To hear the media talk, you’d think that the most pressing issue in the world right now is the dangerous prospect for rising interest rates. Rising. Its members are given this idea from the one source they rely upon no matter how many times that same source lets them down and leaves them in the lurch looking so very foolish (see: BOND ROUT!!!!)

That source is, of course, central bankers.

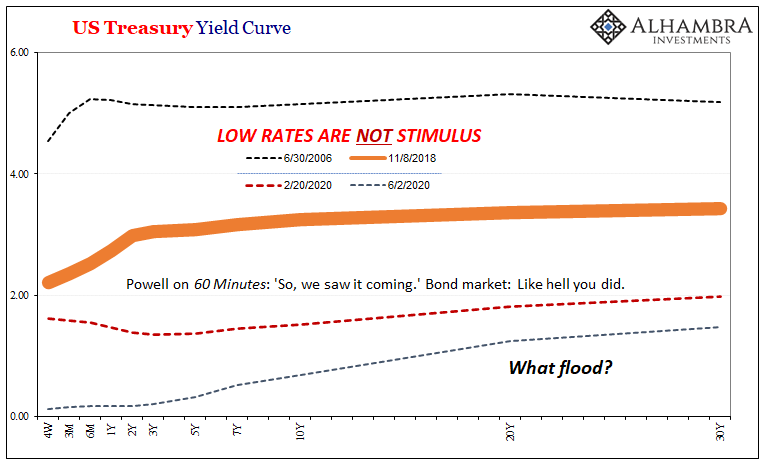

The latest fad isn’t exactly a new one, but it is likely unfamiliar to most Western observers. Yield caps are coming, and officials tell the media to tell you that this is a big deal. Why? Because, they claim, low rates are stimulus. And if the stimulus is successful, then rates will rise which will undo the stimulation.

Oh yeah, it’s just this circular.

To guarantee the success of QE (this time), whichever central bank will instead promise to keep bond yields low for the foreseeable future. They could do this with QE, in theory, but in practice yields have fallen much more without those sorts of bond purchases than with them (so much for the theory).

Plus, it’s a haze of opacity and complexity, too much for the regular folks on the street to understand. Since expectations policy depends upon influencing the expectations of the public, central bankers really do believe you are too dumb to easily comprehend and then behave in exactly the way they want you to.

A yield cap, now that’s easy for the layperson to grasp: low rates are low because a central banker says they are.

Is that really true?

Let’s answer that by first examining a recent example of yield caps. The Reserve Bank of Australia imposed them back in March 2020 during GFC2, opting for what it said was the cleaner, more efficient option than straight QE. Bond buying messy and confused, yield caps neat and simple. It’s been so successful, sayeth the media, that the central bank hasn’t had to buy a single bond in two months. Seriously:

Since setting its target in late March and launching into a flurry of purchases, the RBA hasn’t had to buy bonds for eight weeks. This benefit won’t have gone unnoticed by other central banks.

Umm, that’s not success so there can’t be “benefits” for anyone to notice. Instead, that’s the market once again disagreeing with the central premise of central bankers. Rates had risen somewhat sharply in and immediately after GFC2 because of liquidity breaking down even in government bond markets (especially UST’s, that whole collateral business). Central bankers not doing their jobs, in other words.

While officials have proclaimed a flood of liquidity in practically every currency on earth, bond yields since then instead paint a very different picture; one devoid of any flood, more deflationary than inflationary despite the flood of positive press for the official story. If the Reserve Bank of Australia hasn’t had to buy bonds in eight weeks, it’s not for the reason it thinks; or wants you to think.

In addition to being taught that central banks are central, and that bond markets must therefore obey them (see: Greenspan, Alan; series of one-year forwards), we are also taught that this inflationary bias was a product of experience. The Great Inflation of the seventies reprioritized and superseded the prior deflationary fears born from the Great Depression.

