In every likelihood, the Federal Reserve today is going to join other central banks around the world who have already cut rates. It is the synchronized signal completing the turn from globally synchronized growth into a globally synchronized downturn. To most people in the United States, at least, this is a puzzling shift.

The unemployment rate says things are rock solid. Only seven months ago, the same Federal Reserve officials now voting for “additional accommodation” were then expressing very different sentiments. Hawkishness was the order, inflation and economic acceleration befitting what would shortly become the lowest unemployment rate in a half-century.

It is fortunate and timely that several pieces of forward-looking data are speaking on Jay Powell’s behalf before the public release of the FOMC statement.

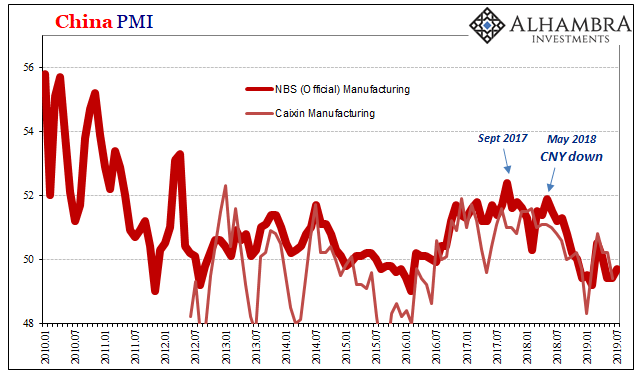

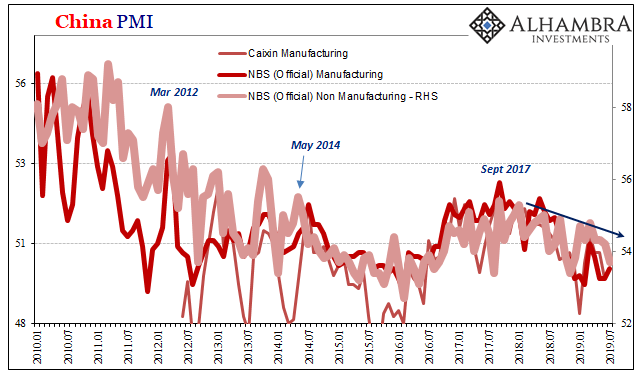

The reasons began last night, as usual, in China. That country’s National Bureau of Statistics (NBS) reported more concerning figures on the economy. Coming in at 49.7 in July 2019, the “official” manufacturing PMI remained below 50 for the third straight month. It was also the sixth time in the last eight. Going back to last October, only once (the green shoot of March) has the index been better than 50.2.

The PMI is already indicating conditions equivalent to the worst parts of 2015-16, which in China was a time when its officials panicked into fiscal “stimulus.”

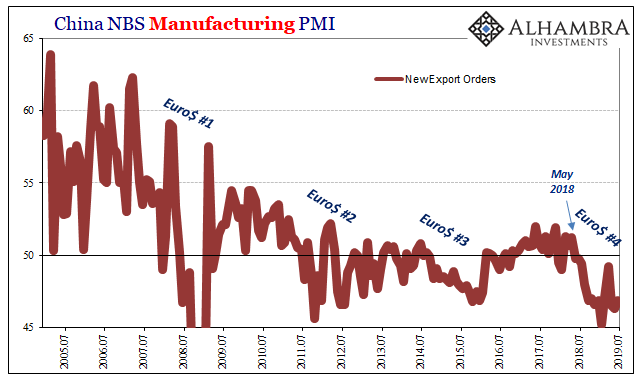

At the forefront of this persistent weakening trend is China’s export sector. While many people are quick to blame “trade wars” and geopolitical tensions more broadly (sentiment fearing trade wars), there’s just too much here to make it exclusively about a few billion in tariffs. There are much more powerful negatives weighing on a lot more than sentiment.

The timing of the shift also suggests the real cause. The whole global goods economy was rocked back in May 2018 – specifically the 29th.

Outside of manufacturing, the NBS Non-Manufacturing PMI was lower, too. At 53.7, July’s estimate was the weakest since November – which also makes it more like 2015-16 than 2017 and the expected continuation of globally synchronized growth.

What does this have to do with the FOMC vote? It’s easy to think China’s problems are for China to deal with.

