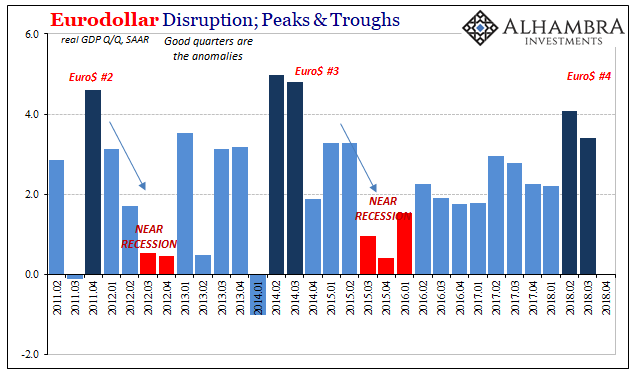

We will hear all day and for the next month (at least) about the two best quarters of GDP growth in four years. Somehow this will be used to justify calling this an economic boom, even though those two quarters in 2014 supposedly didn’t qualify. And they were better quarters, at least so far as real GDP goes.

Knee-jerk reactions are always tricky, but it’s safe to write that the bond market is thoroughly unimpressed. Treasury yields are falling despite the headline 3.5%. Struggling to understand, yet again, why anyone would bet against a resurgent US economy, commentators are first forced to acknowledge the potential for a “slowdown” already visible in many places around the world in order to postulate how this current gangbusters boom could possibly be susceptible to the “overseas turmoil.”

That’s not really the main concern. Instead, the biggest worries are right there in the current GDP report.

It gets back to the idea of globally synchronized growth. In 2017, the narrative was offered and without defining it in specific economic accounts the intuition was simple. Globally synchronized growth was supposed to convey how everything had finally changed; that, yes, the economy had posted an occasional good quarter here and there, maybe even two, in the past but starting in 2017 it was going to have good quarter after good quarter after good quarter.

This time it was different, they said.

Bonds around the world are being bid, on both already visible as well rising liquidity risk, because it’s increasingly evident it really isn’t. It’s the biggest disappointment, by far, of 2018. This is a boom except for all the trouble you don’t normally find during one. There isn’t any hint we’ve put all that sputtering behind us. Rather, combine the realization that things haven’t changed with the prospects for rising monetary and liquidity concerns and there you go.

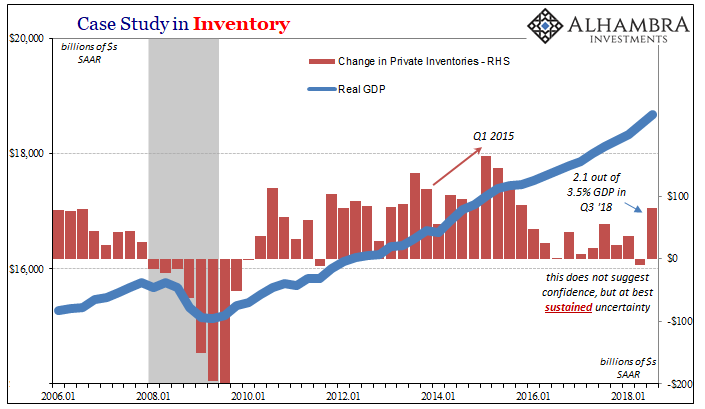

In the third quarter of 2018, headline GDP rose by 3.5% quarter-over-quarter in constant 2012 dollars. Almost 2.1 points of that growth rate was inventory alone. While consumer spending contributed 2.69 points to the headline, slightly more than in Q2, this is still a historically slow pace of activity. It was the best consecutive quarters for consumers since, obviously, the middle of 2014 four years ago.

This is still the same moribund trend that began in August 2007. What the latest GDP estimates show is that these reflationary periods really do have an unusually low ceiling, which makes these constant ups and downs all the more destructive. The economy slows and then never really gets going again, even when experiencing “good quarters.” There’s nothing but danger in recognizing this might be as good as it will ever get.

