You’d think Larry Summers would know better. Not that he stepped in it, again, but rather why he did this particular time. Making a big deal out of inflationary aggregate demand when he’s been practically the lone mainstream Economist to look at the post-2008 economy in an honest and serious fashion to then somehow failing to incorporate that view into our current place.

What got Summers in hot water a few days ago was a rather careless throwaway surrounding his usual partisan politics. Essentially asking the question why the government would want to give $2,000 to all Americans. It’s a legitimate query but one unfortunately couched first in typical and typically unhelpful DC squabbling.

When I see a coalition of Josh Hawley, Bernie Sanders and Donald Trump getting behind an idea, I think that’s time to run for cover.

The more significant problem, in my view, was the basis from which he attempted his answer. Forced to explain this pure bias, or BS, further, Bill Clinton’s former Treasury Secretary felt impelled to write an op-ed for Bloomberg on Sunday in order to clear things up. It wasn’t politics, he claimed, but rather bad Economics (capital “E”, in this case).

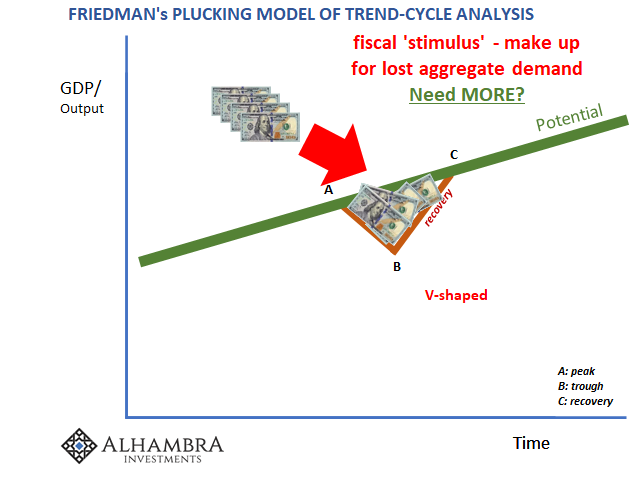

The question is whether there is a rationale for further tax rebate of more than $200 billion a month over the next quarter. This would represent additional support equal to an additional seven times the loss of household wage and salary income over the next quarter.

The government is in danger of doing too much. To be fair, Summers stated unequivocally his support for those who are being hit hardest by the current disastrous economic state. By all means, give them cash aid, he argued.

At issue instead are those who maybe haven’t quite suffered seriously, Americans not only still working but having barely noticed the grave peril which has engulfed so many of their fellow citizens (that’s the real “too much”). On moral grounds, it’s a perfectly worthwhile discussion; should everyone receive a(nother) handout?

