When Argentina requested, and received, a ~$50 billion bailout from the IMF in mid-2018 it was a total shock (to those who follow only central bankers and Economists when it comes to anything, though especially relating to the global dollar system). The platitudes were issued alongside standby financing which lasted only a couple of months before the stricken country pleaded for both more funds as well as an accelerated timeframe for when to receive all of them.

It ended up being a total disaster, and still is today (comprehensive currency controls and yet the peso continues to drift lower and lower and lower).

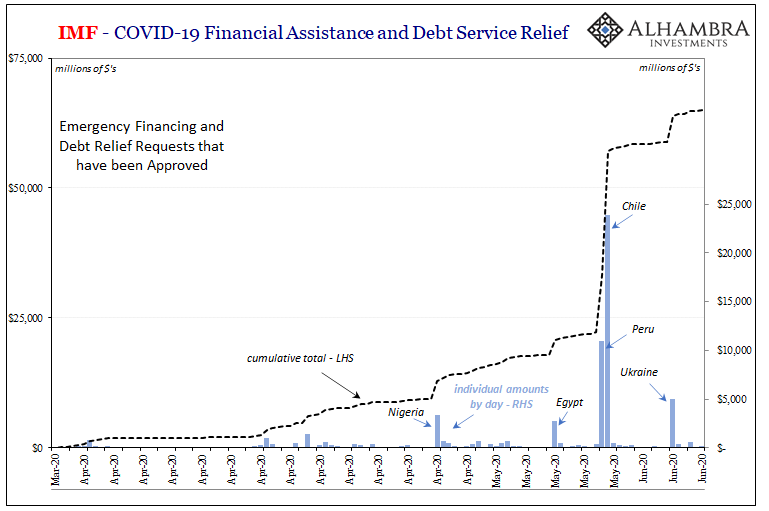

But if $50 billion was a shock, in today’s world $24 billion counts as an improvement?

Not Argentina again but this time its neighbor Chile. Back on May 12, the IMF had received an emergency funding request from that particular country. Authorities in it wanted an immediate discussion for a two-year credit line about equal to 1,000% of the Chilean IMF quota. Approved seventeen days later, it works out to about $23.93 billion.

Didn’t make the news.

Perhaps that was because unlike Argentina, Chile seems to be held in much higher regard. Whereas the former requesting a large bailout feels par for the course, the latter hardly ever generates so much fuss and bother. As the IMF has been very clear in pointing out:

Chile qualifies for the FCL by virtue of its very strong fundamentals, institutional policy frameworks, track record of economic performance and policy implementation and commitment to maintain such policies in the future.

Managing Director Kristalina Georgieva later added:

Chile’s very strong fundamentals, institutional policy frameworks, and track record of implementing prudent macroeconomic policies have been instrumental in absorbing the impact of a series of recent shocks.

Yes, yes; we get it. Very strong fundamentals. But doesn’t that make this more alarming, not less? What I mean is, when the basket case that is Argentina gets approved for a huge handout, that’s one thing that already makes sense. When Chile asks, and receives, half of the amount, with its strong fundamentals, that only begins to raise key questions.

When good countries are even half as bad as what had been, by far, a record sum paid out for one of the worst countries…

To be sure, they’ve hardly been alone. Peru had also requested a large credit line from the IMF and scored an $11 billion approval the day before Chile. Just two weeks ago, the Ukraine managed to snag a two-year $5 billion line which disbursed $2.1 billion immediately; for balance of payments issues, yes, but also fiscal “budget support.”

Now, these are the largest of the commitments so far which the IMF reports sum up to just under $65 billion in total. With $100 billion already made available, and total funding power supposedly $1 trillion (with requests being worked out to perhaps double that amount), we are led to believe everything’s under control.

For as much as the COVID-19 shutdowns have disrupted the global economy, three months into it and maybe it doesn’t seem all that bad. The organization had received more than 100 requests for emergency funds, and, in fact, the IMF has disbursed more than 100 approved allotments.

So far, they’ve largely been limited to very small payouts. Again, is it reassuring so many smaller nations are only asking for dribs and drabs; or, is this maybe ominous in that it might be so bad out there smaller nations are being forced to beg for essentially pocket change from supranational authorities because their margins are so thin and they can’t get it anywhere else?

Then there’s the (more important) matter of trajectory. Does it seem to be getting better, leveling off at a manageable level? Or perhaps merely the first wave with more, and bigger, requests still to come?

Since no one outside of the affected parties is privy to the inner workings of these requests, we can’t say for sure one way or the other.

