What do consumers know that Economists don’t? It’s a loaded question, of course, particularly in this day and age where Economists spend years perfecting the study of mathematics. In many ways, formal training is an impediment to analysis of the economy. There’s nothing wrong with learning about regressions, but it can and often does appear to take away from intuitive capacities for the real world. The math becomes “more real” than actual experience.

It is a form of corruption, where confidence in the modeled projections becomes unshakable as more evidence piles up against it. The recovery and boom (therefore inflation) may not be here today, but the more today’s that pile up without that happening the more it must tomorrow. Models are never wrong, for Economists, they are always early – seven years early (and counting).

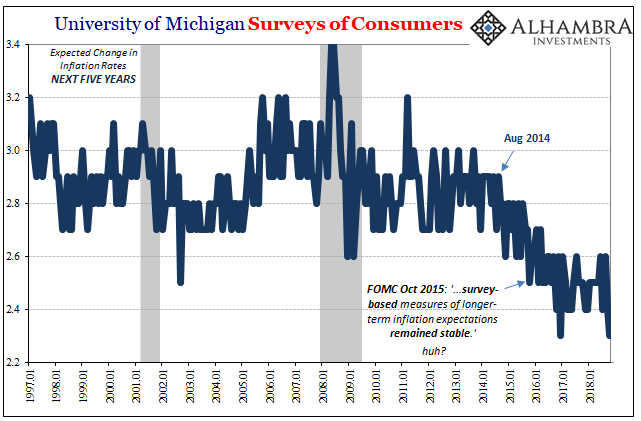

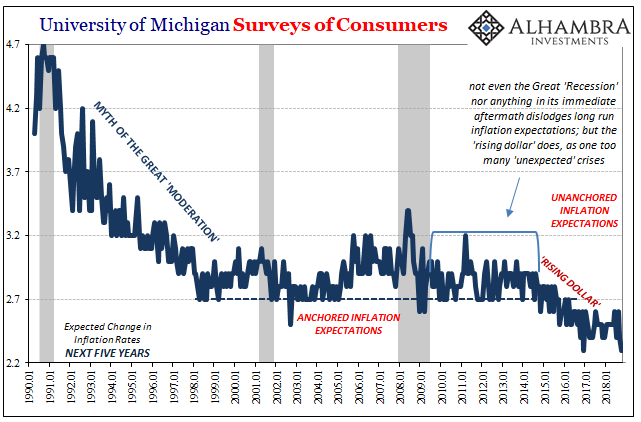

The University of Michigan reported last week that long-term inflation expectations among consumers matched their lowest level on record this month. The expected average annual change in consumer prices over the next five years was for consumers just 2.3%. The only other time in almost three decades of surveys the long-term inflation outlook was this small was December 2016.

For Economists, this can’t possibly be; or, as many of them have expressed since the middle of 2014, consumers are just irrational and/or illiterate. About statistical mathematics, that is very likely so; about the economy, it is almost surely the other way around. Since they’ve never studied the often great difficulties when confronted by heteroskedasticity Economists believe consumers can’t possibly know what they are talking about with regard to the general effects of oil and commodities.

Where DSGE models fail to include financial markets, or even just monetary conditions, consumers don’t have the luxury of remaining blind year after year of little or no legitimate economic growth. They know a recovery when they see one, and this ain’t it. It may be called a strong economy, but consumers continue to point toward something else entirely.

