As the Chinese yuan continues to sink lower in what looks to be an increasingly uncontrolled fashion, the desperate linking of that to US interest rates becomes even more absurd. As shown yesterday, global currencies have run into great trouble with US rates moving higher and lower; in fact more so with lower US rates than higher. The connection between bond markets or any markets with currency markets is “dollars.” Liquidity is perhaps too imprecise of a term, an error that I am quite guilty of making, when in reality we are talking about money supply. The “rising dollar” remains a euphemism for “dollar” shortage, a clarification that does need to be made consistently.

The modern global currency system makes the very idea of money a fungible concept in ways that economists who first dreamed of fungible money never could have dreamed. This has led to an enormous problem of interpretation, from economy on in. To that end, I have charged the economics profession, especially those in positions of influence and actual authority at central banks, with reckless dereliction of duty. It was decided long ago that money was no longer a topic worthy of honest inquiry because, in truth, it had become too complicated. Yes, Economists in the 1980’s and thereafter had turned just that lazy.

Faced with global currency crises that just won’t end no matter which way interest rates go in the US, again where the dollar is supposed to be anchored, some economists, including a (very) few Economists, have begun to examine themselves and their dearly held beliefs. If the world looks and acts like it is besieged by an interminable dollar shortage, then maybe, just maybe, it is.

What you see immediately above is that shortage, or at least one of its primary manifestations. The chart was put together by one of the few who “gets it”, Paul Mylchreest of ADM Investor Services in London. It shows very plainly a very basic contradiction with traditional money theory, something that was supposed to be impossible, yet it lingers month after month, several years already.

He has blended the basis swap premiums across several major currencies. If there was a highly negative basis swap for just Japan, for example, you might be tempted to allow that as purely Japanese in nature; it would be perfectly understandable to assume so since the Bank of Japan the past few years has done an exemplary job of destroying money markets in yen. Some spillover into FX would not be out of line. You could make the same case if it were just Europe, especially given the status of Deutsche Bank and the Italians from Monte Paschi on down. But the negative basis swaps are negative all over the world and all against the dollar. I wrote back in March that the persistence and universality of them cannot be any other reason:

Any speculator or bank with spare “dollars” could lend them in a yen basis swap meaning an exchange into yen. Because you end up with yen you are forced into some really bad investment choices such as slightly negative 5-year government bonds, but that is just part of the cost of keeping risk on your yen side low. Instead, the real money is made in the basis swap itself since it now trades so highly negative. The very fact of that basis swap spread means a huge premium on spare dollars; which is another way of saying there is a “dollar” shortage. Because of the shortage and its premium, you can swap into yen and invest in negative yielding JGB’s in size and still make out handsomely. There has been, in fact, a rush of foreign “money” into Japan to take advantage of this dollar shortage; the fact that there has been such enthusiasm and it still has not alleviated the imbalance proves scale and intractability. [emphasis added]

Faced with such irrefutable evidence of “something” very wrong in global money, some have chosen to bury their heads once more and claim it must not be a problem at all. Others, again a very few at this stage, have finally started to wrap their heads around the fact that money is a very different thing than they have been taught and believed all this time. This is a discussion that should have taken place at least by 2009, if not August 2007. Better late than never, I suppose.

It is the closest thing to a physical law in international finance (e.g. Obstfeld and Rogoff 1996, Krugman et al. 2015), except that it has been consistently violated for almost a decade now. Textbooks, it seems, will have to be rewritten.

That was written in September by some BIS monetary officials. The “it” they refer to is covered interest parity (CIP). By the most basic assumptions about how the monetary world functions, the “physical law in international finance” as the quoted passage above claims, Paul’s basis swap chart just should not exist; in fact, like negative interest rate swap spreads that first appeared in late 2008, they were thought impossible.

It should have been a clue that monetary economics is flawed in its very core philosophies, but instead the topic was set aside and ignored for years – until this year when Economists could no longer escape not just the pure logic of it, but more so all that had already meant in terms of economic damage already suffered by the global economy because of it. I wrote my first full-length report on August 1, 2007, just a little more than a week ahead of the fatal break for eurodollars, entitled Why The Shadow Credit Market Is Failing; How Wall Street Has Done It To Us Again. It is fair to ask “what took so long?”

Just last week, the BIS published yet another paper (thanks to Jason Fraser of Ceredex Value Advisors for sending this to me) on the subject that gets closer to the observable truth that we had figured out almost a decade ago.

A stronger dollar goes hand-in-hand with bigger deviations from CIP and contractions of cross-border bank lending in dollars. Differential sensitivity of CIP deviations to the strength of the dollar can explain cross-sectional variations in CIP arbitrage profits. Underpinning the triangle is the role of the dollar as proxy for the shadow price of bank leverage…

CIP is perhaps the best-established principle in international finance, and states that the interest rates implicit in foreign exchange swap markets coincide with the corresponding interest rates in cash markets. Otherwise, someone could make a riskless profit by borrowing at the low interest rate and lending at the higher interest rate with currency risk fully hedged. However, the principle broke down during the height of the 2008-2009 crisis. After the Great Financial Crisis (GFC), CIP deviations have persisted and have become more significant recently, especially since mid-2014.

