The FOMC yesterday reiterated their stance that the economy was strong. But they also hedged. A one-and-done rate cut is one thing, some insurance (allegedly) for keeping the good times rolling. What about QT, though?

That’s the funny thing that you can’t help but get stuck on. Not bank reserves, mind you, they’re worthless (perhaps literally). Rather, Federal Reserve officials appear to be experiencing that sinking feeling, too.

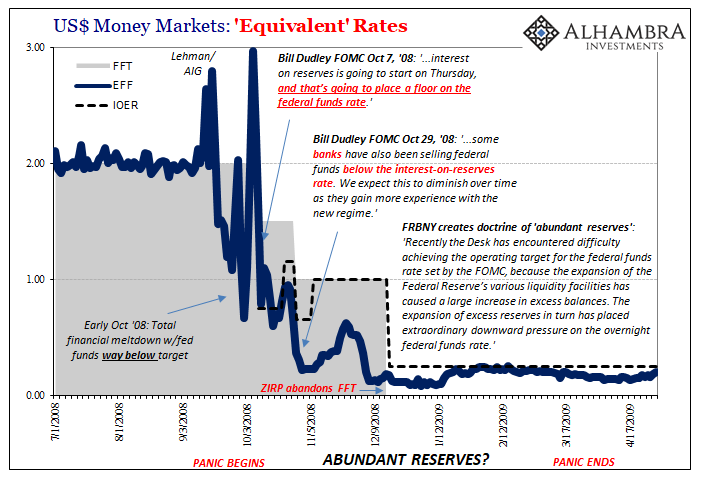

QT was supposed to continue unabated until the level of reserves were scaled back almost all the way back to zero. There were practically no bank reserves before 2008 (an important fact that almost no one stops to think about) and normalization might necessarily mean just that.

There has to be some level of raised reserves, though. The Fed operates monetary policy a little differently, and there’s also other incidentals to consider (things like the foreign repo pool, ironically). So, it was always expected that QT would take things closer to the pre-crisis era but not go all the way.

And it was never expected to be a big deal. Keeping it in very broad terms, policymakers believed the Global Financial Crisis impaired the private dealer system (it did) because of subprime mortgages (nope) and the Fed stepped in to admirably and adequately fill the gap with its own balance sheet (not even close). This is, essentially, the doctrine of abundant reserves.

It wasn’t supposed to be permanent. At some point, once the world got over the GFC the Fed would hand monetary responsibilities back to the private system. This was the whole point of QT – to get these liquidity functions back in the hands of private dealers.

The FOMC used the occasion of globally synchronized growth as that jumping off point. Had it gone according to plan, no one would’ve noticed QT or the level of bank reserves. For however much the Fed would ultimately subtract in the form of balance sheet unwinding and therefore lower levels of reserves, the private system would add back and then some.

Dealer banks would easily pick up the slack. And why wouldn’t they? The world was suddenly full of inflationary growth and opportunity again.

Ending QT prematurely admits that something was off. It says that officials are wondering if level of bank reserves “needs” to be much higher than anyone thought. Ending it abruptly yesterday, another two months ahead of a deadline already hastily imposed, this says that there is some substantial concern in this area. As I write for RealClearMarkets publication tomorrow:

They’ve decided the system really might need a whole lot more reserves than they ever had planned for. In Jay Powell’s thinking, maybe there is something wrong that more reserves might fix.

Another way of saying that?

The world really does seem to be short of dollars.

So, what does the bond market think of all this? After all, it was the eurodollar futures curve which first told Jay Powell he was going to cut rates in 2019. Back in June 2018, the Fed had just upgraded their economic outlook (to very strong) while the curve inverted. The mainstream laughed at the crazy, stupid notion of rate cuts.

Bonds 1, Powell 0.

Yields have plummeted today in the aftermath of yesterday’s symbolic show of confidence. Eurodollar futures are being bid like there is a shortage of contracts. Not only does that say “one and done” is a dream, it also indicates the bond market isn’t taking bank reserves and QT seriously. Why would it? QE was nothing more than smoke and mirrors, a full-on puppet show.

This, of course, should not be surprising but it is news to pretty much everyone including FOMC policymakers (who don’t understand bonds).

The closer you are to the nuts and bolts, the details of design and operation, this view [rate cuts as stimulus] doesn’t hold. In other words, if you are operating within close proximity to the sausage making in money and economy, then you haven’t been able to ignore the ineffectiveness of rate cuts before the ineffectiveness of everything else. There is no “trust us” basis down here in the trenches.

What the bond market has been saying for way more than a year is, you better step up to some real liquidity and money – or else. We’ve moved much closer to “or else.”

The Fed has responded instead with a rate cut and a far higher terminal level of bank reserves. The central bank agrees the world may actually be short of dollars, but they aren’t going to, or can’t, do much about it.

Sure, one and done.

Stay In Touch