It’s never just one payroll report. The month-to-month changes in the Establishment Survey barely qualify as statistically significant, let alone meaningful. What that means is one good monthly headline is nothing to get excited about, just as one bad month shouldn’t get anyone too worked up. May 2019’s jobs report, however, isn’t in isolation.

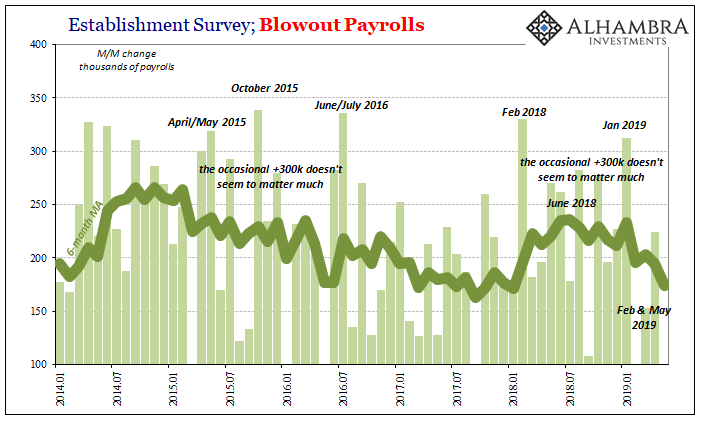

The headline for the Establishment Survey was +75k, well below expectations. On top of that, last month’s blowout (or what passes for one these days) estimate was revised substantially lower. Instead of +263k as first thought, the BLS now believes payroll growth in April was +224k. And it was only that much because March’s in-between figure was also revised significantly, down to +153k.

These three months follow February which still stands at just +56k. In short, employment weakness is beginning to show up across time. The 6-month average for the Establishment Survey fell to just +175k with May’s disappointment. It’s the lowest since the 2017 trough.

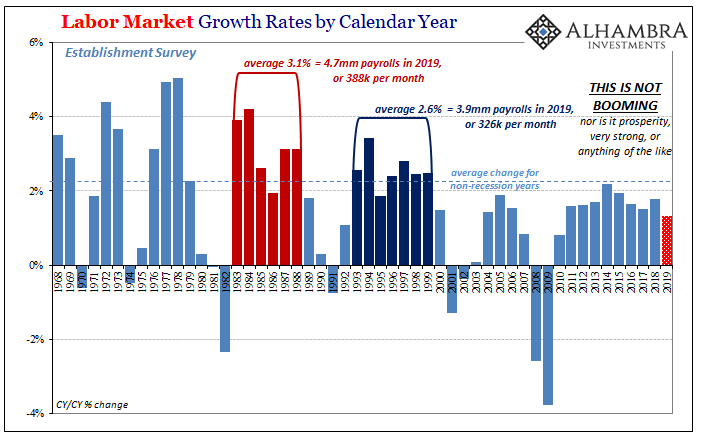

This raises the likelihood that even the highly adjusted BLS numbers at the top are picking up a change in economic circumstances. Calendar year 2019 is on track to be the worst since 2010, and we are only five months in. Whatever rebound in employment for and after Reflation #3, it has looked instead like the aftermath of an October-December global economic landmine.

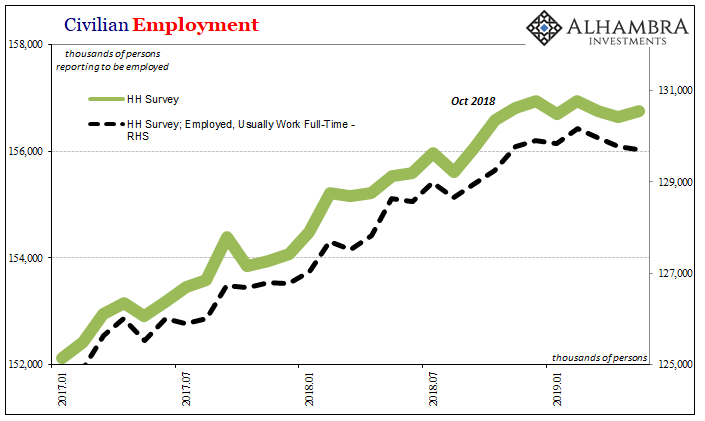

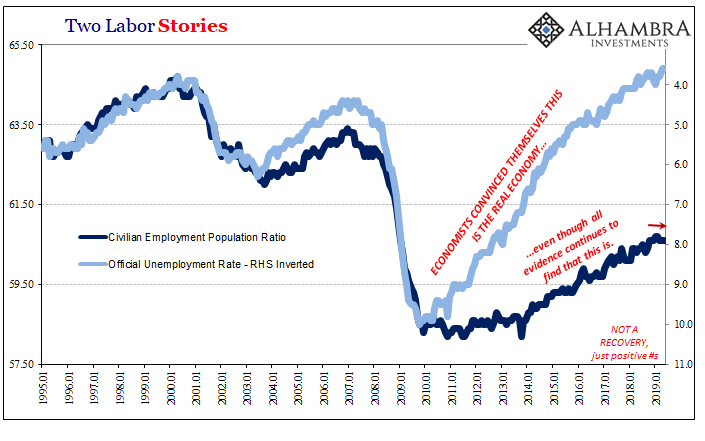

That much is already evident in the Household Survey, the BLS’s alternate main labor measure from which the unemployment rate is derived. While the latter remained steady at 3.6%, still the 50-year low, it’s clear that the HH Survey detects conditions very different from a boom-driven labor shortage.

