Quick questions: who said the following, and when did this person say this?

Our own country has tried one economic theory after another. The present Administration asked for, and received, extraordinary powers upon the assurance that these were to be temporary. Most of its proposals did not follow familiar paths to recovery. We knew they were being undertaken hastily and with little deliberation.

The most obvious answer might seem to be any prominent 21st century critic of the Federal Reserve and federal government, but many if not the vast majority of those have spent the past year, indeed the prior decade and more complaining about runaway inflation and dollar destruction sure to be unleashed by those government agencies doing too much. Since neither of those things ever happened, the public is, by process of eliminating suspects from an-all-too narrow suspect list, “stimulus” policies have to be either just good enough or verging on too good.

There had been a boom somewhere in there before COVID, right?

The questioned quotation was spoken during the 1936 Presidential Election. Republican nominee Alf (not a 1980’s TV fiction) Landon ran his campaign on a platform of, asking sincerely, where’s the damn recovery?

His opponent, the incumbent Democrat, had entered office four years earlier and upended near everything on the promise of one. In his first reelection bid, FDR would boisterously respond to Landon; we’re in it, and you’re evil for trying to mislead Americans otherwise.

It is needless to repeat the details of the program which this Administration has been hammering out on the anvils of experience. No amount of misrepresentation or statistical contortion can conceal or blur or smear that record. Neither the attacks of unscrupulous enemies nor the exaggerations of over-zealous friends will serve to mislead the American people.

Roosevelt, however, knew very well he was the one fabricating fiction, not Landon. While the economy was rebounding from its deepest low on record, the turnaround was nowhere near full recovering. Instead, the message to voters was a deliberate rhetorical sleight of hand, urging them to see the thing through all the way – give it time and the recovery will happen in the future.

It was that last part that was sort of silently implied.

Not wishing to spoil what seemed to at least be the right direction, the electorate agreed with both Alf and Franklin…by voting overwhelmingly for the latter (it wasn’t even close; one of the most lopsided results in the history of practically any free election anywhere). They could tell FDR wasn’t being completely truthful, but at least he was honest about being willing to try anything or everything (much of which wasn’t palatable even to those voting for it).

It just wasn’t enough for Landon to correctly surmise that the New Deal wasn’t working in the way it had been meant.

A few years later, in the wake of the ’37 deflationary disaster (what inflation?), trying to salvage the ‘38 midterm election Roosevelt that April had appealed to his dissatisfied audience on the radio by employing, well, pretty obvious statistical contortion:

Today I pointed out to the Congress that the national income — not the Government’s income but the total of the income of all the individual citizens and families of the United States — every farmer, every worker, every banker, every professional man and every person who lived on income derived from investments — that national income had amounted, in the year 1929, to eighty-one billion dollars. By 1932 this had fallen to thirty-eight billion dollars. Gradually, and up to a few months ago, it had risen to a total, an annual total; of sixty-eight billion dollars — a pretty good come-back from the low point. [emphasis added]

Pretty good come-back isn’t nearly the same thing as recovery, is it? Not when the economy starts out in a huge hole and has so far to go from the bottom that it takes so many years just to register “a pretty good come-back.” A politicians dodge, it’s failure anywhere but Economics.

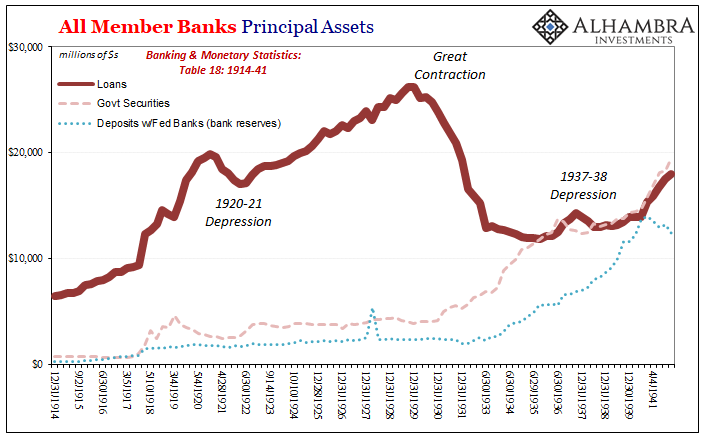

Thus, the Great Depression was made “great” not just by 1929-33, but in a very real sense its legacy was the 1933-39 period of waiting for inflation that wasn’t possible to confirm full recovery that wasn’t happening even though the government kept doing all those wildly reckless things Alf Landon had succinctly pointed out.