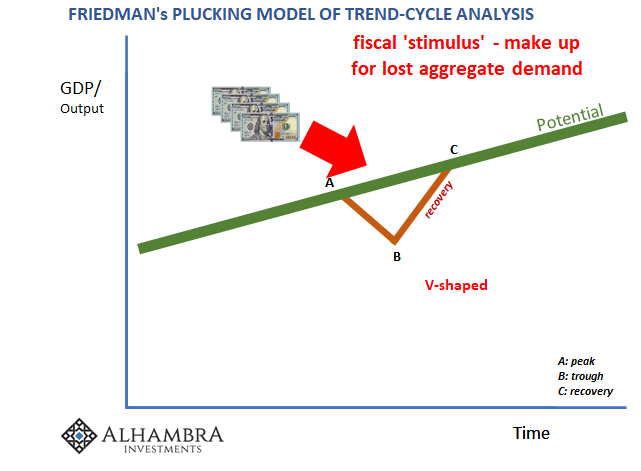

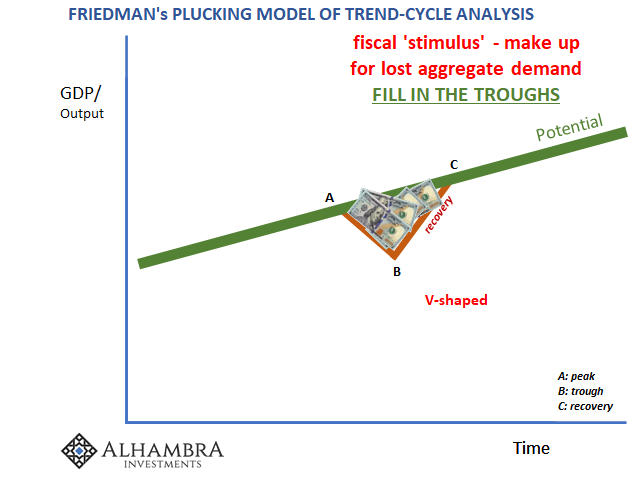

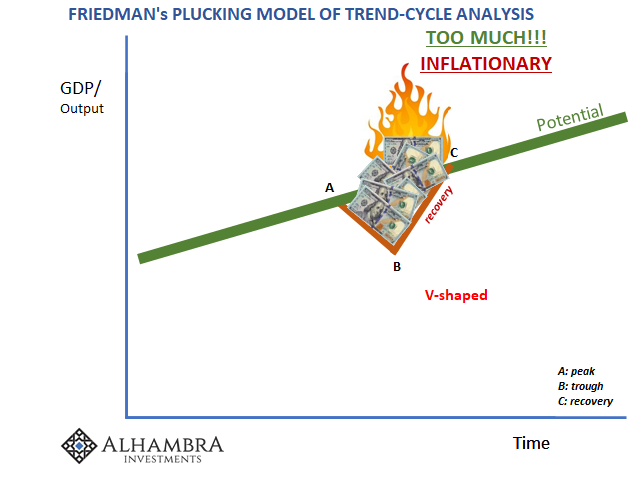

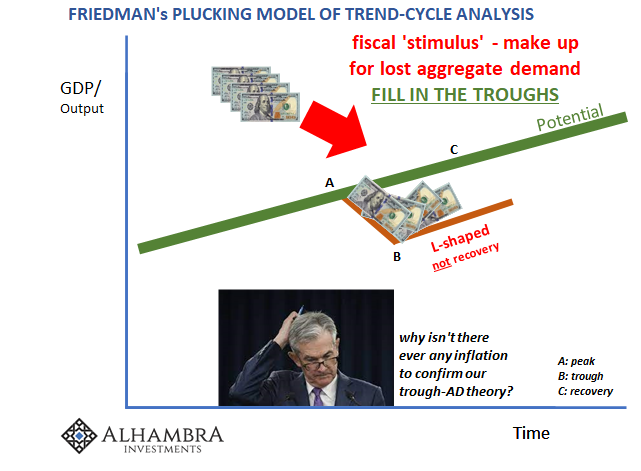

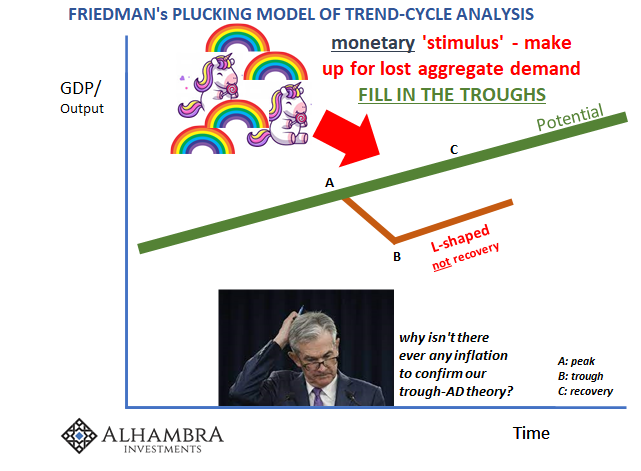

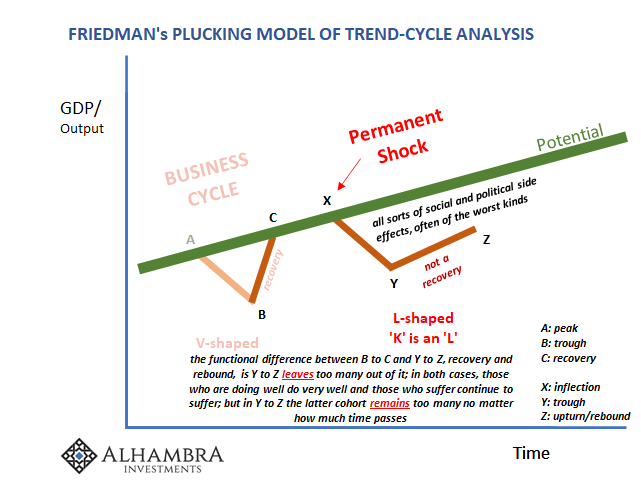

It’s the Economic foundation for what becomes Larry’s objection that is most objectionable. The Keynesian/Japanese idea of “too much.” The problem, as any mainstream Economist sees it, is that once you’ve filled in the trough you need to get out of the way of the recovery lest it run explosively hot seventies-style.