So many myths, so little time. In point of fact, central banks have always exhibited this sort of inflation bias, seeing the price benefits of their own policies in many cases where none could exist. In short, they really, really don’t get deflation.

Two primary examples which predate the Great Inflation occurred within a decade of each other, with the second spawning the current thinking on yield caps.

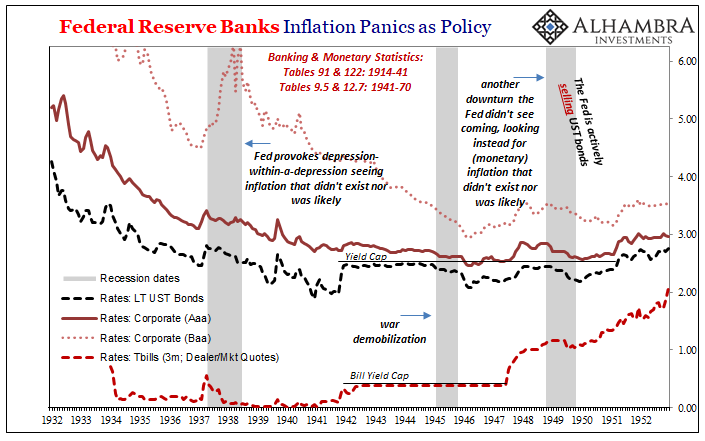

As far back as 1935, in the midst of what was supposed to have been a recovery – and a transition from the deflation of the early thirties into price acceleration of a normalizing money and banking system – the US Treasury Department had gently nudged the Federal Reserve into its corner. Fearing a rise in interest rates as recovery and inflation took hold, Treasury officials wanted a firm commitment from the FOMC to buy up especially long-term bonds so as to keep interest costs (as well as bond prices) stable in the marketplace.

The New Deal was still leaving the federal government with massive deficits, after all.

Early in 1937, the Fed actually did intervene, buying $104 million in bonds thinking the inflationary horizon had finally arrived. That was, along with its change to banks’ reserve requirement, the central bank preparing itself for the higher yield environment it had been promising all along. Hooray!

Instead, the rest of 1937 was an utter disaster, a deflationary depression-within-a-depression provoked, in large part, by insanely over-optimistic monetary policy seeing an inflationary circumstance that didn’t exist in reality nor was likely to ever show up.

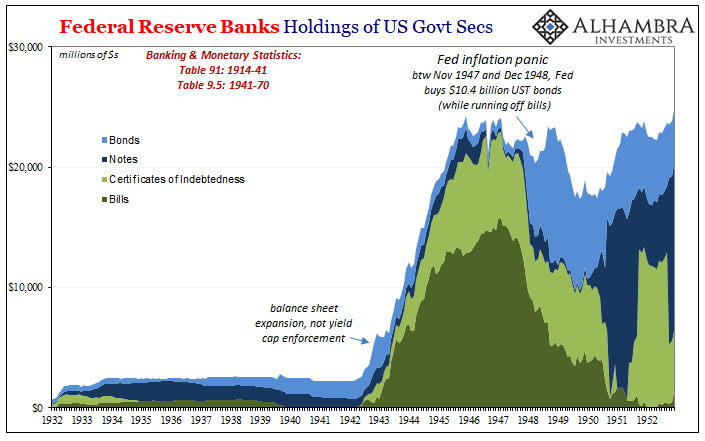

Despite that massive failure, this effort (buying UST’s at the request of Treasury) set the stage for the yield caps of the forties. In the beginning, however, these weren’t necessarily about inflation but raw supply and demand factors; the federal government was going to be borrowing at biblical levels to fight WWII and the Fed was dutybound to go along for the ride.

Treasury officials had wanted the Fed to keep short-term rates low, down near zero by, essentially, engaging in blanket money printing – a flood of bank reserves that would give banks all the necessary financial means to buy up any amount Treasury might float with a huge cushion to spare.