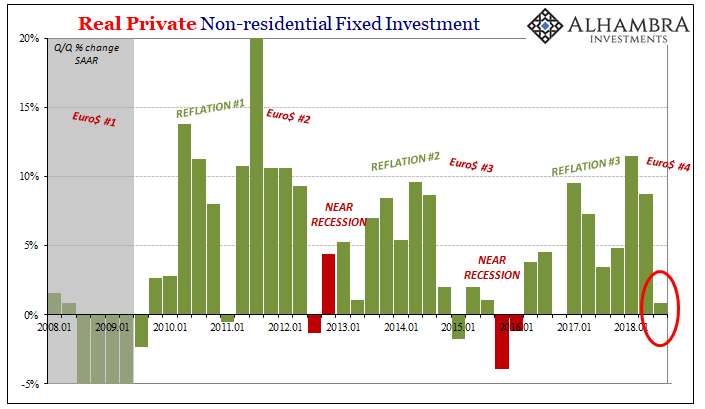

Q3 is instructive in that regard even beyond inventory. Business capex, called non-residential fixed investment in GDP parlance, was unusually weak last quarter. It subtracted a few bps off growth but that compares to better than 1-point contributions in each of the prior three quarters. Quarter-over-quarter, business investment was practically unchanged.

Perhaps that’s just a temporary pause after a few quarters of somewhat decent activity. Then again, everyone thought the same thing in Q4 2014 when business investment “unexpectedly” tailed off, too. At least three years and three quarters ago you could blame the oil patch for the sudden and sharp drop. In 2018, it’s other more general businesses that are declining to invest in the boom.

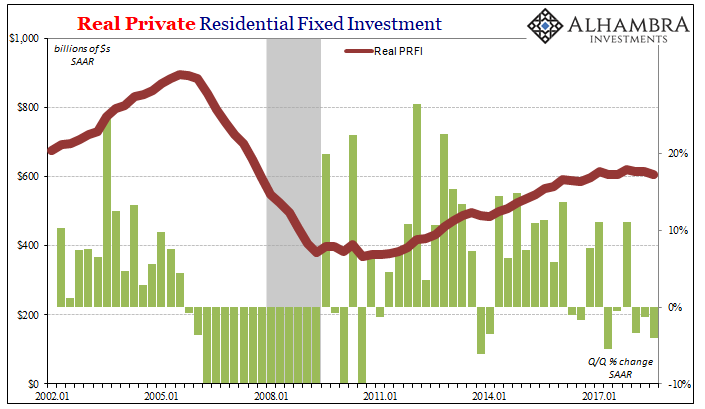

The other piece of fixed economic investment is housing. The GDP estimates merely confirm everything we see outside of them. The real estate market and construction in particular have fallen into a slump. This does not mean that it is heading for a crash like the previous housing bust.

But it isn’t at all consistent with an economy speeding forward onto a new and improved economic baseline. Residential fixed investment has declined in every quarter this year.

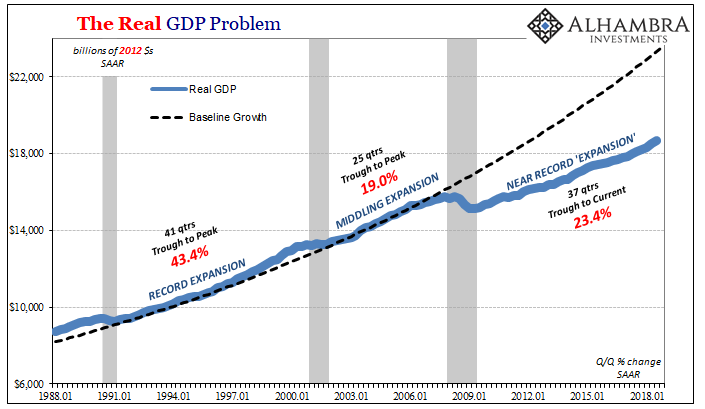

Because it doesn’t add up to an actual economic boom, the mainstream has instead focused on time for all the wrong reasons. It has been 37 quarters since the last declared recession. This makes the current “expansion” the second longest on record. If it can continue for one more year, it will equal the nineties and the complete decade following the mild recession in 1990-91.

It would only be alike in that one arbitrary dimension, however. In what actually matters there is absolutely no comparing the two. It’s what makes this idea disingenuous perhaps intentionally so. By making the comparison about time, proponents are attempting a bait and switch; this economy must be like the nineties because it’s approaching the same length. Therefore, boom!