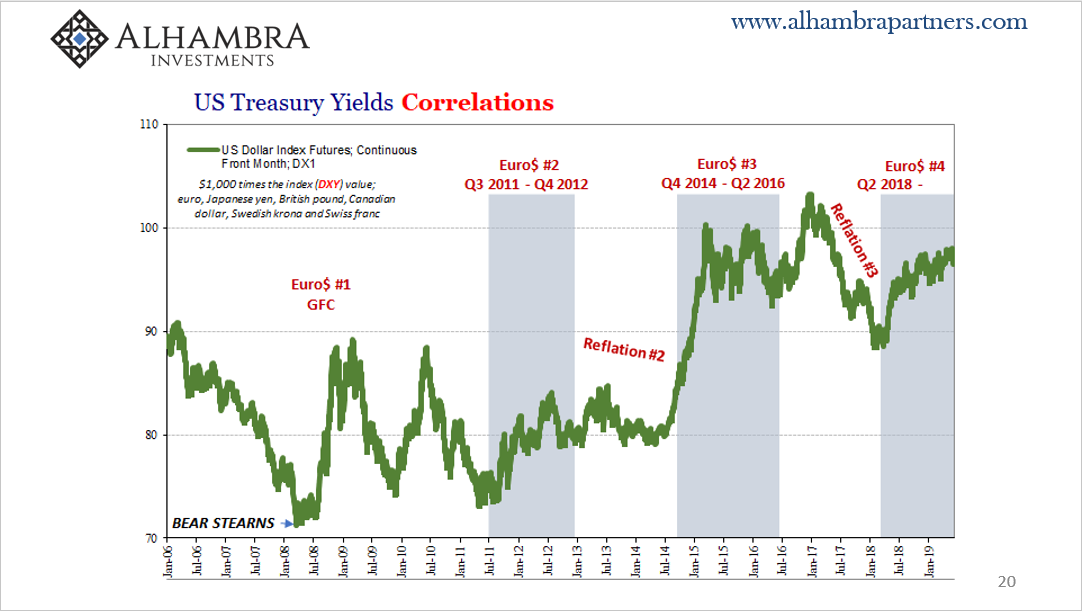

As I said earlier this week revisiting with Erik Townsend and MacroVoices, the correlations make it obvious. It isn’t one thing or another in isolation. Whether by market or by economic data, there is a uniformity across all sorts of indications in so many places around the world which make it very clear what’s really going on in the global economy.

And because this is the fourth time these correlations are being repeated even central bankers and some Economists haven’t been able to just casually dismiss “overseas turmoil.” A few have even taken note. At this point, it is exceedingly difficult not to notice and appreciate the consistency.

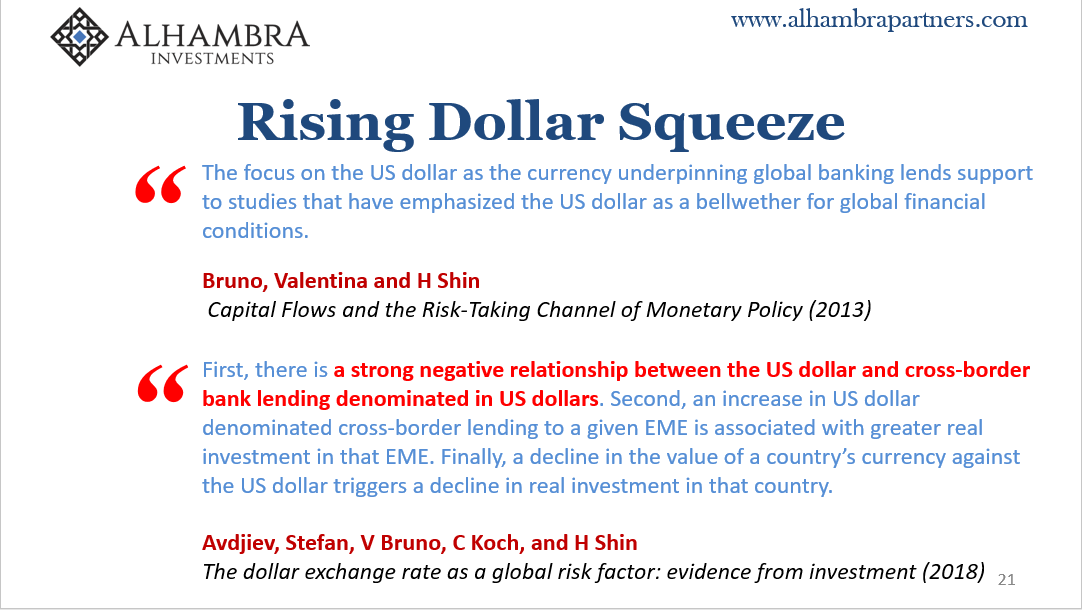

As Chairman Powell, of all people, said recently:

The global nature of the financial crisis and the channels through which it spread sharply highlight the interconnectedness of our economic, financial, and policy environments.

