At last week’s ECB’s press conference, the central bank’s President Mario Draghi was both downbeat and upbeat. As to the former, he acknowledged that Europe’s economy wasn’t working out the way they’d all hoped (and repeatedly promised). Despite the disappointment, Draghi wasn’t completely deterred.

This growth scare wasn’t really European, he said. China, trade, and a bunch of other things from outside Europe (offshore?) were to blame. And contained in that view was the good news as Mario Draghi sees it. He responded to one reporter’s question about a possible 2019 recession by reiterating the transitory nature of these unexpected issues.

At the same time, they [the ECB’s Governing Council] acknowledged also the underlying strength of the economy, the fact that some of these temporary factors are unwinding, and so it was a meeting where the main goal was to reassert the readiness to act if the contingencies would warrant so.

To ensure this soft patch doesn’t get worse, the ECB will offer a third T-LTRO and it has promised, essentially, to keep interest rates where they are for a lot longer. As noted earlier today, this has buoyed European sentiment of late. People especially Economists love dovish central bankers and love to project their surefire success.

While Draghi’s reassuring pabulum made for headlines and widely disseminated media content, not everyone over there at the ECB is so confident. Reuters reported yesterday the ECB President is facing growing opposition from within.

A “significant minority” of rate-setters in last week’s policy meeting expressed doubt that a long projected growth recovery is coming in the second half of the year and some even questioned the accuracy of the ECB’s projection models, given their long history of downward revisions, the sources said.

It has taken almost twelve years, but finally perhaps at least some officials are sick and tired of being on the wrong end of their statistical models – the same that always, always assume monetary policy is effective stimulus. When Draghi or Jay Powell for that matter blames outside, temporary factors for constantly “unexpected” weakness what he is really saying is that he has no idea why downside risks have materialized. All the models projected that there was no chance they’d be here.

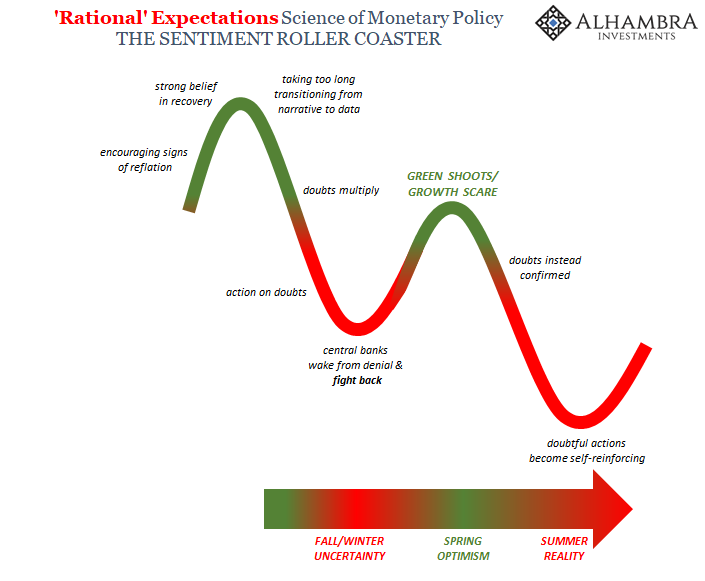

That is, I believe, what’s really behind the T-LTRO’s as well as all this global “dovishness” of late. In the central bank handbook, you absolutely have to have sentiment back on your side. In fact, the central bank manual declares that without positive sentiment you’re sunk.

That’s your 2019 dovishness. Unfortunately, the real economy doesn’t run on sentiment; which is why, as noted earlier, it never really works out – the “long history of downward revisions.”

It may be too late for 2019, but eventually hopefully before Euro$ #5 enough officials will start asking the right questions for once. What is it we keep missing?

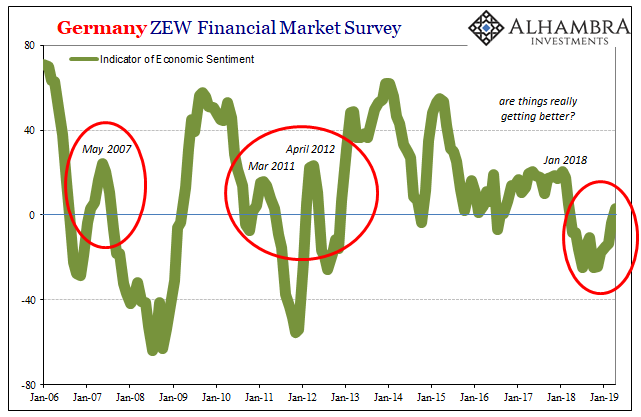

In the right light, the shoots may appear to be green. But when a “significant minority” of ECB policymakers, of all people, aren’t seeing it, you don’t just go back to adjusting the light. You shouldn’t, anyway.

Stay In Touch