This is exactly the point I was making in hugely negative yen basis swaps back in March. We know what it is by its absence, by the fact that “someone could make a riskless profit by borrowing at the low interest rate and lending at the higher interest rate with currency risk fully hedged” but nobody was doing it! While this is a very complex issue, analyzing it from the proper orientation makes it very simple. Even the BIS gets to the heart of the problem in only the second paragraph:

However, in textbooks, there are no banks. In practice, though, such arbitrage typically entails borrowing and lending through banks, and the competitive assumption is violated due to balance sheet constraints that place limits on the size of the exposures that can be taken on by banks. Even for non-banks, their ability to exploit arbitrage opportunities rely on banks to provide leverage. Hence, if deviations from CIP persist, it is because banks do not or cannot exploit such opportunities.

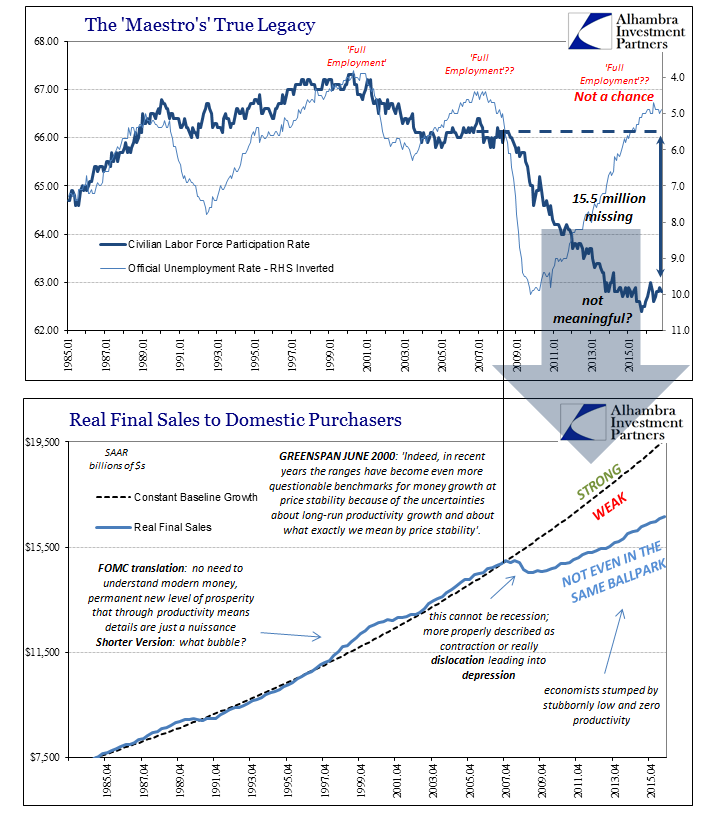

Economists for decades thought that money was money, end of story. In the real world, that just isn’t the case, and for longer than I have been in this business money had been transforming through banking into different conceptions that we (those who bother to look past the “settled science” of QE and Economics) still haven’t fully discovered or mapped out. Alan Greenspan’s June 2000 admission should finally sink him and all the rest who have followed in his ideological footsteps.

In short, bank balance sheets are at the very least an important part of the monetary system. When monetary authorities in the 1970’s argued in favor of floating currencies they didn’t truly know what they were doing, even though there were hints and glimpses already by that time in eurodollars that they simply ignored. I would, have, and will continue to argue that bank balances sheets are more money than the money that Economists use for their regressions (that never seem to work out in the real world).

As esoteric as all this might seem, there is a general simplicity to it that is easy to understand. If bank balance sheets are money, and banks are, overall, shrinking, then the supply of money would have to be shrinking, too. Such “tight” money conditions, as described in every textbook, says to expect falling prices, especially commodities, and at best sluggish economy consistent with lingering depression. Thus, the only real intuitive leap is to appreciate the role of bank balance sheets as central to the monetary process.

We are one small step closer to acceptance of the, to me, very obvious “dollar” shortage, though what that ultimately means isn’t clear. Just because the BIS finally got around to putting to official paper some of these concepts nine years too late doesn’t change the bitter arrangements of these past nine years, nor does it necessarily mean that the next nine will be meaningfully different. I suspect there will be enormous pushback from Economists, delaying even further what is in my view the inevitable conclusion. That is why it would have been far better to have started this debate in August 2007 (even August 2011, so as to not waste more time on LTRO’s and QE3) rather than toward the end of 2016.

Maybe it is better late than never, and that is likely true, but we still have to account for the colossal cost of “late.” And it is enormous, getting higher every day all this still has to be argued.

Stay In Touch