OK, that’s more like it. Finally. American consumers absolutely splurged last month. According the Census Bureau, retail sales last month spiked by nearly 2% (seasonally-adjusted) from August, an unusually big monthly increase. This surge in spending during September 2020 sent the unadjusted total up by just more than 7% from September 2019.

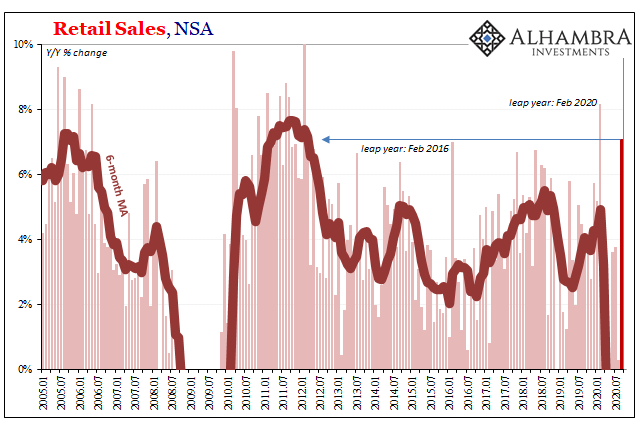

How good is that? Setting aside the statistics of February 2020’s 29th day, this was the biggest increase in total retail sales in eight and a half years. You’d have to go all the way back to March 2012 for any month without an additional leap year day to have been better. Last month’s growth rate edges out the one from February 2016 even with its 29th day.

If we’re looking for something, anything “V-like” this would be the thing.

V’s, however, they aren’t made by a single month qualifying, or even a couple months sticking around in the ballpark. Consistency is the thing; temporary consumer insanity comes and goes all the time. Even more frustrating, these kinds of one-off splurge-fits tend to occur during just these kinds of times.

These retail sales numbers are obviously sticking out in the opposite direction from all the labor data. September 2020, remember, is the same month when the BLS indicates an enormous number of former workers apparently became discouraged and dropped out of the labor force entirely.

Two key data points ostensibly looking at the same thing from different angles, each very much at odds with each other. This kind of disconnect, however, has happened before.

When?

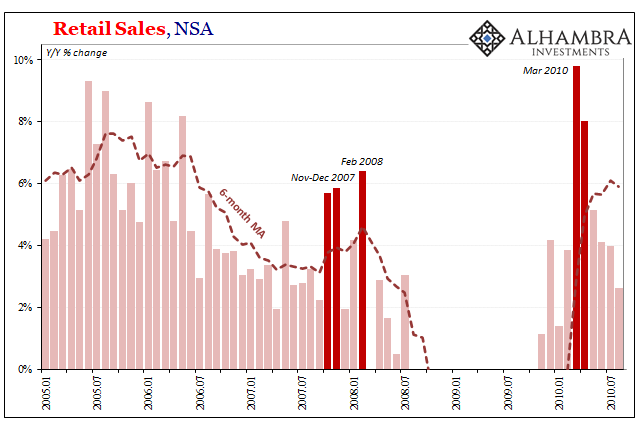

According to the latest benchmarked data, during March and April 2010 retail sales jumped by even more than they did last month. In the former month, the unadjusted year-over-year increase was very nearly double-digits. That was followed by an eight percent increase during April – but then several months of slowing which included the labor force shrinking by nearly 1 million in May and June 2010.

You might recall those particular months if for all the wrong reasons. Like now, or even like late 2007 and early 2008, the economy was supposed to have been recovering (in late ‘07/early ’08, rebounding from so much Fed “stimulus” so as to entirely avoid any recession the rest of 2008). The big number for retail sales seemed to be corroborating the typical post-war “V” pattern which had come to be taken for granted.

Except, in May 2010 there was the (first) flash crash on Wall Street along with a bunch of hazy news about Greek bonds or something. Even before May, trouble in the Middle East and other parts of Europe, each time the bond market (read: repo) had been front and center.

What was supposed to have been the start of full and complete recovery – as the word recovery had been previously defined – instead got derailed by the first steps toward what would eventually become Euro$ #2. Because QE1 and ZIRP hadn’t taken care of the original problem which had ignited GFC1, the global dollar system’s drag reasserted itself pretty early on in late 2009 and especially the first half of 2010.

Too many contrary signals for something like sustained recovery.

Thus, the question for beyond September 2020 is whether this first “V-like” month since March ends up being the only one, or even one of too few. Or, is this really the start of something, the perhaps delayed rebound momentum kicking into the badly needed higher gear?

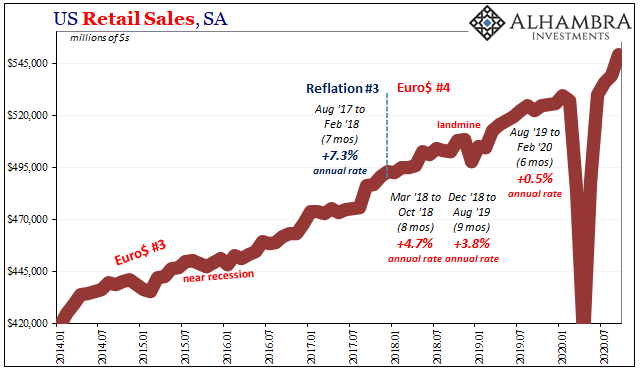

While we can go to market prices and indications to search for clues, that also depends upon which market you value most. Stocks, obviously, they remain firmly glued to the “V” no matter which “V” that might be given the narrative has changed (September retail sales notwithstanding). Bonds and dollar, on the contrary, unimpressed by a single month of consumer insanity, having seen all this before (including the ineffectiveness of QE), are trading as if this is a transitory blip.