This matches the change in trend captured by separate economic accounts from other government agency estimates related to jobs and employment. The BEA, for example, its figures on national incomes are consistent with the slowdown (or worse) showing up in these payroll reports.

As noted yesterday, this is not the product of trade wars. This is much deeper, already well-established, and extensive beyond a few billion in tariffs on Chinese goods. In the mainstream, like 2008 there is no alternate explanation given. In the absence of any credible theory, trade wars is what’s left.

And by the account of bond markets and money curves, this is all just getting started even though weakness has been apparent for a considerable amount of time already. The markets are suggesting all that was just the preamble, the warmup for the still-looming main event.

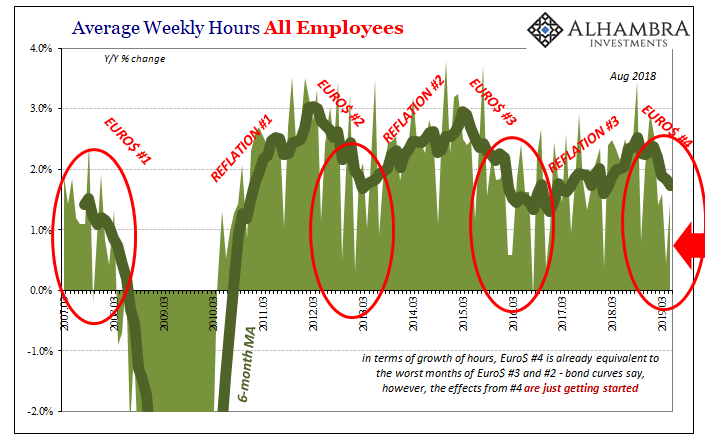

The BLS estimate for total hours worked in May 2019 was up just 1.5% year-over-year. Like the Establishment Survey, hours are also picking up more frequent bad months with lower downside variation. In April, hours had gained just 0.5%.

As shown above, this already matches the low points near the troughs of Euro$ #3 and Euro$ #2. With that comparison in mind, and with the bond curves where they are, this is why I’ve said Euro$ $4 is setting up to be nastier and more direct (as far as the US economy is concerned).

It’s not just one monthly headline. The concerning results are piling up all across the data. Powell and his gang keep saying the economy is fine and they’ll keep it that way with a rate cut or two as insurance. He makes this claim based on his view that the labor market is strong.

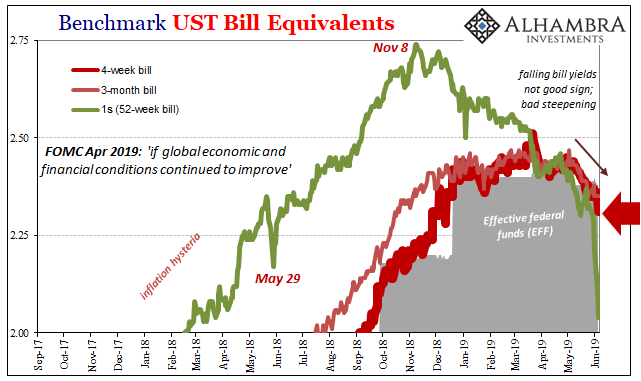

The bond market view, which has been consistent for more than just the last year since May 29, 2018, is that Powell is going to regret having depended so much on just that one labor market number; the unemployment rate. That’s ultimately all rate cuts mean to eurodollar futures, T-bills, and the like. Policy regret over really bad forecasting.

When the eurodollar curve first inverted by just a few bps last year, it was an important signal about probabilities. I wrote last July:

The shape of the current curve is saying the same thing now as it did in early 2000, only at such a diminished nominal level only a central banker could miss the curve’s primary message.

It’s the eurodollar, stupid.

The reason there is so much constant forecast error, especially the last ten years, is that one. That’s why there is no economic growth nor inflation risk as both the eurodollar as well as the UST curves flatten out far closer to zero than normal.

Jay Powell came into his office last February like a hawkish bull in a China shop believing that this had all changed, that guided by first Ben Bernanke and then given sufficient time under Yellen monetary policy had finally succeeded. The bond curves said, unequivocally, NO WAY; the risks of something going wrong in offshore money (the eurodollar, stupid) remained way too high.

By the time Powell was sworn in, the warnings to that effect had already started and many were already pretty loud. After May 29, that was likely the point of no return. It was the market shifting from something maybe going wrong to how bad will it get now that something has.

More and more even the labor data is becoming consistent with post-May 29. This cannot be overstated, the supposed last bastion stronghold of US economic strength. Instead, a few months after the events of May 29, the global economy seems to have struck the landmine. The US hasn’t decoupled, the American labor market isn’t even “strong.”

The Fed was still “hiking” while eurodollar futures were increasingly betting they would reverse course not of their choice.

Rate cuts as insurance? Rate cuts as mistake. A big one. Put the headline and details of the May 2019 payroll report as well as the others recently solidly into the column of “not of their choice.”

Stay In Touch