Crude oil prices are being slammed again today, as the “dollar” continues to reek about the places where economy and finance come together. Crude oil is perhaps the most visible extension of that process, where finance helps figure out direction of prices that will eventually be necessary to physically clear (even and especially to storage) actual product. Given the position of energy in the actual economy, the centrality of it all leaves behind understatement.

Despite all protestation that has continued about the state of the “transitory” risks, the “dollar” has been dead certain about where all this was going. While economists continue to contribute to the myth about QE and “stimulus”, the “dollar” was both unimpressed and equally overwhelming. In some ways, it is a self-fulfilling mention as “dollar” characteristics become “real” in various facets of the real economy, far beyond just the domestic shores of what was once the dollar.

Even Europe, with all its 2015 QE newness, is tracing out so far exactly that financial path. The year started fairly poorly, unleashed Draghi’s long-restrained imagination, and seemed to be heading quite as intended – but only to be dashed yet again on this side of summer. While that “something” may elude the understanding of limited (and limiting) central bankers, it is nothing more than the “dollar” and its waves working in all things such as crude oil.

Euro-area economic growth unexpectedly slowed in the third quarter, underscoring the vulnerability of the region’s recovery as the European Central Bank examines the need for fresh stimulus…

With a slowdown in emerging markets testing the strength of the pick up in the currency union, the data will provide ECB President Mario Draghi with more visibility heading into December’s monetary policy meeting. The central banker has signaled additional stimulus is in the pipeline, citing renewed downside risks for growth and the region’s inflation outlook, which risks becoming entrenched well below the ECB’s goal of 2 percent.

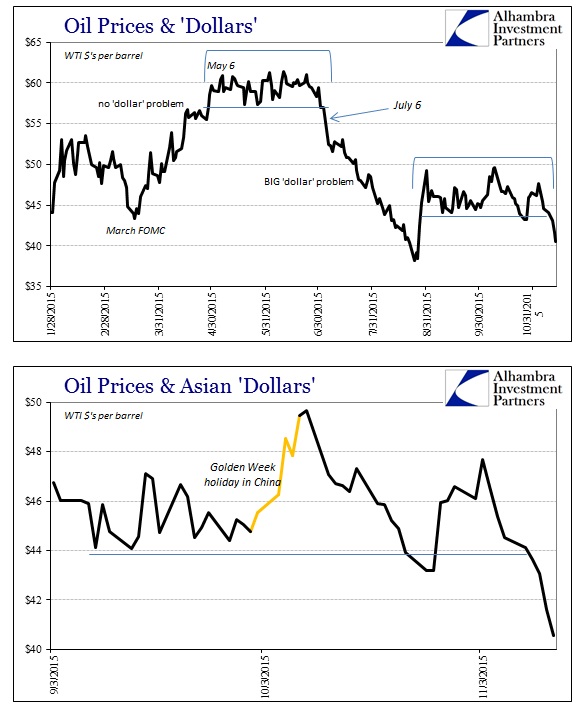

The “slowdown in emerging markets” is just the most obvious effect of much more direct “dollar” influence. The US has been conspicuously no different, as this morning’s retail sales confirm. The summer was mildly better than the winter, but the autumn harkens back to the cold even though it has been dispatched as overly warm (in Europe, somehow, too). It’s as if oil prices are the temperature of the “dollar’s” inverted “heat.”

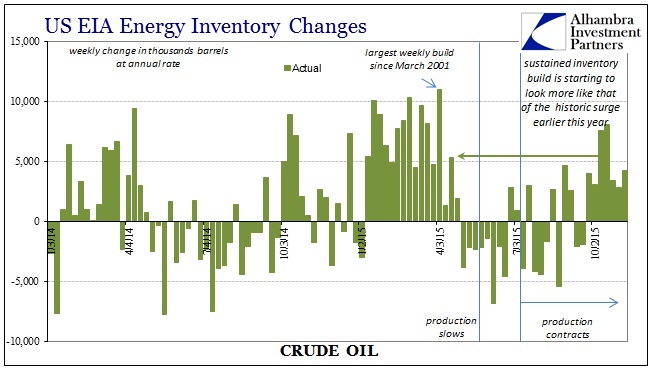

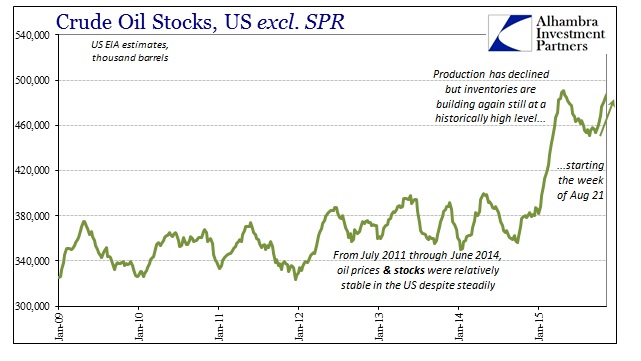

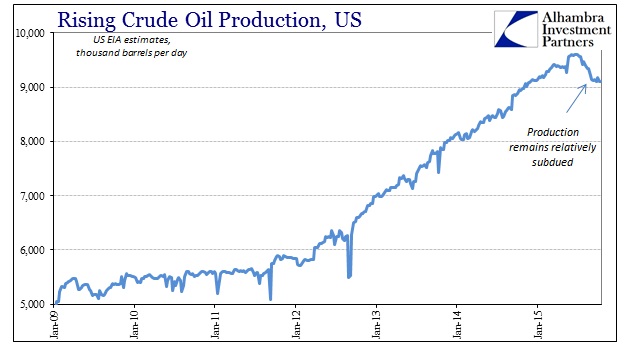

The WTI futures curve has flattened out and sank again, becoming in the past few days uncomfortably close to the August 24 extremes. There is no “stimulus” that can apply a wedge to that as it forms expectations for economic function that continues to conform. Not only are oil prices sinking again, dating back toward China’s on or off influence, they have done so apparently in good and proper anticipation of, at least in the US, a sudden and sharp renewed slowdown in demand. Oil stocks (inventories) have surged of late, pushing up to 80-year highs once more despite the fact that production cuts from the summer, the first “dollar” wave’s remnant effects, have largely held.

It took a massive and global “dollar”-led liquidation in mid-August to push the WTI curve as flat and alarming as it did. Thus, that was just a warning about what was to come, being confirmed in these later weeks by similar action without the intensity and fury; a sign more so of registered if reluctant acceptance that the recovery might truly be dead and “transitory” was always no great concern for the basic and established “dollar” baseline.

In a financialized economy the retreat of basic finance is economy, meaning the “dollar” is as demand (in future tense). As I wrote a few days ago, “Math is money; and where there is less reliable math, there is less money and then geometrically less patience.” Oil proves that yet again, pivoting between the math of modern money and actual, physical economic existence.

Stay In Touch