The only unequivocally positive aspect to the looming “stimulus” debate is the immense political theater it will generate, and has already generated. Hypocrisy will be standard fare, and in any number of ways. For every Occupy Wall Street Obama supporter who found himself likely for the first time in his life enthusiastically embracing “record high stocks” in 2013 will now be replaced by an ARRA-hating Republican who today screams Dow 20k in anticipation of Trump’s version of it.

The mindlessness of the political labeling will be very confusing for a mainstream that will largely stay out of it, apart from noting the grand inconsistencies that will be offered up as “analysis.” Paul Krugman, for one, a man who once was awarded a Nobel Prize in Economics, and who for eight years claimed at every opportunity “austerity” was evil and no deficit was too small to do something about it has now switched to worrying if a President Trump will “waste” too much in his spending and that such waste will absolutely visit catastrophic long term consequences upon the fiscal health of the nation. On the other side from Krugman, and in this case meaning the same side politically, is the newly minted Junior United States Senator from California who appears enthusiastic to embrace “stimulus” from a decidedly non-economic rationale:

Here's the truth: infrastructure spending isn't a transportation issue for most Americans — it's a human rights issue.

— Kamala Harris (@KamalaHarris) January 25, 2017

Economists have done us no favors by insisting that fiscal spending of any kind and in any place has positive often large multipliers. It is nothing more than assumption passed off as, again, “analysis.” Unfortunately, in the United States the last bit of empirical evidence is about eight years old and worked far more against the idea than for it. The Stimulus Bill, as it came to be known, was in the end a term applied in derision rather than an embrace in honest cataloging. Officially it was the American Recovery and Reinvestment Act, which, as I always say, you can tell what won’t happen by what is put in the name of any Congressional act that becomes law; there surely was no recovery and serious questions remain as to what actually constituted re-investment.

This time, however, we are supposed to forget all that and, I suppose, simply accept that the economists who criticized the last “stimulus” will now get the current “stimulus” correct. I, personally, would prefer it if government officials of either political party or of any political persuasion would simply stop trying to create a recovery; maybe it just isn’t your job. In writing that, however, I fully recognize “stimulus” for what it more often actually is, the expansion of political power couched as vitally needed economic aid. From that perspective and to those ends, there can be no such thing as “waste.”

As a matter more purely of economic analysis, we have recent examples and evidence as to the performance of fiscal “stimulus” in particular. Given the disastrous state of the global economy, I have to believe that the Chinese would prefer not to be the prime example for almost every kind of economic experiment in ailment out there. They are not innocent in all this, of course, as they paved their economic foundation on the surface of shaky “dollars”, so they are now reaping nothing more than the fruits of a dubious multi-decade intentional endeavor and dealing with the consequences of it in increasingly ad hoc and erratic fashion.

That includes a massive fiscal program that was initiated just last year. Chinese officials demonstrated very well the prime difference between 2015 and 2016; in 2015, they were content to believe Janet Yellen was right about the US and therefore global economy, and thus let things sort of happen on their own; before even the start of 2016, they realized they couldn’t afford to continue to make the mistake of believing that Yellen or any other economists knew something useful about any part of any economy.

To estimate the size of the fiscal response, we have to make a few calculations and assumptions. You can quibble with my definitions and how I have worked out the numbers, but my intent here is not to account down to the yuan exactly how much Chinese authorities spent, and therefore create a high R-squared regression from it that will determine to four decimal places the exact statistical multiplier of the program(s). We simply don’t need that level of precision, or precision at all, as rough estimates are more than enough to make reasonable determinations.

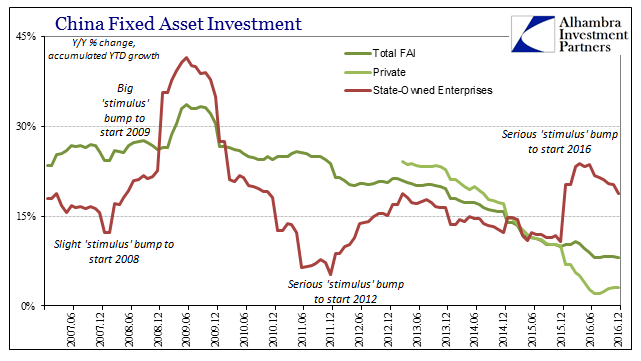

The primary form of fiscal “stimulus” is shown above; state-owned enterprises that engage in far more Fixed Asset Investment (FAI) than they had done previously. These big jumps in FAI through state channels are clearly “stimulus” by any definition, as they are certainly not individual firms deciding all at once about tremendous profit opportunities in the construction of a lot of things China has found the country didn’t actually need (pace Keynes).

