Thirty-nine delegates signed the United States Constitution in September 1787, but three refused to. George Mason, Edmund Randolph, and Elbridge Gerry were against the final draft of the document, Gerry included even though he had chaired the committee that had produced the Great Compromise. Campaigning in his native Massachusetts, the former Revolutionary who had previously served in the Continental Congress among the Boston delegation of John Adams, John Hancock, and Samuel Adams arguing stridently for Independence, Gerry denounced the un-amended governing principles as “full of vices.”

He was not alone in is opposition, as throughout the country there was a great debate more so about what was missing from it. Several of the states ratified it anyway, but on the explicit condition that it be amended with what became the Bill of Rights. James Madison, who drafted most of the text, wrote out 19, drawing from the Virginia Declaration of Rights largely written by George Mason. Madison proposed them to Congress on June 8, 1789; the House affirming 17, the Senate 12.

The final ten were ratified on December 15, 1791, two and a quarter centuries ago last week. One of the final 12 that was rejected by the states, the original unratified Second Amendment (Congress could not change their pay until an election took place), was actually added as the 27th in 1992 over two hundred years later. Though that proposed item is an obscure political, historical reference, we know very well what became the actual Second, as the First, but also perhaps the Fifth.

The Fifth Amendment decrees, “No person shall be…deprived of life, liberty, or property, without due process of law; nor shall private property be taken for public use, without just compensation.” Private property is central in this amendment because private property was understood then as a central check not just on government but as the primary tangible instrument of freedom. There was and is everything a man might think up and dream, but what he could do with such endeavors is as important in the plying of a just and stable social arrangement.

John Adams once wrote, “The moment the idea is admitted into society, that property is not as sacred as the law of God, and that there is not a force of law and public justice to protect it, anarchy and tyranny commence.” George Mason himself had declared, “Frequent interference with private property and contracts, retrospective laws destructive of all public faith, as well as confidence between man and man, and flagrant violations of the Constitution must disgust the best and wisest part of the community, occasion a general depravity of manners, bring the legislature into contempt, and finally produce anarchy and public convulsion.”

It wasn’t just the Founding Fathers who called private property the “bedrock of capitalism”, though of course they never used those terms invented later, as it had been very well understood especially as an outgrowth of the Enlightenment. Winston Churchill, the greatest of English statesmen, said in the 20th century that:

Personally I think that private property has a right to be defended. Our civilisation is built up on property, and can only be defended by private property.

As private property defines capitalism and freedom, it offends collectivism and socialism. Friedrich Engels wrote, “the slave frees himself when, of all the relations of private property, he abolishes only the relation of slavery and thereby becomes a proletarian; the proletarian can free himself only by abolishing private property in general.” Hippy folksinger and little “c” communist Pete Seeger suggested, “In a world of private property, if something isn’t owned by somebody, it’s going to be misused by somebody else.”

To all sides, banking has been a subject of so much consternation because it is a basic offense to all these perhaps intrinsic ideals. To the socialists and collectivists, banks are a primary source of inequality and oppression; to the original principles of the Bill of Rights, they can be too much wiggle room. For many today, banks should be abolished; to the founding generation they were to be severely constrained. One of the ways in which the latter could be accomplished was private property under the Constitution and Bill of Rights, and the inclusion of money into that realm.

The argument for modern banking, however, is that the needs of modern economy cannot be so restrained. The most extreme example, for those that take this line of argument, was the Great Depression. Banking had become a vital, central instrument of trade and general commerce, and therefore pure emotions of the people who had by their rights as property owners deprived banks of necessary funds with which to maintain trade and the nation’s economic welfare. Banks were increasingly removed from property law and placed more and more unto financial law that imposes this socialist view (the “greater” good).

I use the term “repo” exclusively not because it is shorthand but because it is altogether different from what the full term suggests. A repo is not a repurchase agreement; it is a collateralized loan. The way in which the latter became the former demonstrates a great deal about the overlaying of financialism in banking and modern money. For a very long time as repo became more popular, there was no actual agreement as to what a repurchase agreement actually was. It was not only unstandardized, it was treated very differently under the law.