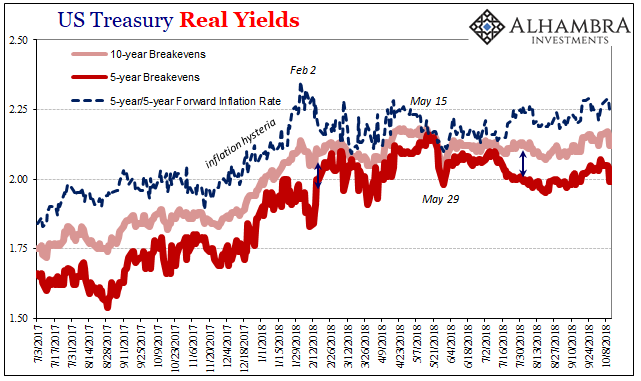

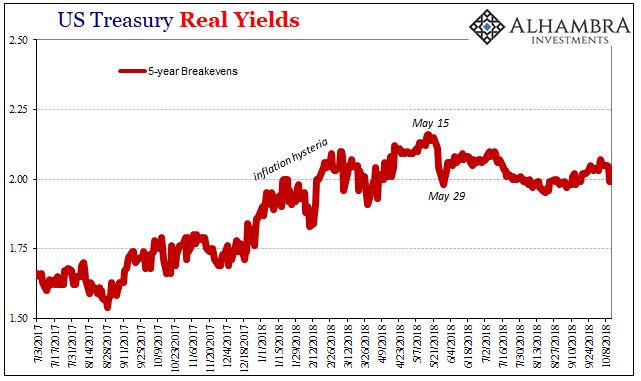

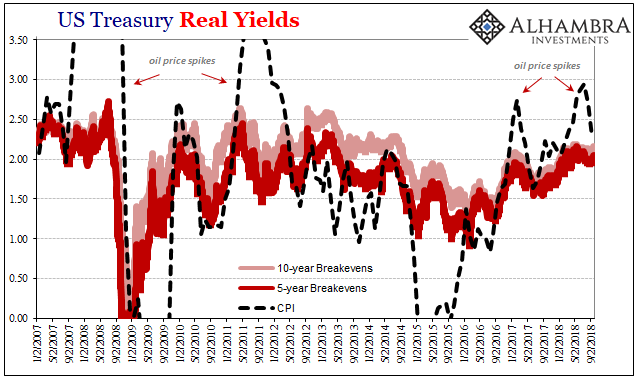

Their view is backed up by markets, in this case the Treasury market. TIPS yields are consistently stuck at the lower ends of expectations. Since May 29, whatever small upward (inflation positive) optimism which had broken out of the 2017 upturn has passed.

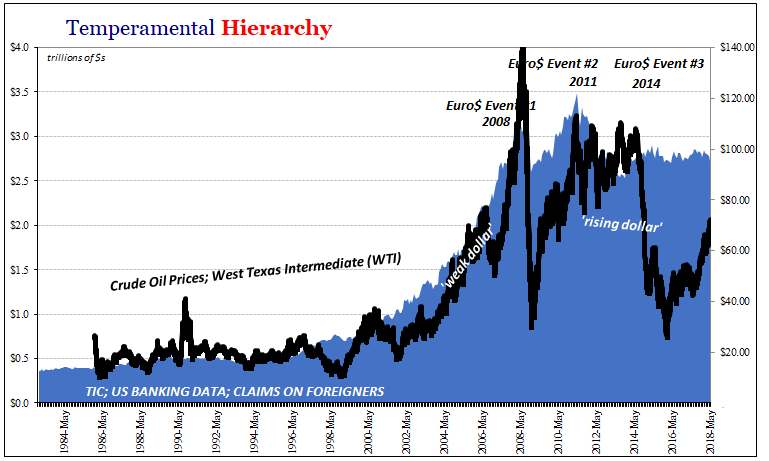

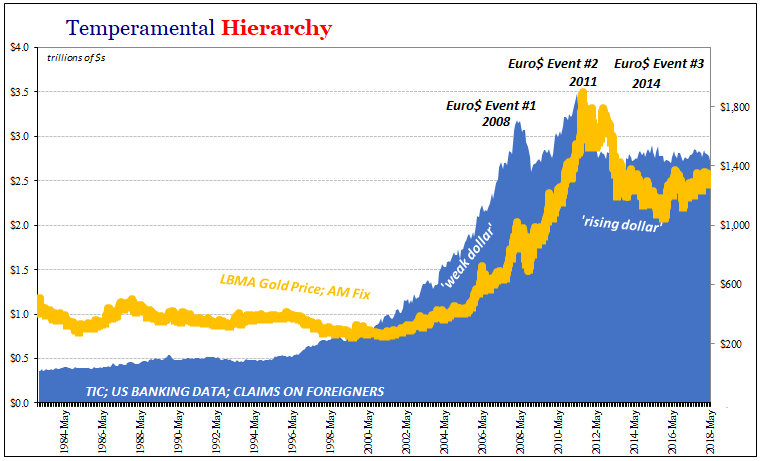

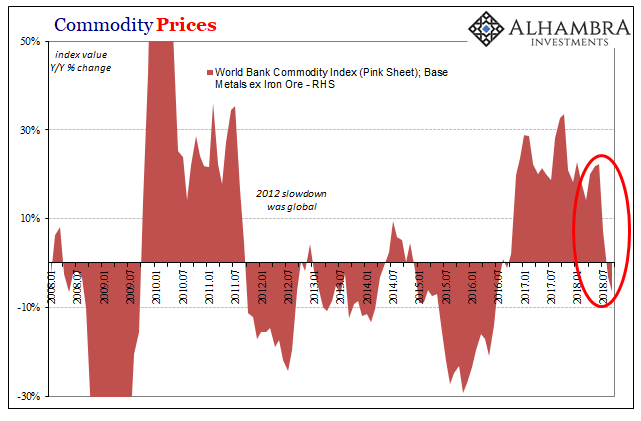

Like consumer expectations, market inflation expectations are weighted heavily toward the downside again. Most of what inflation has materialized over the past few years has been commodity prices alone, a lot just crude oil, and now there is the growing realization in the real world outside Economics the mild upward trend has stalled if not rolled over entirely.