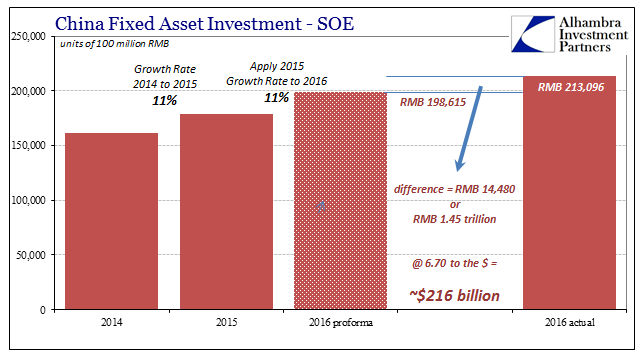

Full year 2015 FAI in State-Owned Enterprises (FAI) grew by 11% over full year 2014. If we assume the same growth rate as a baseline for 2016 comparisons, that would have meant RMB 19.862 trillion as a starting point for last year. Instead, FAI via SOE’s was RMB 21.31 trillion, meaning that additional spending was in the neighborhood of RMB 1.45 trillion. At an average exchange rate of 6.70 to the dollar, it was about $216 billion in “stimulus”, which is not a trivial sum by any stretch given that it was about 1.9% of 2016 total accumulated GDP.

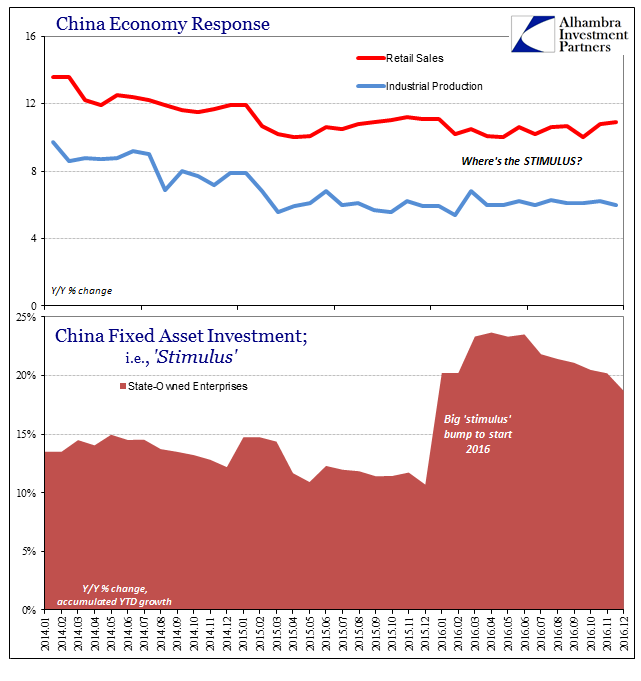

The results of having spent that huge additional amount, however, were whatever description might lie beneath underwhelming:

The most charitable attribution would be to claim that at least it didn’t get worse in China, which leads last year’s Chinese “stimulus” straight into the class already populated by the ARRA and its version of “jobs saved.” There just isn’t any indication at all it had any effect whatsoever. You may argue lags in that the Chinese economy didn’t have enough time to absorb and reflect upon this massive infusion, and that may be correct.

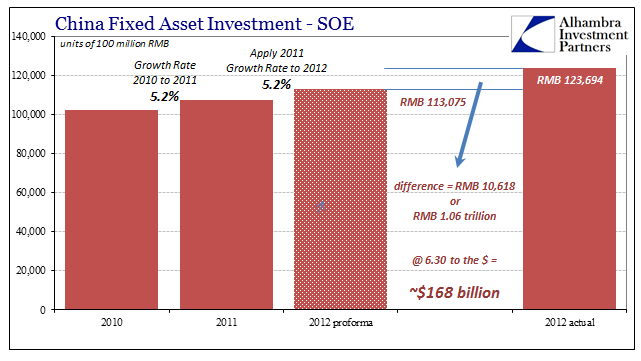

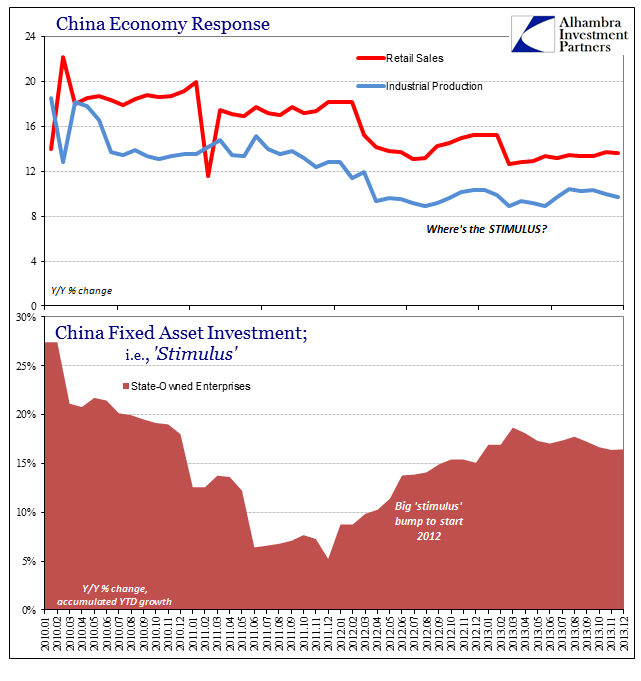

Fortunately, this is not the first time the Chinese have done this. In 2012, as 2016, Chinese government authorities similarly enacted fiscal spending plans far above the prior year’s level so as to treat with similarly great economic concerns. The scale of those plans were also in the same ballpark (and near exactly the same as to scale, which I don’t think coincidence) when adjusting for the different size of the Chinese economy then vs. now.

