Stop me if you’ve heard this before. Longtime readers/followers/enthusiasts will be forgiven for immediately thinking I’m quoting myself again, as I so often do:

Following its emergence, the eurodollar market played a big role in the Bretton Woods system and also its breakdown and eventual demise in the early 1970s.

The primary reason I refer so much to my own work is that ever since the early eighties there’s basically nothing else out there. Believe me, I’ve spent years looking. Even after the worldwide financial and economic breakdown that was the first Global Financial Crisis, still zip. Zilch. Nada.

It’s not so much painful silence as a form of corruption, a very real sort of monetary omerta.

Only occasionally has the truth slipped out, and when it has it has immediately been buried purposefully under an avalanche of “subprime mortgages.”

No sir, the dots connect directly from the eurodollar’s emergence in the fifties to the Great “Moderation” that wasn’t so moderate sweeping its tidal wave of globalization over the planet to then its ultimate breakdown begun before “subprime was contained” until after August 2007 no longer resistible.

This was the Global Financial Crisis.

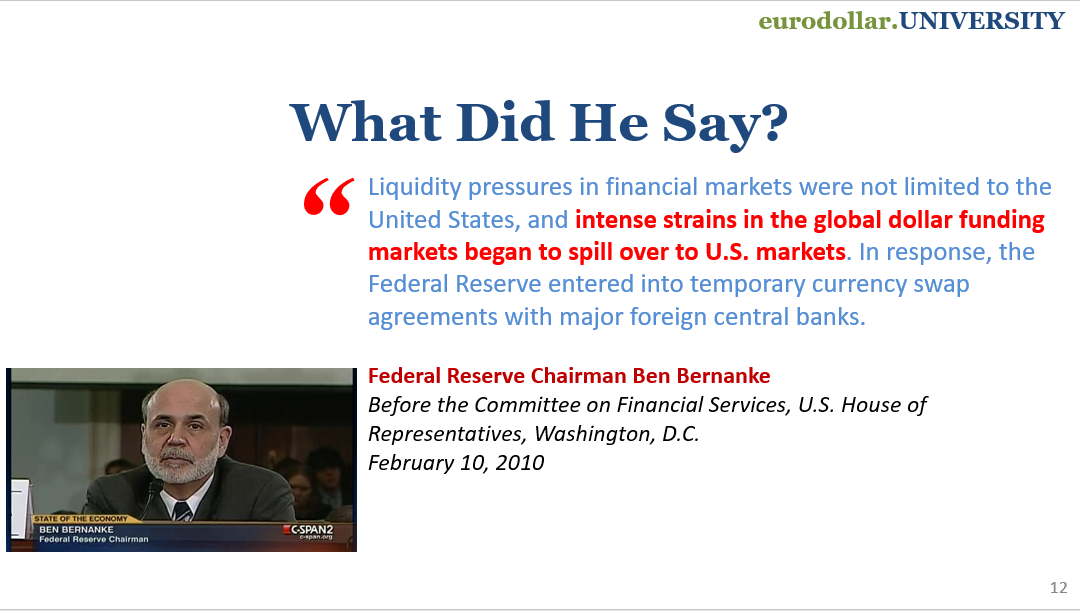

Liquidity pressures in financial markets were not limited to the United States, and intense strains in the global dollar funding markets began to spill over to U.S. markets.

Again, it sounds like I’m taking from my own body of work, or perhaps from something Emil Kalinowski has written and published. Nope. Even Ben Bernanke in February 2010 couldn’t say otherwise (though nobody, and I mean nobody, noticed or if they did they didn’t know how to properly conceptualize it). The quote immediately above was lifted from a Congressional transcript for when Chairman Ben had argued for why he shouldn’t be blamed and not entirely disqualified from a second term (thus, the “hey it’s not my fault” honesty).

Likewise, the original excerpt from up at the top isn’t mine, either. Nor Emil’s. It is rather a product of a couple researchers from the Federal Reserve’s St. Louis branch (big thank you to an unnamed, eagle-eyed, and equally resolute eurodollar fan researcher).

Yes, the Fed.

Pulling data from what the BIS had pieced together in the 1960s, the pair of authors briefly relate one of the eurodollar’s origin stories (out of several others) before explaining how offshore dollars “began to expand rapidly” and all long before August 1971.

To those who often visit here, absolutely nothing new. To the vast majority of the public, huh, what did you just say?