That’s what this is really about – and has been about since 2008. Aggregate demand is a fancy word for lost economic output which has been lost because of recession. But recession itself is little more than a temporary deviation from economic potential. Painful, sure, but given enough time everything goes back to normal insofar as policymakers don’t screw it up before reaching that critical point.

The orthodox prescription for a recessionary trough is, in theory, very simple: fill it in. Boost government spending – funded by borrowing rather than taxation – to limit the economy’s downside, amplified even more by whatever monetary policy does. It is the downside, marked by time, which is the real enemy. Long run economic damage comes about when there’s too much time, or too much depth around the trough, which can harmfully reshape economic potential.

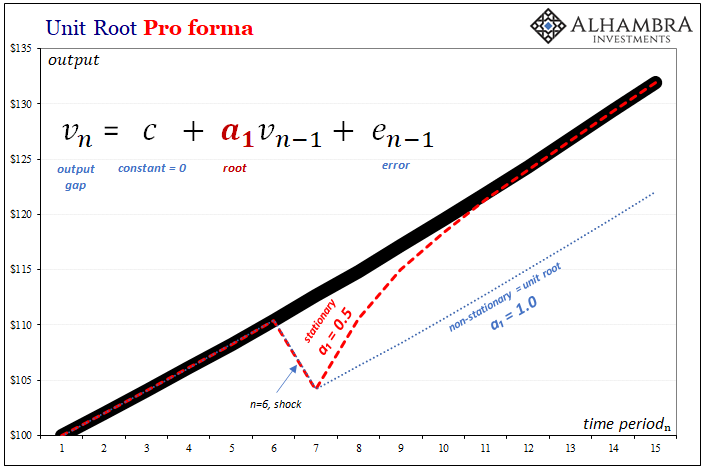

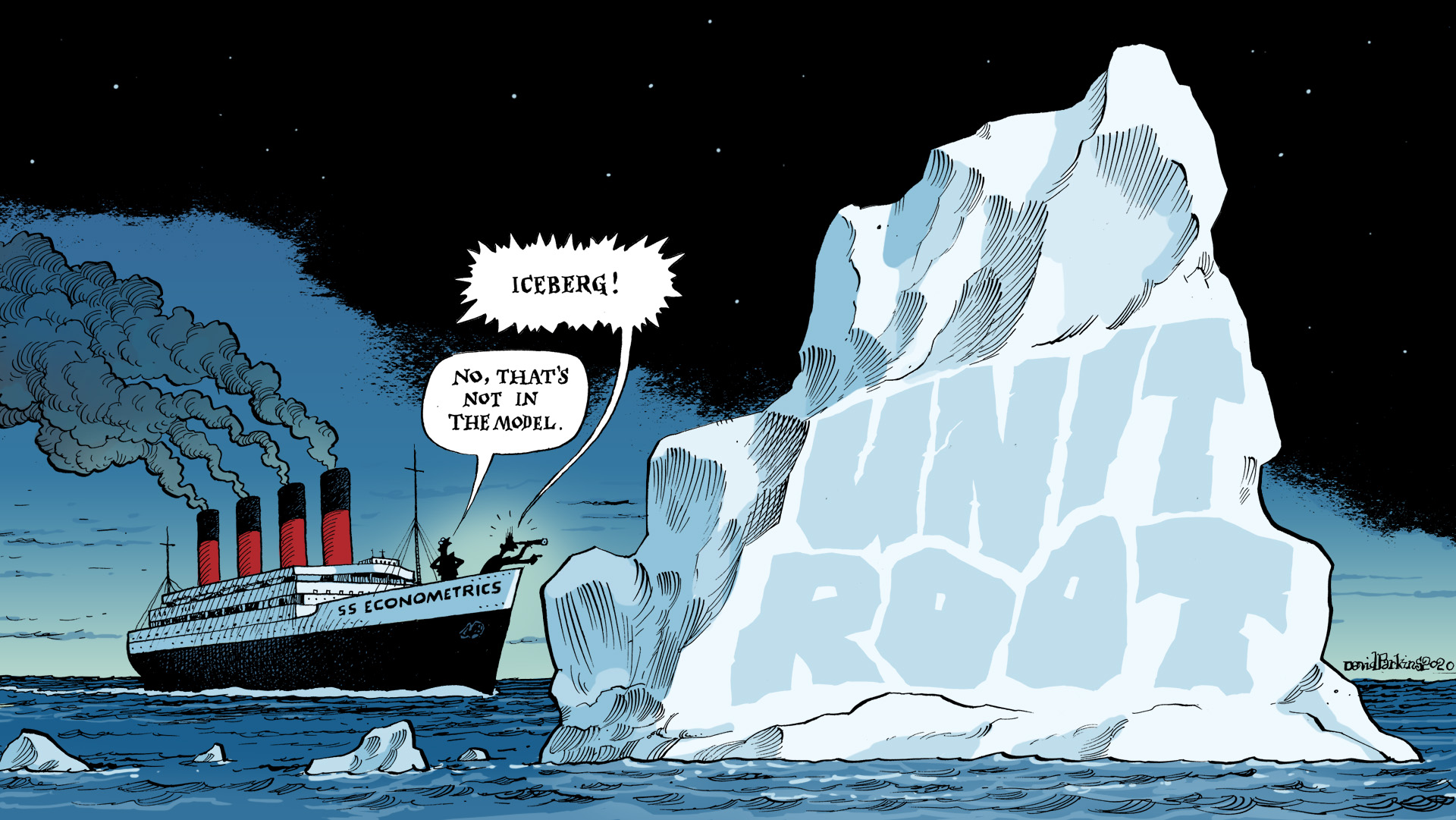

Economists like Summers, however, don’t worry about such things. They’ve banished unit roots from their econometrics, in the process completely disregarding any notion of a permanent shock. Faced with recession, therefore, always recovery because recession is (presumed) an unwelcome but ultimately transitory setback.