Earlier today, Jay Powell made his one-year anniversary pitch; it sounds suspiciously familiar. Writing in the Wall Street Journal, the Chairman said that though risks remain very serious everything is looking up (thanks to him):

…the situation is much improved. A little more than half of the initial job losses have been regained. With the arrival of vaccines, the outlook is brightening. The American people have persevered through this difficult time with determination, resilience and ingenuity.

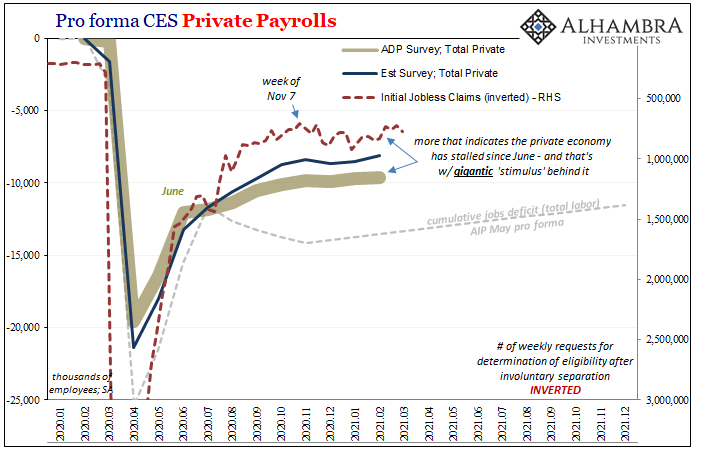

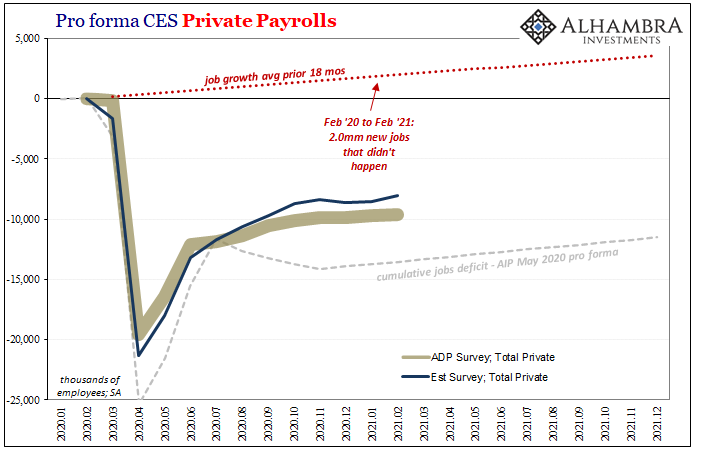

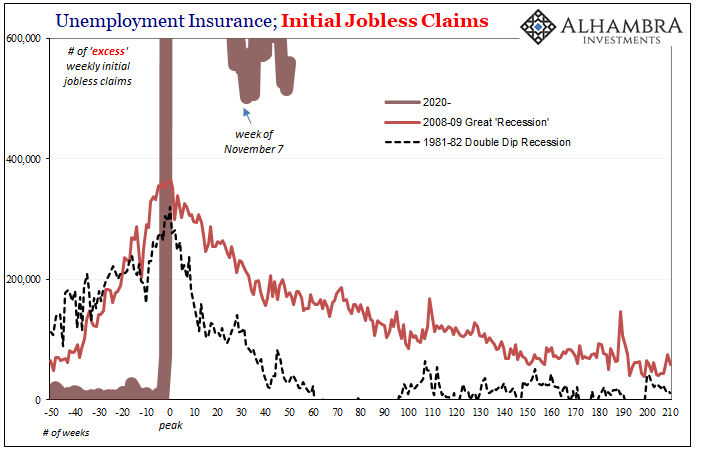

“A little more than half of the initial job losses” is one thing if we’re talking about some regular recession which, peak to trough, forces businesses to shed some two or three million workers at most – who are pretty assured, though unsettled, that throughout history within months maybe a year they’ll be back at work even if in a different place.

But 2020 brought on two things which made the recession of last year even greater than 2008’s Great “Recession” which even today still occupies so much of our economic discourse. Those two things: twin panics over COVID and (financial) collateral.