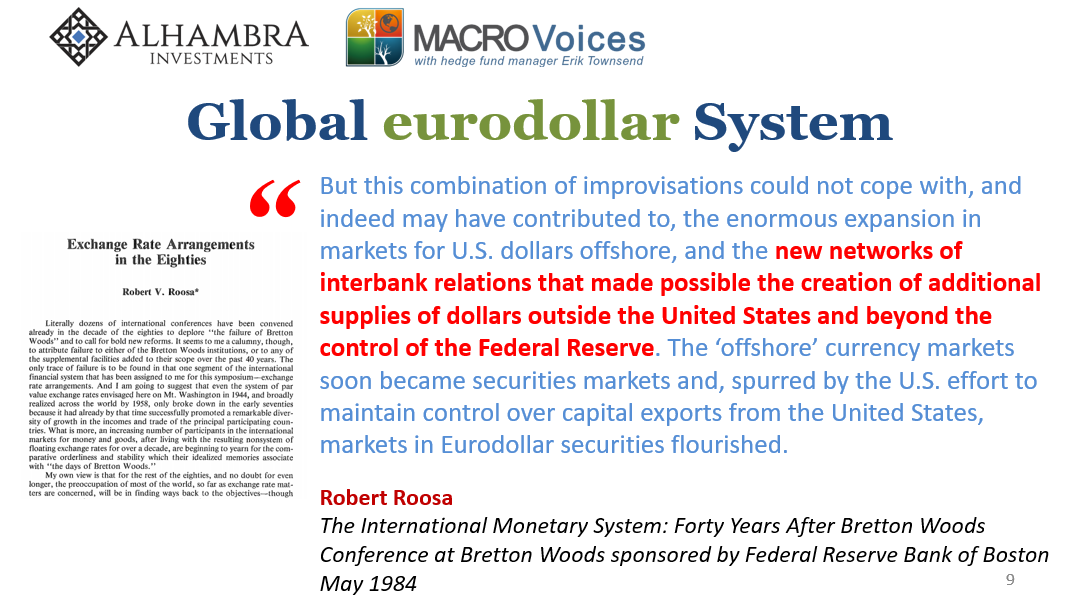

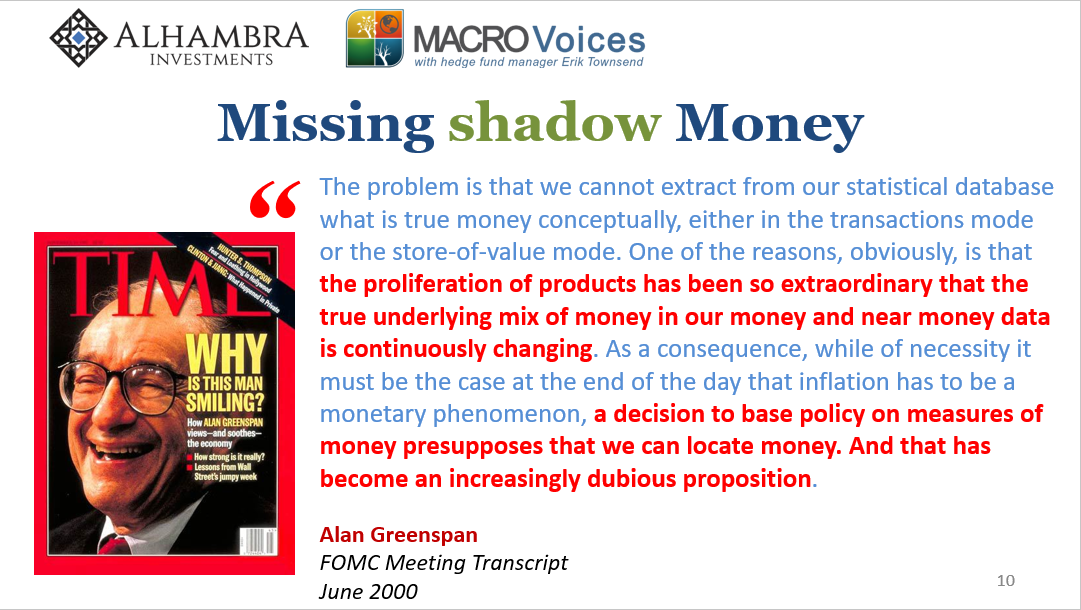

For of the very few Ben Bernanke confessions about “strains in the global dollar funding markets began to spill over” there precedes them this same blind spot of self-imposed ignorance found by Alan Greenspan’s “proliferation of products.” For the St. Louis Fed to have published but a few brief, cursory words about it in January 2022, there were those unheeded of Robert Roosa from 1984 having long since been buried and forgotten.

It is the dirty little secret of this American “central bank.” Why dirty? Because within the story of the eurodollar lies its catalog of how the Federal Reserve lost its monetary way, never regained it, instead relied on really dubious theory and therefore became something other than a central bank (see: Roosa; Greenspan).

To pick up the topic now at this late date – not just decades after the origin fact but also, more importantly, a decade and a half after it all went to hell and the system was given only useless QEs in the meantime – is a bit curious.