Yet it had been the Economist Larry Summers who around 2015 began yelling about “secular stagnation.” A permanent shock, yes, but one which he said looked more like what had Alvin Hansen up in arms in the thirties; a Marxist-like innovation plateau, lack of new land, and a permanent shortfall of babies. Not a shortfall of aggregate demand, a break in trend/potential due to problems outside the purely economic system which conveniently (for 21st century policymakers) wouldn’t be fixed by orthodox macro prescriptions like these (also monetary policy).

This wouldn’t necessarily be repeated for what nearly all Economists believe is a COVID issue alone in 2020 and for 2021. Like 2008, fixing what they said had been a subprime mortgage problem, fix COVID therefore recovery. Fill in the trough in the meantime, but be careful not to do “too much” lest the fires of inflation burn too hot and run out of control too quickly.

That is his material hostility to the proposed $2,000. Worded poorly, written out first out of emotion, it’s standard neo-Keynesian claptrap nonetheless of the kind we’ve been forced to sit through for over a decade.

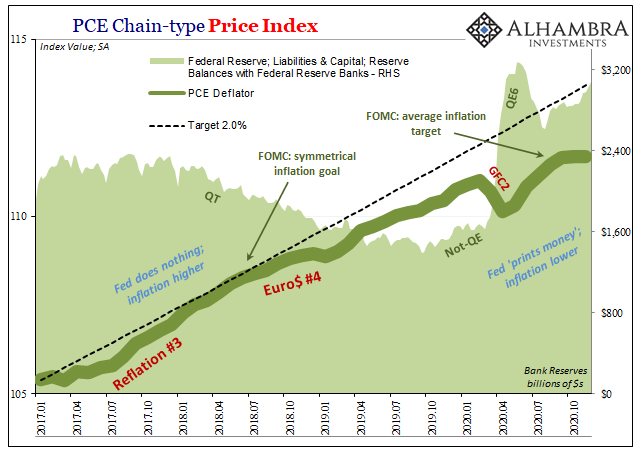

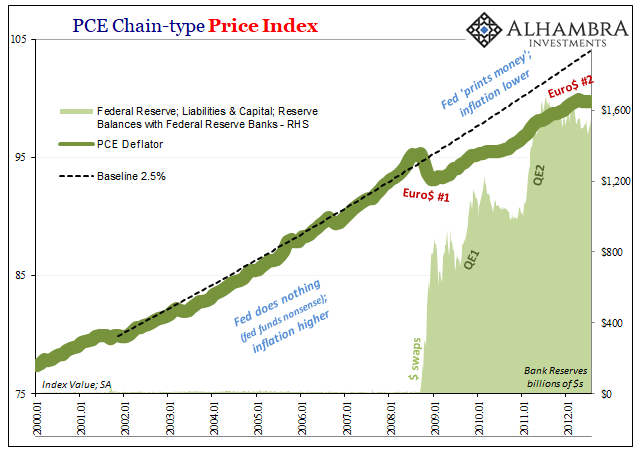

At this point, of course, Jay Powell would like a word. The Federal Reserve simply cannot find the inflation from the first time they’d “filled in the trough.” Remember back to 2009, it was both extreme levels of monetary policy plus historical profligacy on the fiscal side and yet no inflation to confirm the trough had been partially let alone completely plugged.

