Rhetorically, I wondered yesterday what it was that economists and the media were actually looking at when opining about certain economic topics. That was in relation to German factory orders which are clearly moving in the “wrong” direction, to which that is supposed to be set aside in favor of “sentiment” and the ephemeral “confidence.” Neither of those words really apply here, just as they haven’t much in many years, as what it all really amounts to is rationalizing some form of monetary policy. A central bank does something, especially of significance, and it is just accepted that it will work.

This morning we get a companion to German factory orders in German industrial production. It was ugly, and undeniably so – or so you would think. But here is the Financial Times describing, in as little detail as possible, how this is great news for Europe.

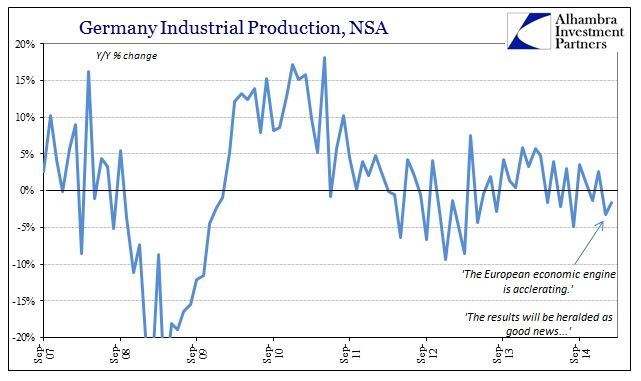

The European economic engine is accelerating.

Industrial production climbed 0.2 per cent in Germany from a month earlier, eclipsing expectations for a 0.1 per cent gain, as the production of energy and capital goods rose, according to the latest figures from the Bundesbank.

As if to totally confirm the monetary bias and the above rationalization, they end the short piece with:

The results will be heralded as good news from the European Central Bank, which announced in late January plans to unleash a controversial easing programme. While the €60bn a month bond buying scheme went into effect in March, word of the programme led to an increase in business confidence, including several manufacturing surveys which have climbed.

Germany’s IP figure was for February (whereas yesterday’s factory orders were already into March) so to tie it all to QE the FT has decided that the mere announcement was enough in January. Therefore, everything that comes after must be really good because QE, apparently, cannot fail even from the moment of conception.

What really happened in Germany was atrocious. The adjusted figure, which includes the standard ARIMA-X seasonality from the US Census as well as a trend-cycle component (more on that below), was indeed +0.2% over January. However, that increase only took place because January was revised from +0.6% to -0.4%! An entire percentage point was taken off January and February was only marginally better, but the FT wants you to believe there is high acceleration and that QE is already working.

There are rationalizations that we have come to expect and then there are blatant forms that are so transparent as to question why they even bothered to attempt it. Away from the adjusted figures, German IP was 1.6% below February 2014, coming after January’s serious decline of 3.2% year-over-year (second derivatives: February was declining slower, so that equals acceleration).

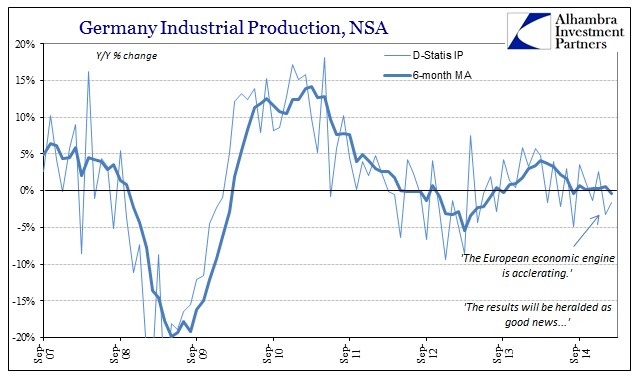

The argument for acceleration was thin before, but in this context it is nowhere to be found. Ever since about June, that “dollar” again, there isn’t much doubt as to which way industry in Germany is heading. This is itself an “unexpected” outcome because the weaker euro is supposed to be a huge boost (and it was if only to German exports, which again suggests that Europe isn’t actually faring well internally). To emphasize that even more, the 6-month average is now negative again, as this latest retrenchment is quite visible and obvious.

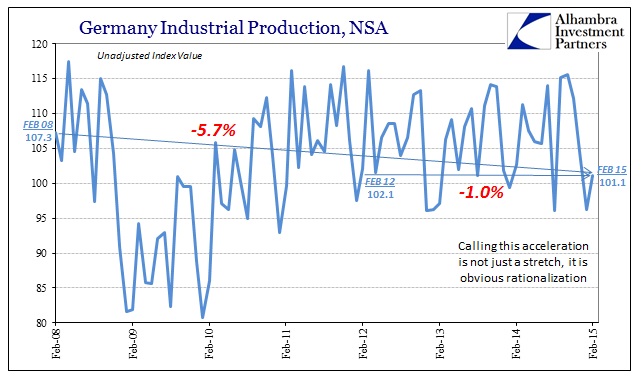

In this wider context, the pattern that emerges is not anything favorable to even a single month. Comparing February 2015 to prior February’s shows just how dire the situation in Europe actually is. German IP in this latest estimate is actually 1% below February 2012, and an astounding 5.7% below February 2008. Acceleration is not a word that should properly be associated with anything here.

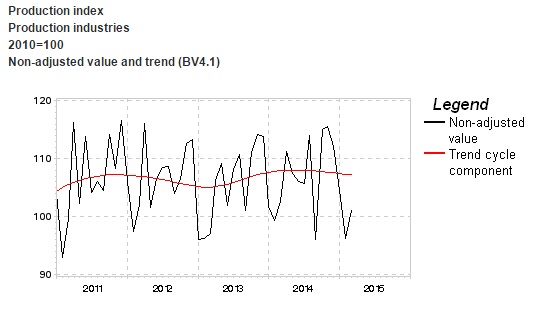

This data is completely and comprehensively bereft of anything that might be heralded by even those just slightly biased toward QE. Further, the Statistisches Bundesamt helpfully provides their breakdown of trend-cycle, unlike the BLS’s numbers from which we can only infer by the divergence of their output from everything else.

The trend-cycle adjustment to the final month-to-month variation is still nearly as high as it has been in the entire post-2009 period. Like everything else of developed economy statistics, this shows yet again that the mainstream and orthodox interpretation of cycle, which boosts actual figures and estimates, is not at all appropriate. Compare the trend-cycle estimate to everything else, especially from 2012 onward, and you can plainly see that they have it entirely backwards – the trend is not rising post-2012 as it is clearly falling and all over the world.

That means that the “heralded” +0.2% is as much trend-cycle statistical guessing as actual growth and, indeed, acceleration. I understand that the FT is a mainstream outlet with an interest in maintaining the monetary status quo, but you would think that a truly rational interest would wait at least a few months for actual confirmation before jumping fully and headfirst into the QE pool.

Maybe this aggravation is related to the fact that QE hasn’t worked anywhere else, failing quite obviously right now in Japan with even the US finally falling under a serious cloud of suspicion. In other words, there is the same “rational expectations” reason for trying to get ahead of the curve and make everyone believe QE can work before it actually does. That is, after all, the way modern monetary policy is crafted, to “influence” rather than actually accomplish anything. In terms of Germany and its industry, that is abundantly clear by absence of actual progress for years (which includes the enormous and prior ECB “solutions”) and the fact that March factory orders are already sadly still captured by the same decay.

Stay In Touch