The relative increase in FAI 2012 versus what it might have been at a constant 2011 growth rate was RMB 1.06 trillion, or about $168 billion. That is, again, of the same size scale (2.0% of 2012 GDP) and produced exactly the same disappointing and inadequate results:

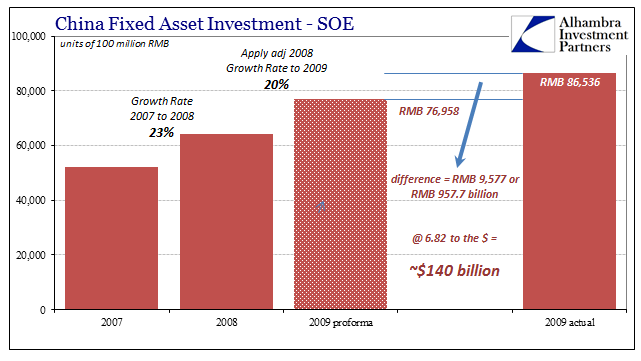

The only period where one might suggest “stimulus” worked was in the immediate aftermath of the Great “Recession.” In making 2009 calculations of FAI spending, I made a small adjustment in the 2009 proforma to account for the fact that Chinese authorities had already begun the “stimulus” toward the end of 2008. Whereas the accumulated growth rate was 23% by the end of 2008, I applied only 20% to determine the baseline for 2009.

With that adjustment, I figure the direct fiscal injection in FAI was about $140 billion, which was actually significantly larger (2.7% of 2009 GDP) than 2012 or 2016 (as you would expect given the circumstances of 2009).

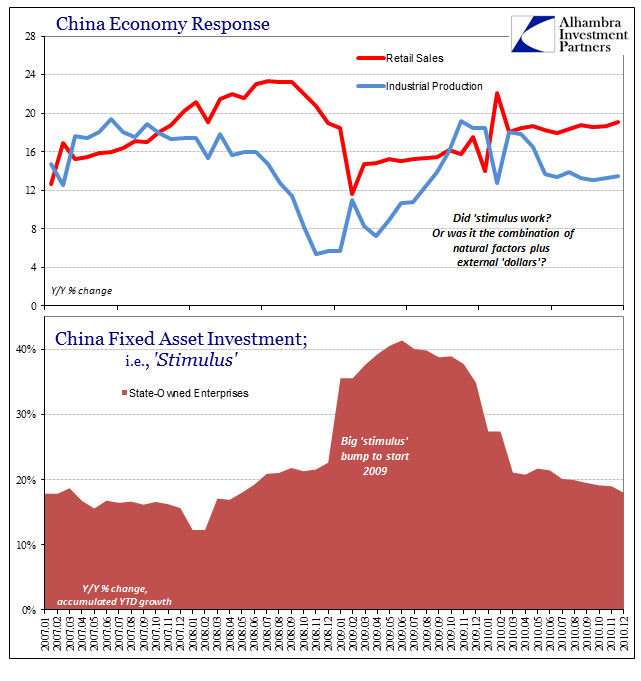

Industrial production rebounded nicely, and retail sales accelerated to a lesser extent. But was that due to “stimulus”, fiscal as well as monetary, or just the natural end of the global Great “Recession?” If we attribute China’s (partial) recovery in 2009 and 2010 to it, then how do we account for the vastly different results in 2012 and 2016? I think the answers are incredibly easy and simple, as the big difference between 2009 and 2012/2016 is found in an external but highly relevant capacity, as noted yesterday.

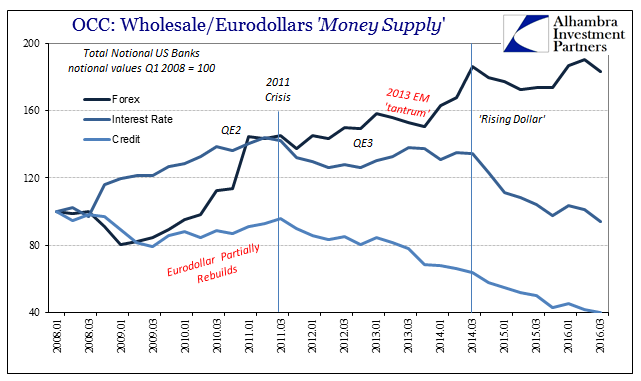

It’s the same difference we find in “stimulus” of all kinds all over the world, where what seemed to have maybe worked in 2009 by 2012 had become totally ineffective. This clearly different spectrum of results proposes that in no uncertain terms it wasn’t “stimulus” driving economic conditions at any of these times. If it all appeared to be a positive factor in 2009, that was far more likely due to the partial restoration of the eurodollar system (pictured above); thus, the difference between 2009 and 2012 or 2016 is the end of that restoration.

There just isn’t much, if any, evidence that fiscal spending is actually stimulus. But, as I suggested toward the beginning, that may not really be the primary consideration here. At least it will be highly entertaining political drama, because it is (still) decidedly bad economics (small “e”).

Stay In Touch