In weeks, about twenty (not two) million workers were sent home; millions more faced hourly cuts, and the rest of the workforce wondered who’d be next. Despite early optimism (“V”) that it would be really easy, like the flip of a switch turning everything back on just as it had been turned off, as feckless Jay admits the US only got about halfway.

And that was around June last year!

Over the final half of 2020, and the first sixth of 2021 – eight months now! – little progress has been made.

Why?

Jay claimed that his Federal Reserve performed admirably last year when financial markets “somehow” were thrown into a disastrous mess even though, he later claimed, “we saw it coming.” It’s the corona’s fault, you see, and the central bank did the best anyone could have possibly done given circumstances beyond its control.

Back to Powell:

Addressing a fast-moving global pandemic was mainly the realm of healthcare providers and experts, and some asked what the nation’s central bank could realistically do. But we concluded that we had to act forcefully.

And they did; or so they claimed. What’s “forcefully?” It cannot be the mere assembling of big numbers. To be forceful more than implies effectiveness beyond mere absolute figures.

History, in detail, showed just that (and revealed the reasons why Powell would outright lie just two months after it was over). While Powell wrote his version of last year, today I wrote my own quite different summary of March 2020:

It was a Sunday, but no ordinary end to that particular weekend. There was much to be done before the workweek could begin the following morning. At 5 pm in the Eastern time zone of the US, on March 15, 2020, the Federal Reserve finally issued its statement. The central bank’s policymaking body, the Federal Open Market Committee, or FOMC, had decided it couldn’t wait any longer and that drastic action needed to happen – even on a late Sunday afternoon.

The big “bazooka” of monetary shock and awe.

Yet, on Monday morning, March 16, bloodbath. The big bazooka wasn’t just a dud, it had turned out to be another dud in a whole series of them. As the stock market selloff got bigger (and it wasn’t just stocks, that’s just the market the public has been told to pay attention to), so, too, had the “rescues” from Washington.

The S&P 500 opened at just above 2400, rising somewhat during the day and at the final bell eventually less than its open. Close to close, the loss was 11.98%; the worst single day since the Crash of ’87.

Contrary to what Jay’s selling you, the entire crisis had gone in the same way; one “bazooka” after another had failed to stem the rising global tide of wrecking illiquidity (global dollars, after all). Only an unscrupulous statistical contortion of the events late February to late March 2020 can conclude otherwise.

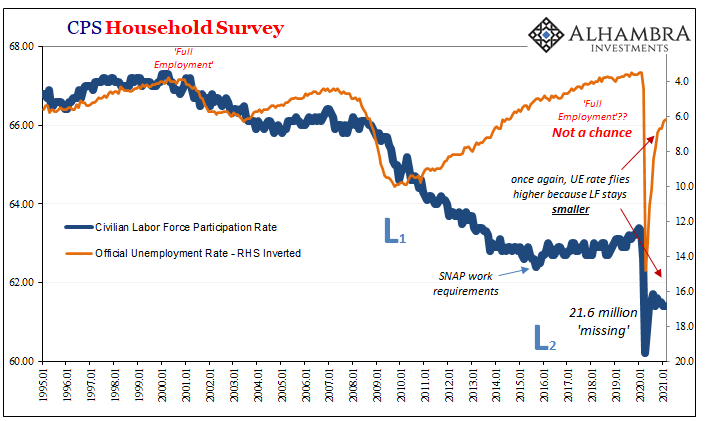

And so, we have to ask just how it is that one year later the US economy can be short not just the 10 million or so jobs which still haven’t come back but also the 2 million (conservatively estimated) others that never happened? How can we be, like the thirties, stuck with Chairman Powell, like Chairman Bernanke not long before him, trying to sell the public on yet another “pretty good come-back from the low point?”

Like the thirties, and the 2010’s, liquidity and perceived permanent risks have a whole lot to do with it.

The labor market’s struggles – as yet another week strolls by with initial jobless claims more than 700,000, the 52nd such week, a full year at levels more than any other week in pre-2020 history – are not COVID alone; they cannot be.

If “they” can’t be honest about what happened last year, and 2020 featured the most massive numbers since FDR, thirteen-digit “stimulus” programs, of course we should expect each of the same results, the same excuses, and the same shifting goalposts.

A pretty good come-back has never been anything more than not nearly good enough. What follows is, as it has been, (more) statistical contortions and only (more) trouble.

Stay In Touch