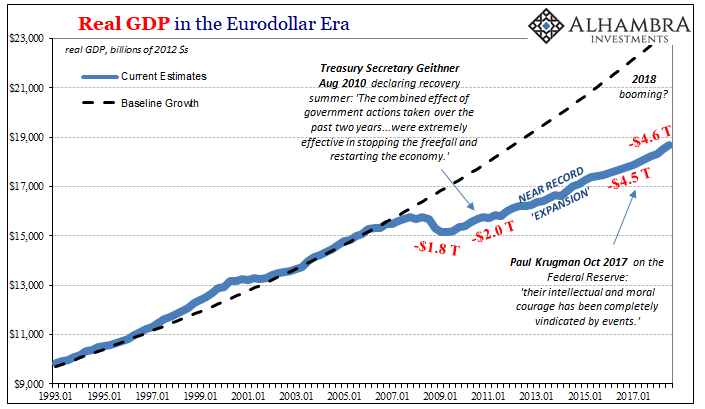

Even if we don’t include the size and length of the contraction, the recovery or expansion period is unlike anything we’ve experienced since the thirties. That’s the useful and appropriate analog, not the nineties. Though the current economy is nearing the same time interval, it is doing so at only a little better than half the rate (again, this does not include the recession portions of either).

In fact, the current “recovery” is barely more than the one in the middle 2000’s even though it has already lasted three years longer.

What that means for the current quarter is that time isn’t on anyone’s side. Economists and policymakers like Jay Powell may think the length of expansion proves it is an expansion when in fact it actually proves the opposite. If the economy has been stuck without growth for this long, what are the honest chances that it will suddenly break out of the malaise? The longer it goes, the less the probability becomes.

It is what it is.

And then you get a GDP report like the one for Q3 that may look good, but is filled instead with red flags. This is entirely too familiar.

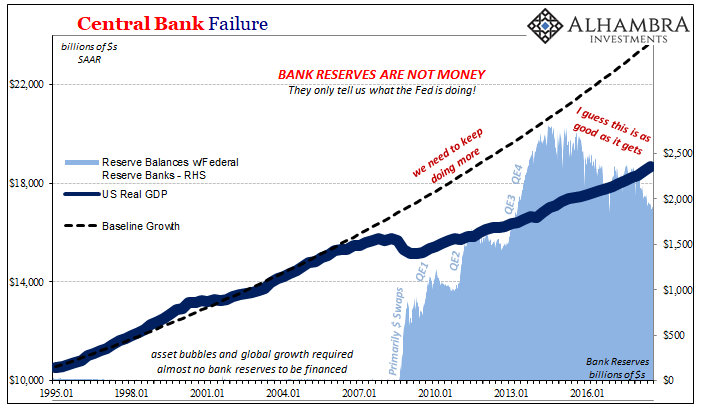

This realization applies as much to the Federal Reserve as the economy. There is less talk of so-called quantitative tightening than there is about loose trade war stuff, but either one are looking for excuses in the wrong direction. The economy is clearly in the same way as it has been for more than a decade; there is nothing new here.

The Fed’s role in all this is irrelevance. The level of bank reserves only tells us what the central bank is doing, and by extension what it thinks of the current shape of the economy. Up until 2013, US central bankers knew they needed to do more because of obvious reasons.

Since, policymakers have drawn the conclusion there is nothing more that can be done. That’s the only thing the level bank reserves tell us, nothing else. To justify this view they’ve made a lot out of what little is available to them; from completely (corrupt) writing down economic potential (radically redefining the very idea of recovery) to calling the economy in 2018 strong when it doesn’t even measure up to four years ago (let alone eleven years ago or the nineties).

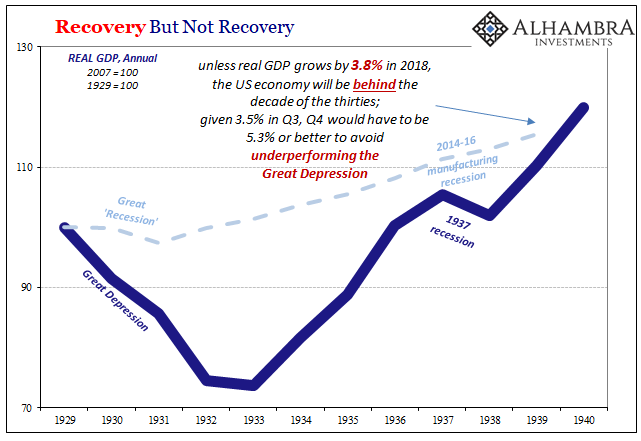

Since Q3 2018 came in at just 3.5%, that means unless GDP expands by 5.3% in Q4 the Great “Recession” economy will have “expanded” by less than the Great Depression economy.

This is the only realistic comparison, not to the nineties, and it demonstrates the severity of the situation quite well. The more time passes for this “expansion” the more obvious that it won’t change out of it. The latest quarterly numbers remind us once again the dangers of being stuck right here.

If this is as good as it gets, buckle up.

Stay In Touch