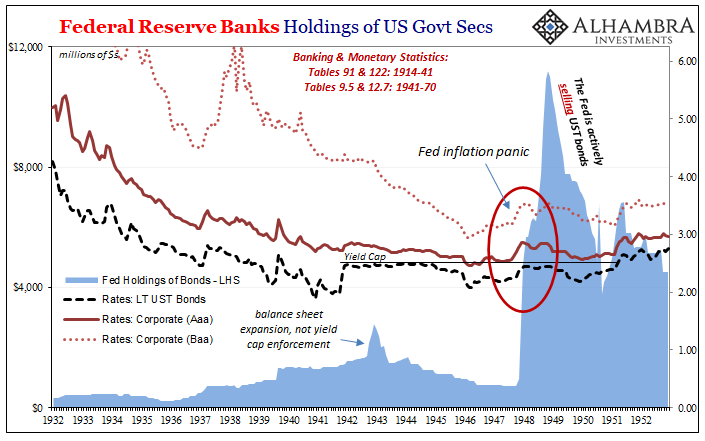

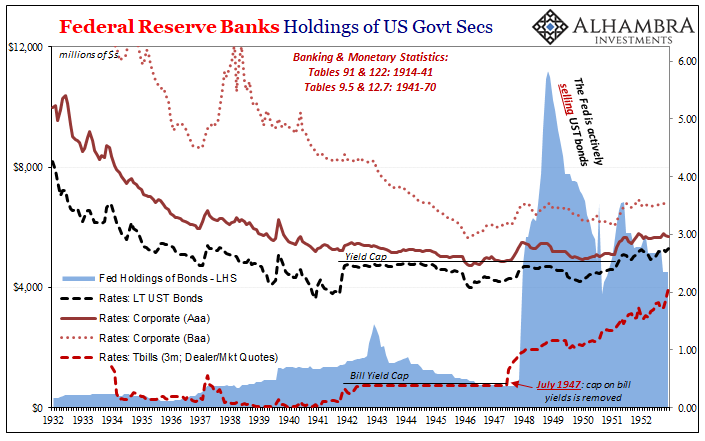

The Fed instead worried that this way of cushioning the blow of gargantuan debt supply would itself be, you guessed it, inflationary. Its experts instead preferred to let short-term rates rise while capping long-term UST bond yields at 2.50% which it believed would make sure the federal government could borrow at reasonable costs no matter the deficit.

On March 20, 1942, the two compromised with a series of rate limits starting with the bills. The Fed would buy up whatever bills necessary to hold their yields down to 3/8 of a percent (only slightly higher than the prevailing interest on them at the time). The 1-year Treasury would be limited to no more than 7/8 of a percent; 7 to 9-year yields, 2 percent flat; and long bond yields were supplied the 2.5 percent ceiling.

Treasury could be assured that its borrowing program could be conducted at predictable costs, while the Fed would only supply as much reserves as the market “needed” to keep everything that way.

Almost immediately, it led to the central bank buying up nearly every T-bill issued (along with most certificates of indebtedness, too; short-term Treasury debt maturing in less than one year but paying out coupons).

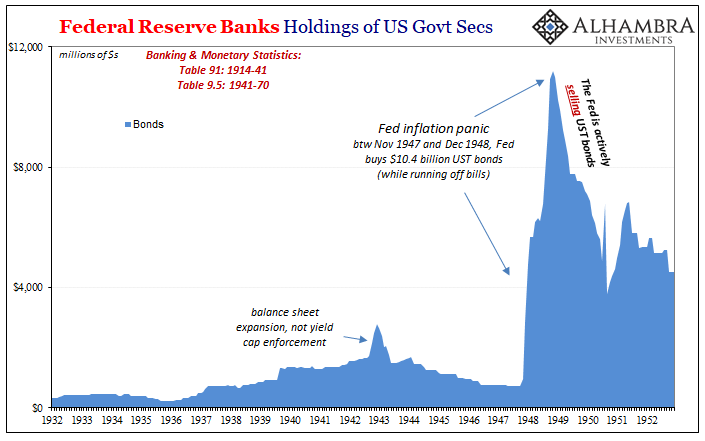

This policy would continue until July 1947 when the cap on bill yields was removed. When it was, it led to the only instance whereby the Fed was “forced” into purchasing Treasury bonds to maintain that particular rate ceiling which remained in effect (and would continue effective until 1951). Over the almost decade of this yield cap program, the only time there was any substantial bond purchases took place, curiously, starting in November 1947 and ending in November 1948.