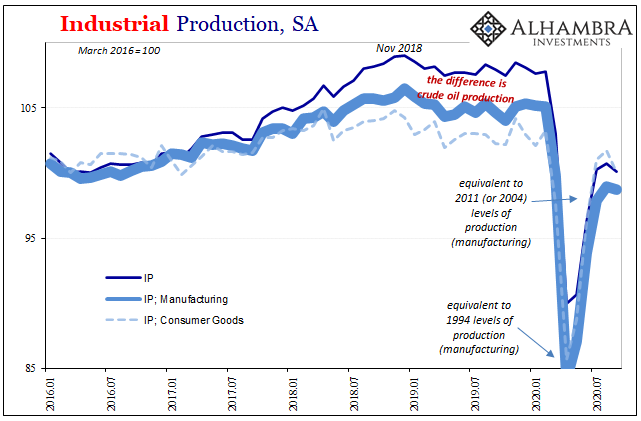

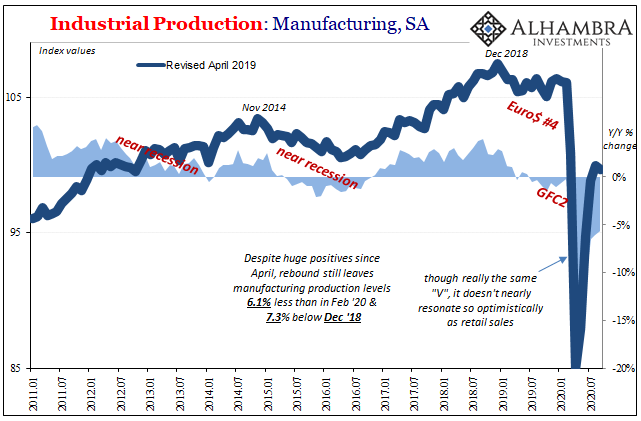

Fortunately (unfortunately, given what follows), we also have estimates today made available for what the production sector thinks about all of this. The Federal Reserve released its data on Industrial Production for September 2020, too, though unlike retail sales the post-July stumble continues further down the supply chain.

Down last month from (upwardly revised) August, there’s been little rebound since June. That’s three months which is more like the labor data and more established than retail sales. It’s also widespread, across-the-board. Utility output sank the most in September, but, as you can see above, no sector was immune from the ongoing slowdown/setback.

Manufacturing most of all, which should be running at elevated levels already if to catch up to retail sales, remains severely depressed. Compared to September 2019, total manufacturing output was nearly 6% less in September 2020. That kind of shortfall is more than a mildly recessionary rate.

What this difference between production and sales suggests is that manufacturers (and miners) aren’t yet buying the splurge in consumerism. And that could be for a couple reasons: the entire supply chain is looking at September as the anomaly in spending, a temporary increase for artificial reasons before coming back down; at the same time those within the supply chain are actively choosing to run down inventory for either/both business or/and cash flow reasons (sorry, no $ flood); some of both those things.

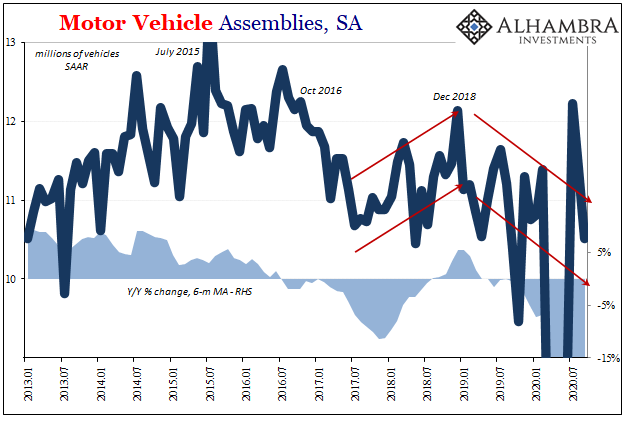

Those implications might be most evident, and most pressing, in the auto sector. Before getting to that, though, the Census Bureau says the auto sales part of retail sales in September exploded upward, rising more than 14% from September 2019. This contributed a lot to the headline gain.

On the other hand, the BEA’s version of auto sales counting units remained down by more than 4% year-over-year for the same month.

In terms of the Fed’s IP data, total Motor Vehicle Assemblies had jumped up in July to a rate of more than 12 million (SAAR) but have since fallen (sharply) down to fewer than 10.5 million during last month. More like recession again than retail sales “V” recovery.

As we’ve noted the past few days by looking at specifically Industrial Production around the world, the numbers, rates, and trajectories all look the same way even coming from such disparate geographic locations. Not even half a “V.”

That’s the thing about “V’s”, and the lesson which should have been learned back in 2010; they are, or should be, unambiguously widespread. Though these are even more uncertain times than back then, which we all hoped would’ve been impossible, despite the lack of complete clarity there’s a more than reasonable basis – history plus broad survey data – for widespread skepticism that this one month of retail sales isn’t the belated start of the thing.

And that’s just the “stimulus” “V” talking. Which, you’ll recall, is also just like 2010 and that year eventually succumbing to QE2 (also didn’t work). If officials believe they need to do more “stimulus”, and they sure do right now, that’s not a good thing.

Retail sales in September definitely were; unless it accelerates and repeats it won’t be close to enough. Doubts to that possibility most likely explain why retail sales are all alone in that regard.

Stay In Touch