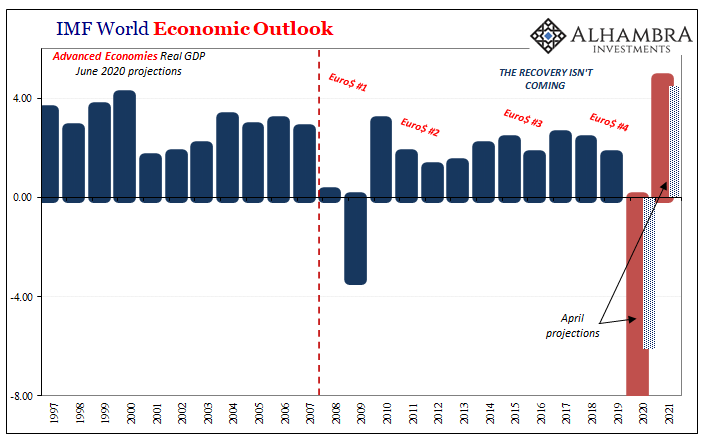

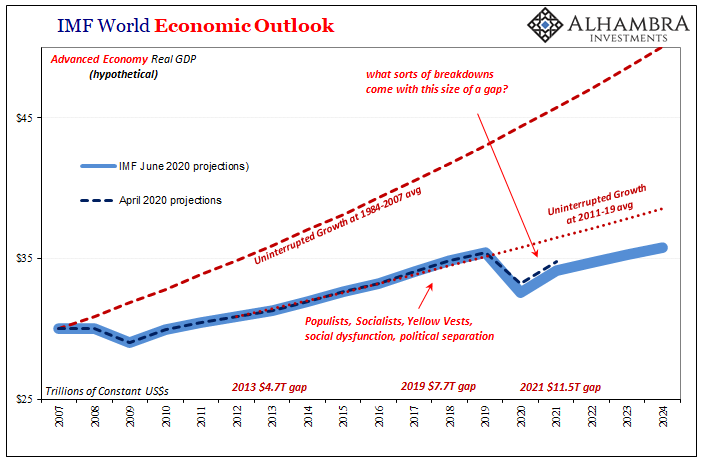

However, it is interesting that in its latest World Economic Outlook (WEO) published today the staff Economists at the IMF, using their typical DSGE econometrics, substantially downgraded expected growth both this year and next year for Emerging Economies.

Back in early April, taking their first swipe at projecting the downturn and the rebound out from it (not a recovery), these models forecast only a 1% decline for real GDP in calendar year 2020 followed by +6.6% in 2021. Now, it’s -3% and then just +5.9%. It may not sound like much but both are significant downward revisions.

Why?

The IMF may be uniquely situated to better understand (even if not fully) the potential real economy drag from what’s looking to be a drawn out and at best uncertain global dollar shortage. Strong Fundamentals Chile and $23.93 billion certainly doesn’t argue for thinking meaningfully better about this year or next (or what follows 2021).

Away from Emerging Markets, DM economies are in just plain trouble. Dollar shortage and spillovers, assuming everything goes right from here with them (including local “stimulus” in addition to the IMF not Argentina-ing more than a couple of its more than hundred borrowers) the models are, like all the rest, extremely light on the right side of this purported “V.”

Back in April, they calculated the 2020 downside at around -6.1% this year and then +4.5% next year. While they’ve bumped up the rebound a touch (almost certainly due to their improperly optimistic views of “stimulus”) to +4.8%, that would already get canceled out by what’s now looking like -8% in contraction.

All of which leaves the US, Europe, and Japan in horrible shape by the end of next year, only hoping it starts to get better into the middle twenties. Thus, nowhere near a “V” since the advanced economies aren’t really advancing anymore – not that they had been during the decade prior.

In fact, what we’re really talking about here is more and more a near-certain, multi-decade double “L.”

Somehow the idea took root that governments can flip the economic switch at will; turn everything off and then turn it right back on again. No harm, no foul.

Three months later, we still don’t have any good idea how much harm there ultimately will end up being, but we already know that it won’t be zero. Furthermore, there is every reason to suspect these numbers are the most optimistic scenarios, and they aren’t anywhere close to good.

While none of the models factor a second COVID outbreak, they also ignore what I believe is a much higher probability second leg for GFC2. The first time we did this, GFC1, there were two legs, too (though you could make the argument the second leg should be split around December 2008, leaving a total of three; whatever the case, certainly not one).

Chile, strongly fundamental and otherwise solidly awesome, yet now needs half an Argentina. The final dramatic touch of a successful few months for authorities, or particularly portentous sign about what really comes next?

Stay In Touch