When the US Court of Appeals for the Fifth Circuit ruled on American National Bank of Austin vs. United States of America in January 1970, they overturned the District Court’s ruling siding with the Bank of Austin against the IRS. The government had charged the bank with a tax assessment based on its own ruling that the Bank did not own the municipal bonds which it had claimed as generating untaxable interest. The District Court found that repurchase agreements as they related to collateralized loans did not transfer title of ownership; the Appeals Court found instead:

Since sale-versus-loan cases turn upon their own particular facts, United States v. Ivey, 5 Cir., 1969, 414 F.2d 199, the decided cases which have considered the precise question presented here offer little directional guidance toward a proper resolution of this case. We therefore take the route of ad hoc exploration through an expanse of essentially undisputed facts, see United States v. Winthrop, 5 Cir., 1969, 417 F.2d 905, to find that taxpayer was not entitled to the section 103(a)(1) income exclusion. [emphasis added]

In citing United States v. Ivey, the Appeals Court was reaching back to a similar case of ownership question vis a vis taxation (it’s always taxation, i.e., the legitimate boundaries of government) in the collateralized arrangement of physical commodities. James L. Ivey was a cotton farmer in the El Paso Valley of Texas who throughout the 1950’s engaged financial relationships with RT Hoover Company, a brokerage firm. Ivey appointed Hoover as his agent in the sale of his cotton for each planting season, and through that arrangement Hoover would warehouse the commodities until sales could be realized. Hoover would, at times, obtain loans collateralized by the warehouse cotton receipts and from time to time advance cash to Mr. Ivey from those loan proceeds for expenses related to the engagement of cotton farming.

Ivey had declared the advances from Hoover as income in the years in which they were still outstanding; the IRS determined that they were instead loans, collateralized by cotton, and that only the sale proceeds could be declared income. Ivey contended that it was his understanding that the transactions were ownership changes upon delivery, proceeds or not. Further, since he paid no interest on the advances it was his understanding that upon delivery the cotton was Hoover’s. The Court concluded that, “to treat what are in fact loans as sales would distort the taxpayer’s income.”

The facts of United States v. Ivey do seem to confirm the Fifth Appeals Court’s ruling in Bank of Austin v. US; that cases involving repurchase agreements had to be determined on their own merits rather than treated in standardized fashion. The reason for that seemed more obvious at the time, but has become, I think, lost as the connection of money to property and then to economy was systematically erased during this era.

I wrote earlier this year about a preceding case that had also recognized the obscured boundaries of repos and the clear establishment of title. In Union Planters National Bank of Memphis, TN v United States of America, there wasn’t even uniformity among the repo counterparties as to what was going on in these several trades; some were booked as repurchase agreements and all the legal niceties that should be derived from it, including a transfer of ownership; others were accounted as repos, collateralized loans where the understanding of each counterparty is on those terms. The District Court in the Union Planters case wrote in what surely seems obvious frustration, “one dealer advertised for sale to its customers those bonds which had been transferred to the Bank.” Thus, what does “sale”, “transferred”, even “bonds” mean under these arrangements?

My preface to all this in May was,

If the bedrock proposition of capitalism is private property and clear title to it, then repos have done little except make a mockery of it. First of all, the term “repurchase agreement” sounds abundantly clear and concise: one party sells something to another with an attached agreement to buy it back at some later date at some predetermined price. Legal title to the “something” should easily follow accordingly. But as with so many financial practices, the intrusion of “financial” changes everything.

Repos would become standardized such that they were entirely understood as repos rather than repurchases. While that eliminated the individual concerns of case-by-case review of the facts, it also moved this form of money to become exclusively “money.” With standardization came proliferation, of course, to which is always assigned a positive outcome for the “great good.” It is only in these “later” years where these distinctions have been revealed as sticky and difficult for a great many good reasons.

Repo fails, in particular, are an insult to the capitalist tradition. One of the primary imbalances that led to directly to panic in 2008 was the near total failure of the repo market, itself brought to that state by among several things the Lehman failure. In a world of fluid “fails” and rehypothecation, what did bankruptcy mean for these collateral chains where ownership was just this kind of fuzzy financial relationship? It was the ultimate form of unstable money, and the results of such monetary instability became very shortly thereafter obvious to everyone.

It wasn’t just that one instance, however, as the whole of the wholesale monetary system had been unstable all along; it just had remained unchallenged prior to August 2007. A repo as distinct from a repurchase agreement is not reducible to defined terms. It is a peculiar instance of a system that works because it works. “Everyone” tolerates a certain amount of repo fails because that is just the cost of the “greater good” of fungible wholesale money.

Another way of writing that is to suggest that repo system participants tolerate a certain amount of embedded and often visible instability. No monetary system will ever be perfectly stable, of course, because money is a social construct subject to the ever-changing human condition. That was one reason why it was once given the protection as property, so as to better align our own individual interests with understanding these variable parameters.

