SIB’s were as robust as inflationary expectations – investors seeing the opportunity (and, very importantly, the reduction of risks) associated with economic recovery at last.

NOTE: I’ve included below only the G-SIB’s falling in the FSB’s buckets 2 through 4 (nobody is in 5), with the exception of Bank of China whose stock doesn’t trade in the US and Deutsche Bank which we’ve covered extensively elsewhere, therefore the most systemically important of the SIFI’s apart from that one.

The upward skew for everyone’s share price during the inflation hysteria period is unmistakable. When the consensus was for the benefits of globally synchronized growth, bank stocks performed very well even though it would’ve meant higher rates everywhere over the intermediate period (in some places, like the US, more immediately). Loose not tight in the future.

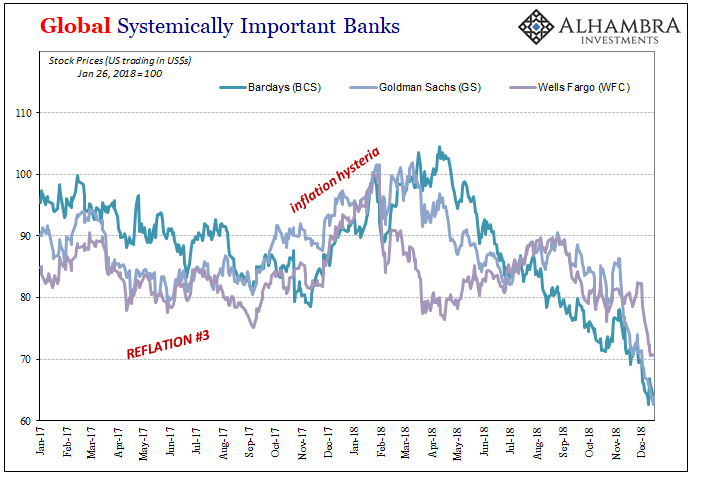

Even for the few banks under suspicion for one reason or another during Reflation #3, there was still a sustained, noticeable bid during this time.

I chose to equalize and index all banks stocks to January 26 for a reason – that was the last trading session before the first liquidations struck this year. As you can see, everything changed after then, more so over time as investors began to (re)consider how conditions weren’t actually ripe for more “rate hikes.”

Recently, even as a “Fed pause” develops in what is surely only the first step to official policy reversal, SIFI stocks are being hammered. Lower on average perceived money rates are never a good thing because they coincide with ridiculously dangerous liquidity risks above all (interest rate fallacy).

In this one instance, the stock market of all things is demonstrating exactly what’s wrong in 2018. It isn’t “rate hikes” or QT, those things consistent with inflation hysteria. It is instead the rotten global money system acting up all over again. The G-SIB buckets don’t tell us anything about good or bad banks, but even the stock market is attempting to draw attention to how they are once again all at risk regardless.

Hawkish or dovish Fed, these terms are likewise meaningless. As are, on their own, “rate hikes.”

Stay In Touch