From what few conversations I’ve had in and around the place along with reading so much mainstream scholarship (too much, since most, but not all, is just a worthless waste of time) along with other sources of information, I can tell you there is a nascent organic desire to get at some level of truth.

What I mean is curiosity, as a start, from down at the staff levels way far away from the politics (and empty suits) of non-money monetary policy and its Enormous Lie. There’s a natural human impulse, a grassroots revolution to rediscover the basic fundamentals of reality.

Dollar shortage. Offshore. Not subprime mortgages. Couldn’t have been subprime. You can only keep screwing up so many times before those you’ve hired to do your work can’t take it anymore.

Eurodollar, not bank reserves.

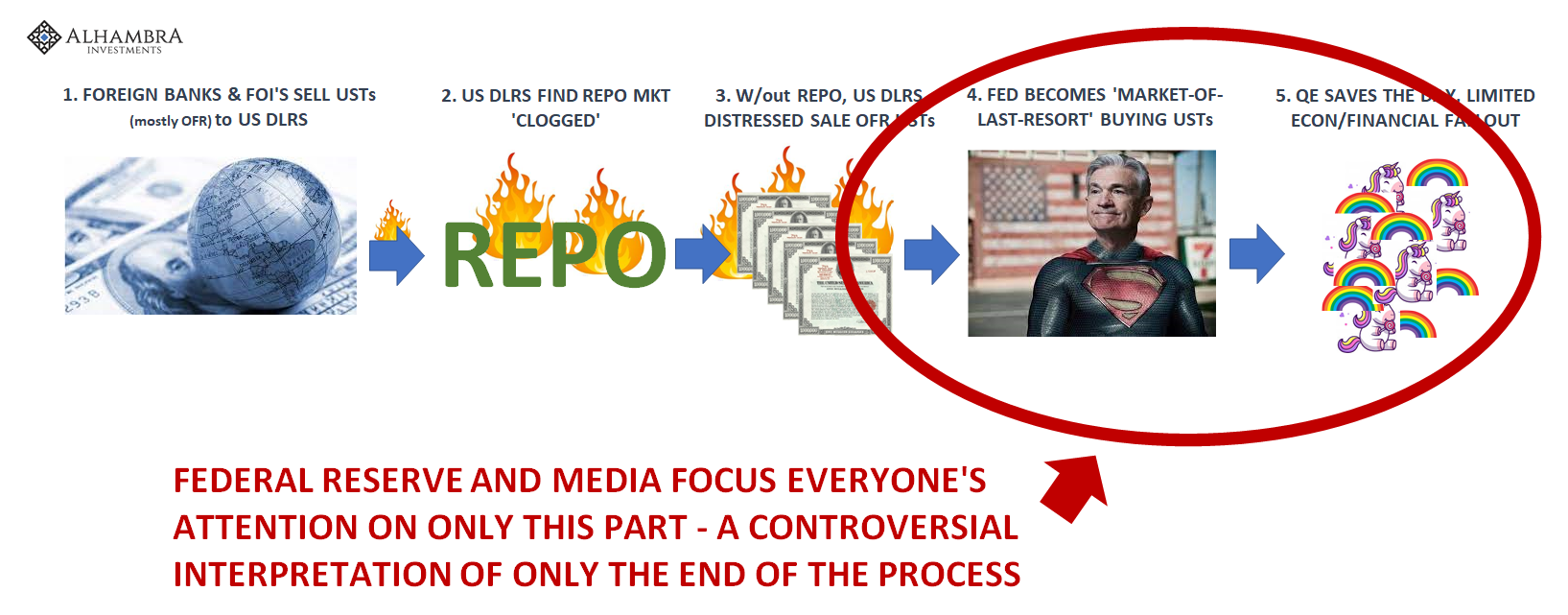

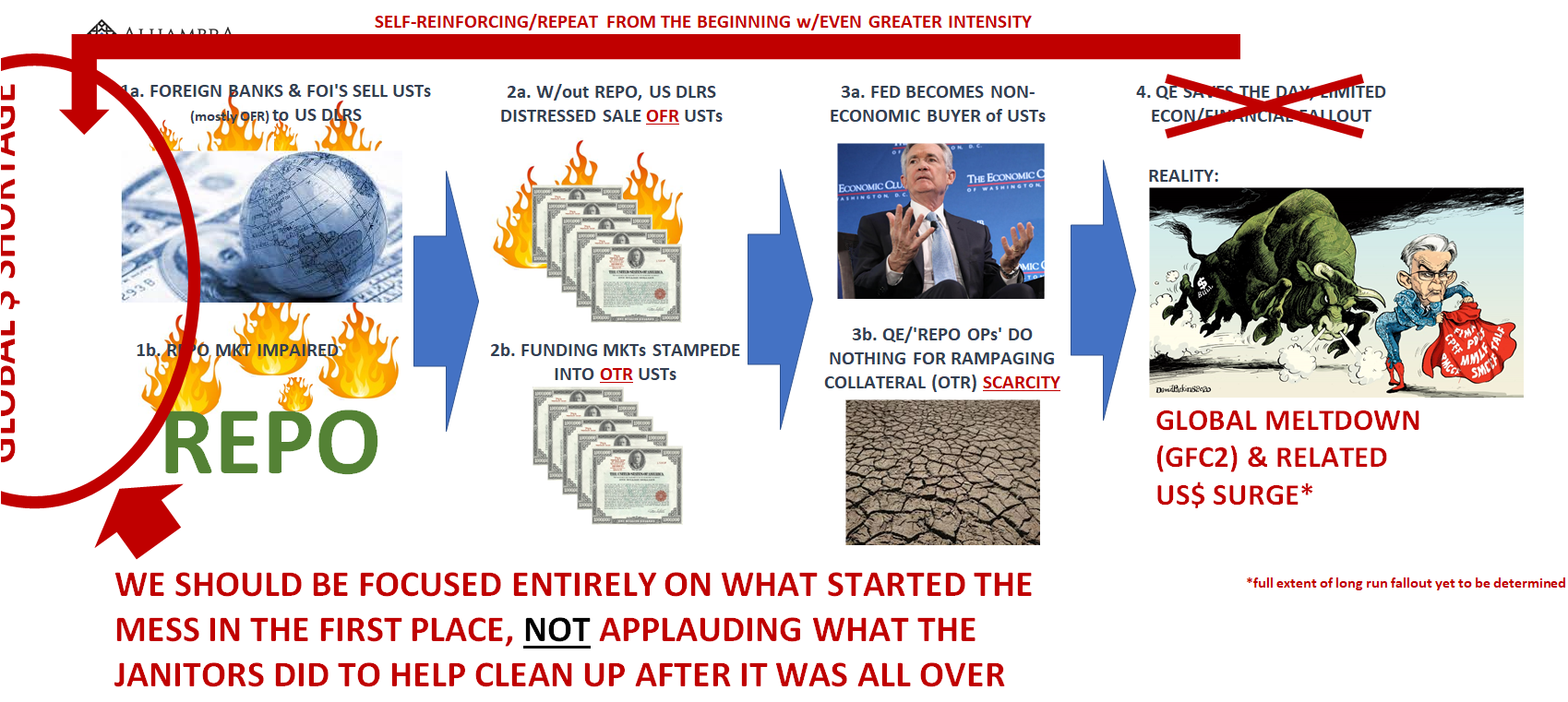

In fact, when you actually look at what happened just this last time – and I mean really and honestly look at it – the whole affair can only be classified as, “strains in the global dollar funding markets began to spill over to U.S. markets.” After all, March 2020 can only be hidden as a “breakdown in the Treasury market” for a little while longer before any serious analysis and review uncovers the real secret.

Yeah, like the first time the problems in the Treasury market the second time began from the outside, too!

Make no mistake, it remains nothing more than an occasional drip and drab; a few lonely pieces of genuine scholarship amidst an ongoing ocean of orthodox econometric echo-chamber.

Despite Jay Powell’s (bald-face lie) assertion in May 2020 of a global flood of digital dollars, last year, 2021, there was too much that didn’t quite associate that way. At the very least, the monetary story is increasingly obvious to be more complicated than QEs and bank reserves. They say flood, but, really, where is it?

Most of the public might believe it’s right there in last year’s CPIs, but any serious student of economics (small “e”) can see otherwise. And that would mean something very different for this year. And should this year turn out this way, it will leave practically everyone including the FOMC members to ask, where’d the money go?

It’s a question that has been asked for a very long time, it’s just nobody today knows this.

It is a matter of convenience vs. truth. A nominally-created central bank that isn’t actually a central bank and because it isn’t the institution has to instead play a central bank on TV, and to do so requires shutting down and shutting out this massive truth-telling. The cracks in the silence were always there, so eventually the whole story cannot help but spill out.

Unfortunately, we are a long way still from that day; untold future damage yet to pile on top of the incomprehensibly huge already experienced. Institutional inertia in this case is both criminal as well as understandable. Ben Bernanke was never going to get in front of the microphones and confess, nor will ever Jay Powell. It’s just too much all at once; the backlash assuredly epic.

A couple staffers here or there, an occasional (if self-serving) admission of the truth, those are going to leak. What ultimately matters is if when it does it does add something positive and good to the public understanding and breaking down of what is, and continues to be, the Biggest Story Never Told.

Quoting myself again, you really don’t have to take my word for it. But I do realize how there aren’t a whole lot of others’ words out there. At least, not yet.

Stay In Touch