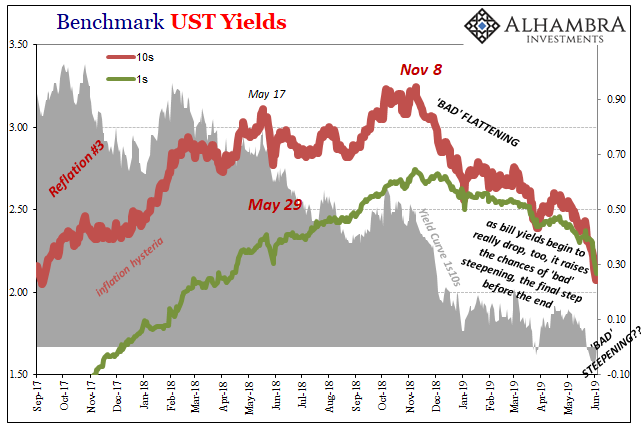

Normally, it’s a very good sign when the yield curve steepens. If longer-term rates are rising faster than those on the shorter end of the curve, it would say the bond market is forecasting a better probability of normal. Given where interest rates have been the last decade plus, this kind of steepening is what should’ve happened in 2017 if globally synchronized growth had been a real thing.

There’s another kind of steepening curve – the bad kind. This one is pretty much the best recession signal there is – not just the probability of it happening, but the high probability it has begun. Forget inversion, when you see the bad curve show up it’s all but game over.

In mainstream convention, they have these all backward. At least I think so. In Wall Street jargon, the bad curve is called a bull steepening. I don’t subscribe to the view there ever can be a bull market in bonds; that perspective seems pretty upside down given the accuracy of what is instead a liquidity indicator.

Therefore, to me what convention says is a bull steepening (for bonds) it’s actually a bear steepening. For everyone else outside of bonds, pretty much the rest of the world, when this happens it’s a really bad time.

This other curve case materializes when the short-end falls faster than the long end. That says the market is thinking lower money rates ahead, often a quick succession of them, the kind of result you just don’t see outside of full-blown contraction. The longer end more deliberately processes the negative repercussions of that sort of scenario.

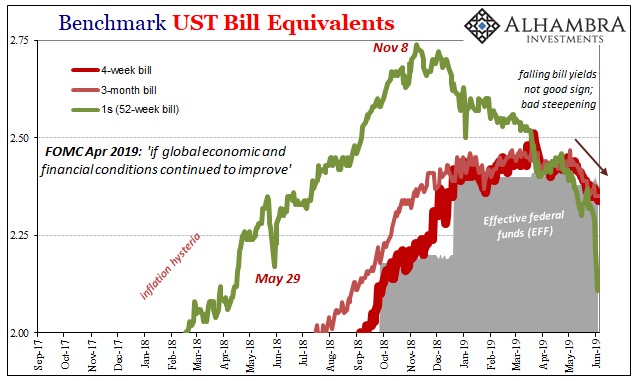

Bill yields have already begun their descent. To this point, they haven’t overtaken the long end so the curve remains flat and inverted – in key places. The 52-week bill, however, the equivalent yield on this instrument has plummeted the past few days. Even today when bond and note yields finally took a break and retraced somewhat, the bills were down (4w) or steady (3m, 6m).

It’s not my bear case just yet, though this is what you expect to see just before it. The bills are starting to mimic eurodollar futures and more forcefully price that series of rate cuts increasingly within the visible horizon.

What ultimately happens is the self-reinforcing processes show up; not the virtuous circle of recovery as in the good steepening, but the viscous cycle of contraction. Tighter money (rising liquidity risk) leads to economic uncertainty which feeds even tighter money that eventually, if left unchecked, creates the same sorts of feedback loops in the real economy.

Businesses get nervous and begin to rethink their plans, which causes other businesses to get nervous, and so on. If that keeps going, “rethink their plans” becomes downward adjustments and then eventually those spiral into outright cutting back no matter what.

What we call recession.

Since Europe has been on the leading edge of what is already well into a globally synchronized downturn, it was noteworthy that in yesterday’s IHS Markit’s Manufacturing PMI for the EU there was the first direct mention of some of those real self-reinforcing negatives. Chief Business Economist Chris Williamson wrote:

A fourth successive monthly drop in output and further steep decline in new orders underscored how the sector remains in its toughest spell since 2013. Companies are tightening their belts, cutting back on spending and hiring. Input buying, inventories and employment are all now in decline as manufacturers worry about being exposed to a further downturn in demand.

The new orders index has been below 50 for eight straight months and the unemployment index turned for the first time in 56 months; meaning that European manufacturers appear to have reached their limit. They held out waiting for “transitory” factors, as they are called in both the US and Europe, to dissipate as predicted by Economists and central bankers. They haven’t, so the self-reinforcing negatives may already have begun.

And though that is in Europe, it would certainly play a role in further confirming market risk perceptions globally. A bigger, more substantial downside is much closer.

No wonder Fed officials are now talking their two-faced position; strong economy but possible rate cuts to make sure it stays that way. A strong economy doesn’t require rate cuts, not for a group of small transitory factors, anyway. But if all the worst indications start to click into place at the same time?

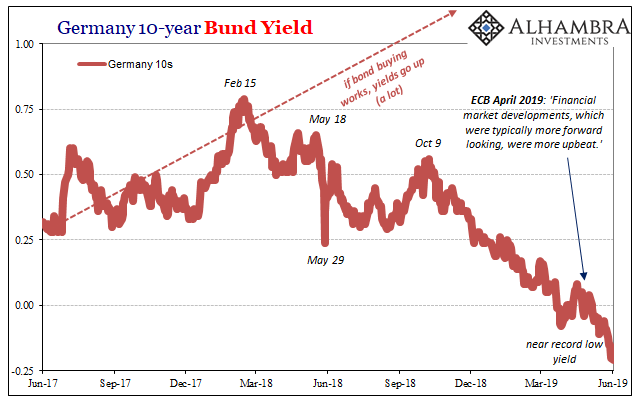

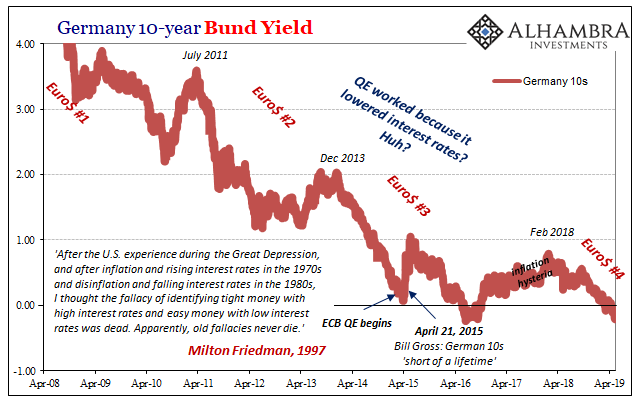

Since the global economy is, well, a global economy, clear recessionary processes which break out in Europe would likely be just the first confirmation. It would explain why German bund yields are a mere few bps off their previous record lows already and maybe also this first serious taste of the bear (bad) steepening in the UST curve.

Stay In Touch