Admittedly, there isn’t much economic data released in the back half of every month. So, we’re sort of stretching our gaze into the second (maybe third) tier. But in this case, it’s just by way of reinforcing much what we already know and further what’s been suspected.

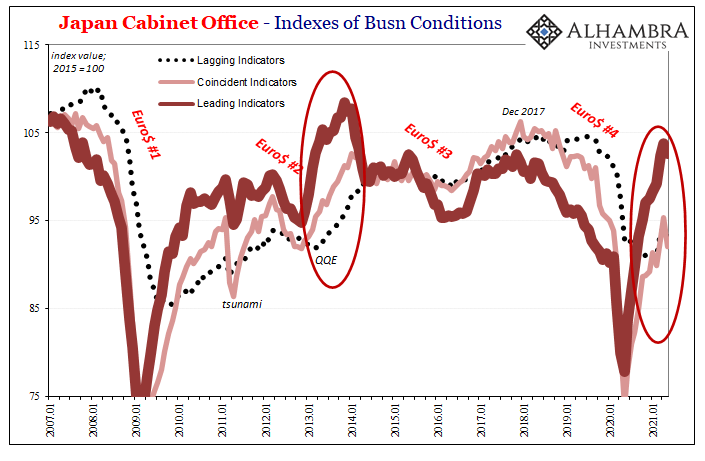

Over in Japan, the government’s Cabinet Office gathers surveys, cross tabulates results and market prices, and then produces a set of economic indicators from leading to coincident to lagging. As I already said, lower tier.

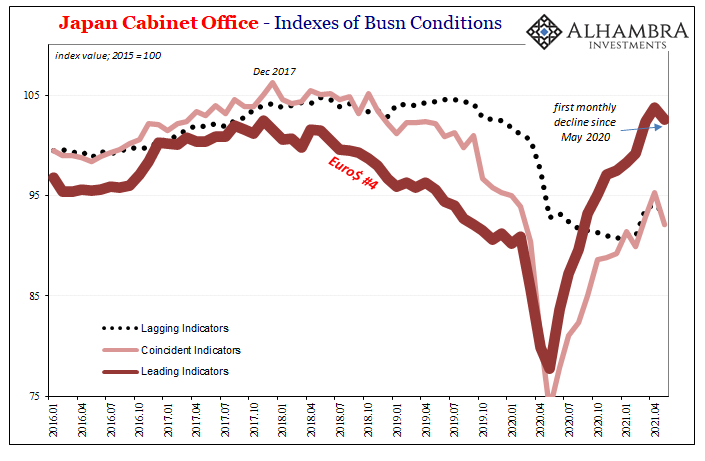

Still, there’s been value in it as a corroborating proposal for things going on elsewhere (see: Euro$ #4). What’s potentially noteworthy is the Leading Economic Indicator (LEI) for May 2021, the result released just today; it declined for the first time since last May, down more than a point, too.

We obviously don’t want to make too much out of it, especially a single monthly decline for one piece of a dataset that rarely, if ever, by itself moves the needle of anyone’s analysis. But it wasn’t just the LEI, the coincident index (CEI) also declined, too, and perhaps more important is the timing.

There’s something about May.

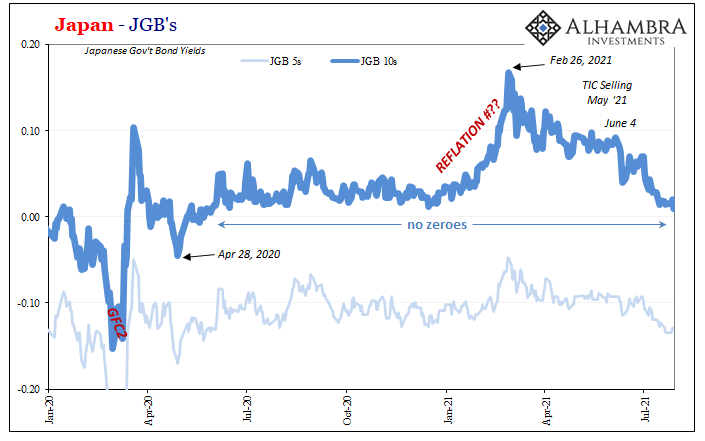

Certainly true for TIC (serious dollar warning) which seemingly set up deflationary potential to get up more in June. This was the case for Japan’s bond market, thereby putting all three of these factors into the same general bucket: bonds, economy, and dollar. None of it going in the right, or inflationary, if that’s your thing, direction.