Leaving one Larry Summers half a decade into it to wonder about the possible origins of decidedly disinflationary “stagnation.”

In other words, what if the recovery isn’t a surefire outcome? What if unit roots, meaning permanent shocks on the macro side, are very real after all? Could it be that what had unleashed the deflationary depressions of old, monetary panics, might not have been historical relics after all? Especially when the currency which goes inelastic in order to trigger one isn’t a currency any policymaker has ever had their eyes on.

And then it happens again.

Thus, one answer to the post-2008 “L” – as in lack of recovery – and therefore stagnation then raising the prospects for a second “L” following a second and very devastating monetary disruption earlier this year. In short, another permanent shock which wouldn’t immediately accede to recovery and a filled-in trough even at government-funded thirteen-digits.

No inflation, again, despite so much “money printing” (the true nature of monetary policy depicted realistically several graphs upward) and fiscal recklessness. You know, the Japan situation.

The on-the-ground problem with Summers’ thinking is quite obvious to those who participate in the real economic situations left to suffer these consequences (which are not Economists). Larry is talking about paying people (whether all or just a targeted group) for the next quarter for whatever lost income during that quarter, and thinking that’s likely more than good enough to get everyone through the trough.

But what about the quarter after that? And the one after that? And…

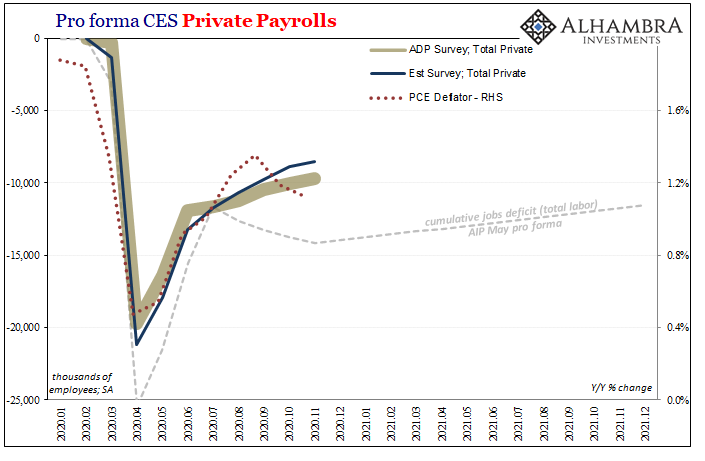

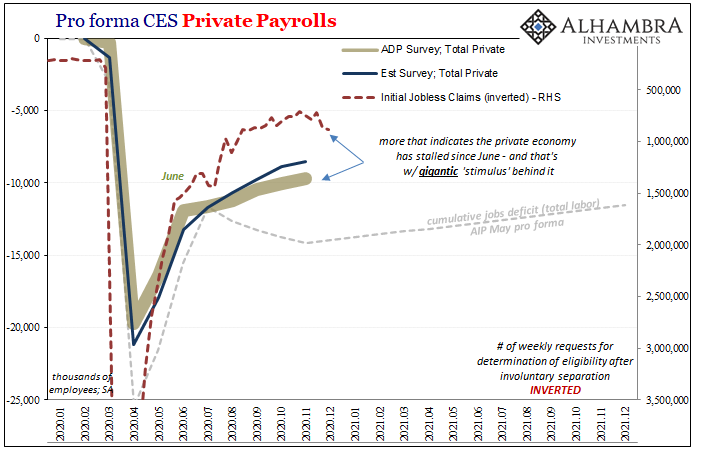

The assumption is there won’t be any permanent damage when we’ve already seen signs (and not just anecdotes) in practically every systemic corner. Businesses that won’t be coming back, that’s economic potential lost for reasons of time as much as COVID. Those struggling to hang on, who, as this thing only drags forward, can do nothing else other than give up.

They aren’t coming back and they’ve taken with them all that potential needed for there even to be a trough. But from Summers’ perspective, it’s all figures in a series of equations. To an Economist, the problem is always about why people don’t act the way the numbers do on the spreadsheet – and then work backward from that position. What Economists need to start doing, for once, is to ask themselves why their spreadsheets never seem to accurately model what really happens to these unfortunate people.

And why it keeps happening.

From that question, the possibility of permanent shocks (unit roots in the models) isn’t a big stretch at all. Stagnation the result, the situation isn’t even a trough to be filled in. Again.

Stay In Touch