What are those “channels through which it spread?” It’s difficult for officials to say it in straightforward plain language, or just to whisper the words quietly to themselves, but they can at least dance around it by copping to its effects. I say it is a eurodollar squeeze but the term dollar shortage will work fine.

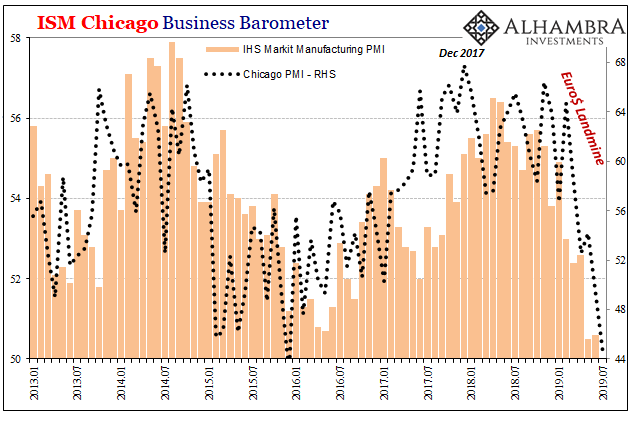

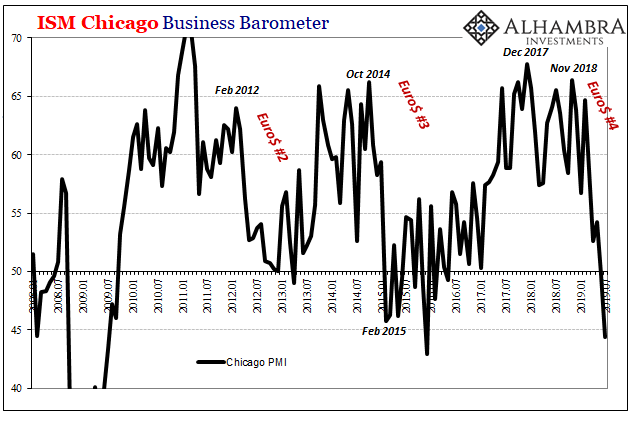

And to drive that point home, the ISM’s Chicago bureau provides the Chairman with a very poignant, close-to-home bookend to China’s PMI data. The institute’s Chicago Business Barometer, an important regional PMI subset, collapsed to 44.4 in the latest estimate for July 2019 (also released earlier today). It was the second worst month since 2009.

What really matters is not the sharp decline in July or even this one PMI. It is, again, consistency and correlations. The Chicago BB merely repeats and further confirms what other data already suggest. The global economy, the US very much included, is heading in the wrong direction right now.

That’s already enough for the FOMC to justify a rate cut (though still mistaken in believing the rate cut will do anything to arrest the decline). But what should really worry officials at the Fed as well as around the world is that this PMI behavior is what happens toward the start of a downturn – not at its end.

During Euro$ #3, the Chicago BB, as other PMI’s, fell sharply starting in late 2014 before completing the shift in early 2015. The “manufacturing recession” followed that change in sentiment, not hitting its worst points until much later in 2015.

This would suggest we won’t see the full extent of the real damage done by the latest squeeze/landmine until later this year. When the same thing happened early in 2012, Ben Bernanke’s Fed responded with QE3 in September and QE4 in December (there were four QE’s, not three).

Far be it for me to defend the Federal Reserve and their motivations behind a rate cut, but this is a global economy problem not a US economy one. It only seems overwrought and unjustified to the public who has been taught and told the US is an island and the unemployment rate is the only true barometer for conditions on that island.

A lot of the world economy is already in rough shape. Only some of that rough stuff has begun to show up here. If the Fed seems a little panicky it’s because they have every correlation to be.

Stay In Touch