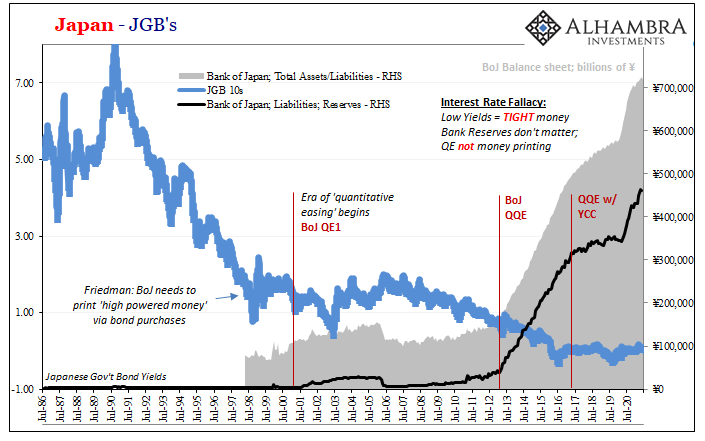

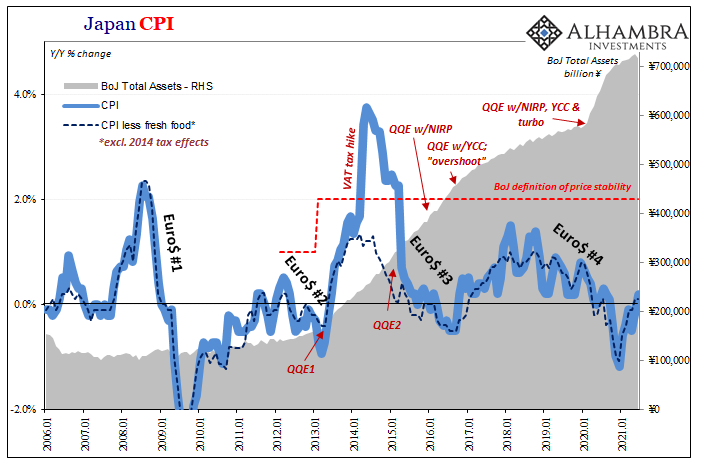

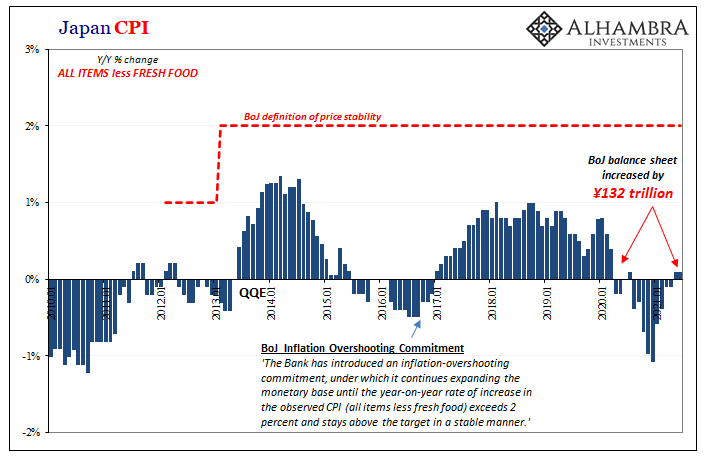

Before the LEI or CEI, though, in Japan as Europe each beset by a lack of inflation. Both central banks have “printed” trillions, in the BoJ’s case, more than a hundred trillion, with truly nothing to show for them. The Japanese continue to perform truly heavenly work by year after year unconsciously proving – beyond every single doubt – that neither QE or bank reserves mean anything beyond ritual.