Monetary policy is supposed to reduce instability through its various methods of currency elasticity, which is itself another form of socialism in money; to use more if intended instability to counter instability. The results have been predictable in just that way; central bankers for the most part satisfied that they had alleviated monetary issues in the banking system at least, while at the very same time the banking system became more and more unstable to the point of a global monetary shortage. We can see this very plainly through the conditions of the repo market:

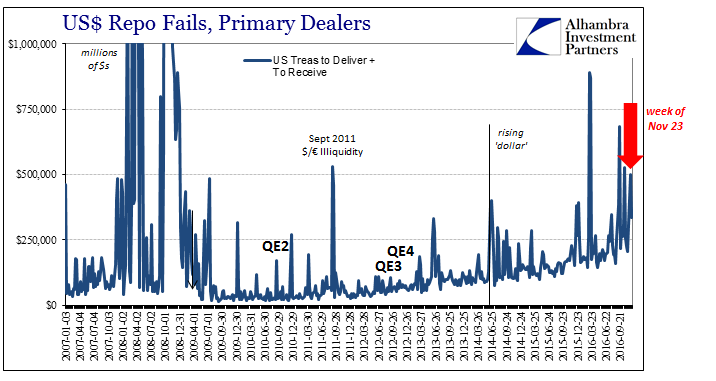

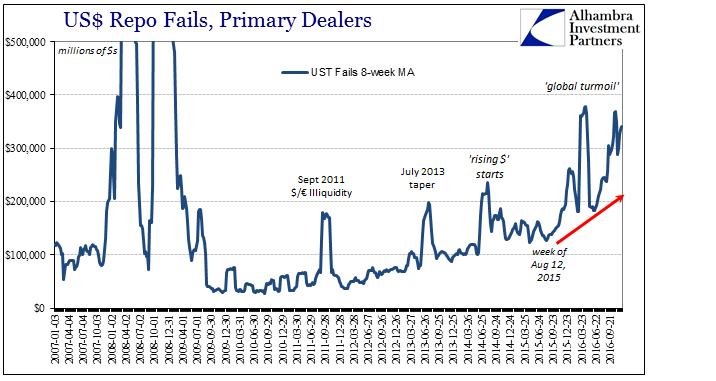

It is perfectly obvious that repo fails had been rising almost steadily since 2011, marked by short but intense bursts of illiquidity in the middle of 2013 and again in the middle of 2014. That all changed the week of August 12, 2015, a week we should all know very well by what happened with the Chinese yuan; not because it happened with CNY and the global importance of China, rather due to how the Chinese relate their system to the “dollar” system. Since repo fails are a highly observable form of unstable money becoming more unstable, the financial and economic results of the past year and a half are wholly unsurprising.

Since the last week in August 2016, repo fails have not been less than $200 billion (both “to receive” and “to deliver”) in any week. Of those fifteen weeks (thru the week of December 7), they have been greater than $300 billion eight times, including each of the past four weeks going back to the week after the election (which does not propose the election as the cause). Fails have been above the $500 billion level three times, and each of those weeks corresponding with a whole lot of Chinese money market instability (which does propose more than the contours of causation within a global monetary system).

In the 31 weeks of 2015 prior to that week in August, repo fails were more than $200 billion only three times; the highest level of fails was a spike to $285 billion the first week last March just before the Chinese starting pegging CNY for as long as they could. You could say that the repo market has become “used to” a higher degree of instability for operation over the past two years, but it is much harder to make the same claim for money markets and general economic function globally. To economists, the two are unrelated; understanding both eurodollar operations as well as how they got that way reveals that not only are the two related, one does follow closely the other.

Repo fails are only one possible form of monetary instability, but they are emblematic both of the immediate problem as well as the disease of the whole system. This is not capitalism, full stop. You can add whatever other term you like in its place, I use financialism not just because of the preference it gives to financial considerations above all else, especially economy, but also because the word embodies the balance of transformation from property law to finance law and all that has gone with it. The largest such drawback has to be not just the depression since 2007, but more so the derived inability of those who are supposed to know better, who claim they know better, but clearly don’t know any better about what has actually happened all this time.

In short, we’ve wasted just about ten years calling a depression a recovery, and all because money is so unstable that it has become, for the mainstream as well as mainstream authorities, unrecognizable. If you don’t know what money is, you aren’t going to know when money is a problem. When money was property, we all had to know better because it was our own that was at stake. In the “modern” version, it is left centralized to the cabal of ignorance and ego, a concern that motivated exactly the writing, ratification, and righteous enshrinement of the Bill of Rights.

Stay In Touch