Otherwise, long-term Treasury yields had given no issue with threatening an upward breakout.

After removing the cap on bills, those rates rose immediately – which fed right into fears Fed officials had been waiting for. They worried this was the signal for the inflation they had long been preparing for, and therefore, in addition to their commitment to Treasury, they were keen on keeping long bond yields low as a market practice. Even though, as you can see below, long-term rates didn’t actually make much (or any) move. Bumped up a fraction by rising bills, that was it.

Those who argue this yield cap policy had worked point to those purchases as holding down long-term rates at just the right moment. From there on, proving their worth, like in Australia nowadays, the market simply followed the policy, never fighting the Fed over it again.

Bullshit.

Notice on the chart above what immediately followed that Fed’s buying panic in bonds – massive selling of those same securities. The reason the FOMC began to give back more than half of what it brought in was simple – the market demand for those bonds was steady and then became overwhelming. There never was any danger of a BOND ROUT!!!, central bankers making their usual inflationary mountain out of the smallest molehill of rates backing up ever so slightly.

The Fed had, once again, overreacted to an inflationary scenario that, like 1937, didn’t exist. As it turned out, the risks prevailed in the other way.

What happened in late ’48? A really nasty recession the inflation priests didn’t see coming (just like ’37). The Fed’s 1949 Annual report admits that its selling of bonds was caused by a definite uptick in demand:

Throughout the first half of the year [1949], the Federal Reserve sold Treasury bonds from the System portfolio in response to market demand, primarily from nonbank investors.

The whole point of yield caps is, contrarily, to offset a condition where there isn’t demand so as to keep yields from skyrocketing in disorderly fashion. With the 1948-49 recession taking care of the possibility for inflation, demand simply wasn’t a problem (this should sound so ridiculously familiar).

There had been a severe spike in consumer prices beginning in ’47, but it wasn’t of the monetary variety (supply shock) which Fed officials would’ve known had they listened to bond yields rather than believing they controlled them.

Though short rates rose once the yield cap was removed, there was only the slightest nudge in longer rates (shown above) given that the bond market (corporates, too) viewed the inflation burst as temporary (even though the CPI would increase by double digits in some months of ’47) and that continued hedging (holding the safest, most liquid assets) against the downside still the priority (proven prudent by the recession).

The yield caps, therefore, immaterial to the behavior of the bond market overall during that period. And the only time the Fed “needed” to intervene it was a ridiculous overreaction because it is innately biased to see inflation risks no matter the actual condition. Today or long ago, monetary policymakers always believe their stuff works well.

That’s ultimately the lesson – they haven’t learned a damn thing; not in the forties from the thirties, and not today from all this history. They just don’t understand bonds and yields because they don’t understand money and banking. Never have (thus, Great Depression) and never will (two GFC’s within a decade, and inflationary forecasts galore in between them).

If the Reserve Bank of Australia today like the Fed in the forties really doesn’t have to buy any bonds, that’s not successful policy it is instead a warning that policies haven’t worked. Central bankers can declare a future filled to the brim with inflation, but unless and until actual market demand for the safest, most liquid instruments does fall off in reality (rather than media imagination) there’s no point to yield caps.

Not a technical one, anyone. Instead, it all comes back to the puppet show. Yield curve control, as they called it in Japan starting in 2016, is just the latest character to make its appearance on stage in order to deliver one introduced line: never fear rising interest rates.

The bond market doesn’t.

Stay In Touch