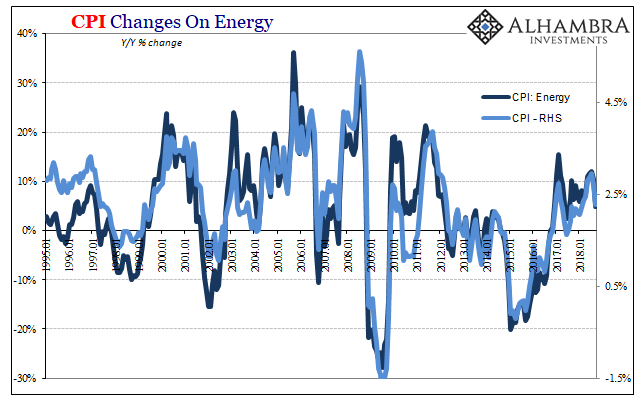

The data-dependent Fed will march forward anyway no matter the lack of data. This dearth of statistical confirmation also included last week’s CPI estimates. The headline advance for consumer prices was materially less than expected by analysts, as the oil price ascent proved once again the only basis for inflation rates above those posted during the past seven years.

According to the CPI, the rate of advance was 2.28% in September 2018 down from 2.70% in August and a high of 2.95% in July. The energy index which had been rising at double digit rates each of the prior four months before September increased by “only” 4.8% last month. Without oil, meaning continued strength in oil, there is no inflation.

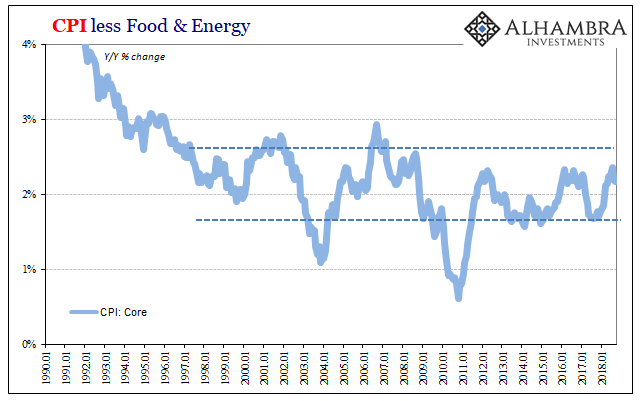

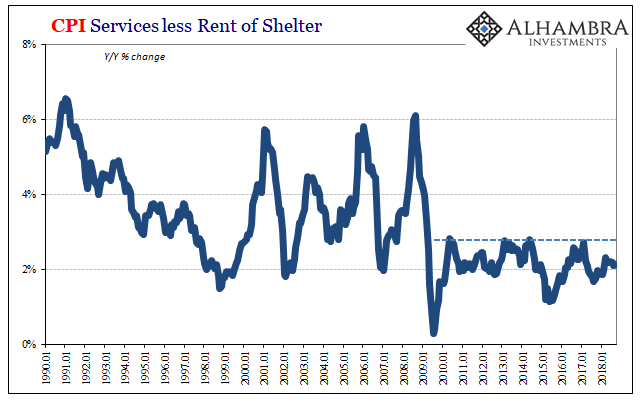

Despite the mini-revival of hysteria following the August payroll report released in early September, there is just no indication whatsoever that inflation regimes have shifted toward a more robust economy. Quite the contrary, September was yet another month clearly displaying the same depressive characteristics (especially in the all-important service sector).

In other words, if there is wage inflation, which we know from labor statistics that there isn’t, consumers are not using those gains to demand more and pressure companies (especially in the service sector) to raise their prices. This is, in theory, what Economists are expecting.

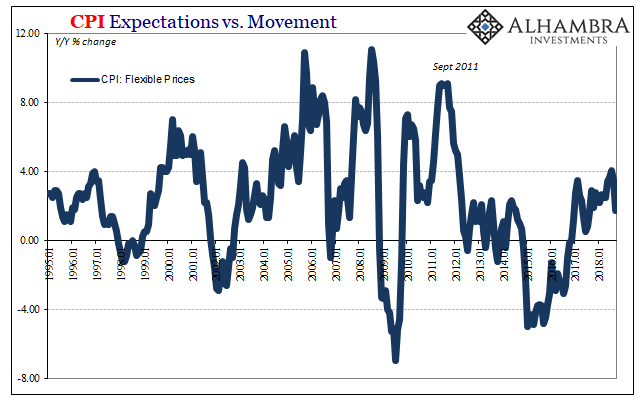

It is perhaps ironic that in the places where consumer prices have been moving the most over the past two years it actually shows us the absence of inflation pressures the best (above). Flexible prices under the CPI definition even at their highest this summer were nowhere near as significant as they had been in years past.

In other words, if core rates are where an inflationary trend would show up last and most convincingly, flexible prices would be where it would start. Therefore, even the beginning of this last hysteria was predicated on vastly overstating price changes where the trend might have launched (small surprise, what with the hysteria surrounding it).

What’s changed instead is that over the past few months risks have all shifted back toward the downside; or, risks have always been this way perceptions of them have changed. Commodity prices outside of oil are now potentially reflecting not just rising economic risks but already economies in trouble (or, more appropriately, parts of the global economy retrenching as a first step toward the next downturn applicable for the whole of it). Consumers, and to some extent TIPS markets, are wise to the risks that Economists like Jay Powell refuse to account.

In the ideology of Economics, statistical models are better data than actual data.

The CPI was their best shot to trick for expectations. Even then, it never really got far. If Jay Powell isn’t careful, he’s going to unintentionally stamp his name, and his alone, right on this “boom.”

Stay In Touch