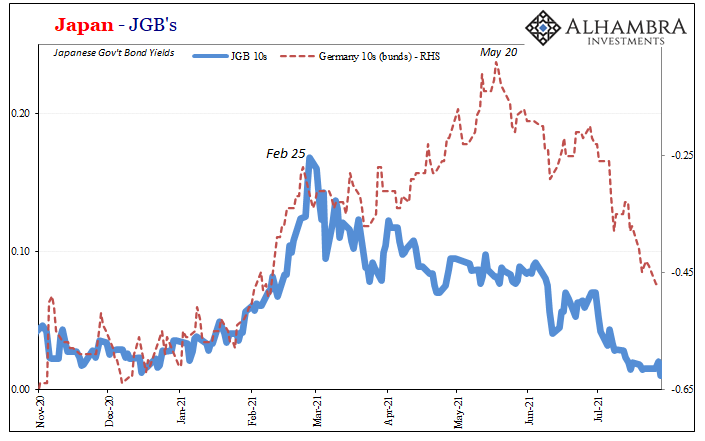

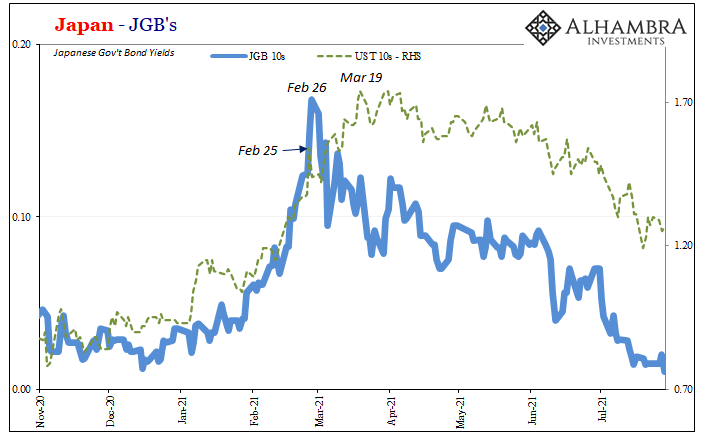

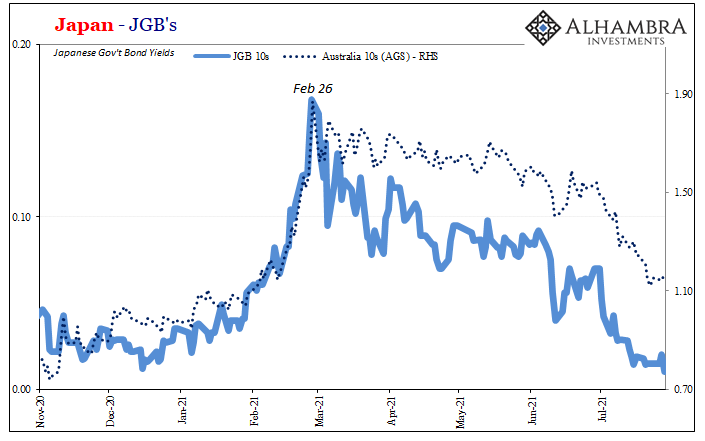

Without any expectation for inflation, JGB yields didn’t move much; but they did move. Starting in January up until late February (a very specific few days in February), modest reflation registered in the Japanese market as it did in bond markets practically everywhere else around the world.

Since, after an initial departure, getting more synchronized by the month. There was first a minor “decoupling” with UST’s (falling in line mid-March) and more so German bunds (syncing up again in, yes, May).

In other words, there is and has been a very consistent global picture (global deflationary factor) across the entire global market. It more than modestly indicates Japan’s yield behavior cannot be strictly Japan, bringing the discussion back to low-level Japanese CPI’s as well as the possibility the LEI might actually be significant as a more developed turning point (though it remains to be seen).

May 2021 was the spark of renewed COVID fear for that country, as anyone watching the Olympics is aware. That might be what’s going on locally, but not globally. Concerns over corona’s delta may be amplifying those already dating back to at least late February.

And those are not runaway inflation. The US CPI’s are the global outliers, supported by an even bigger one in US consumer binging (only in goods). The rest of the world just doesn’t look anything like those, and the consistency across these markets indicates a strong, getting stronger belief the American outliers will eventually converge with the world’s true (and sickening) baseline shape.

Not the other way around.

No, the Cabinet Office’s LEI isn’t truly a big deal. But that was really just a way to introduce all this other which is.

Stay In Touch