The molehills get even smaller simply because there’s never any mountains. The conventional view, no surprise, is looking at this situation exactly backward and trying to impose an idea that just doesn’t fit. Upside down, if you prefer.

A smooth Presidential election in the US plus the smooth transition into Jay Powell’s monetary ecstasy of inflation is going to bring on the BOND ROUT!!!! Foregone conclusion in all the financial press. There’s no other possible explanation because all the central bankers say so.

Therefore, any slight backup in yields has to be that very thing. Here’s the real thing, though, does this even count as a slight backup in yields? Not by any reasonable standards. Narrative, however, yields to none.

Instead, that yields haven’t risen any more than the few basis points they have completely upends the whole thesis. Undercuts the entire view, renders it an obvious fit of rationalizing.

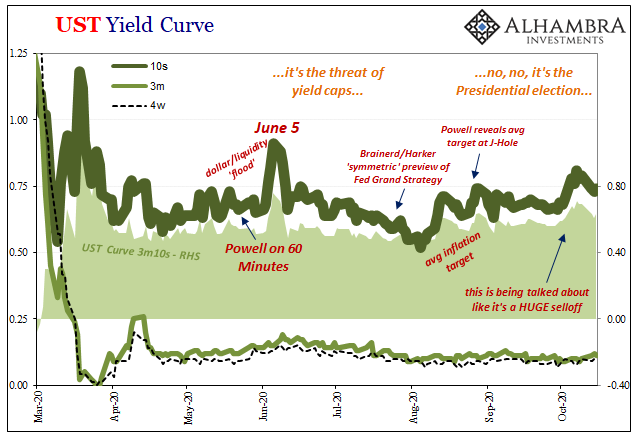

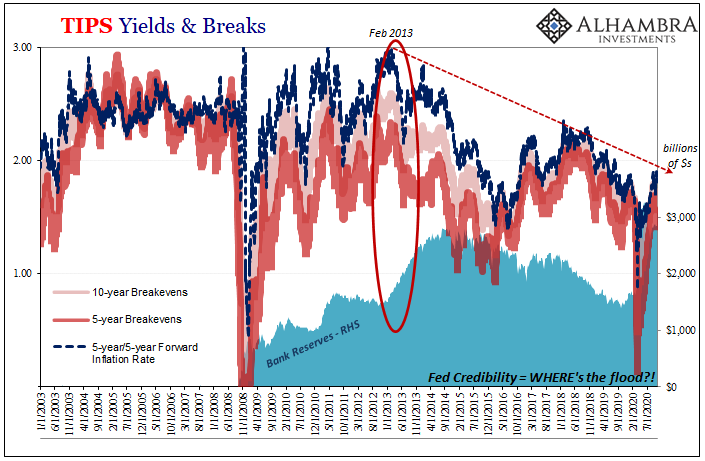

See for yourself (above). Is there really anything to be excited about inflation-wise? Not even a recognizable bump.

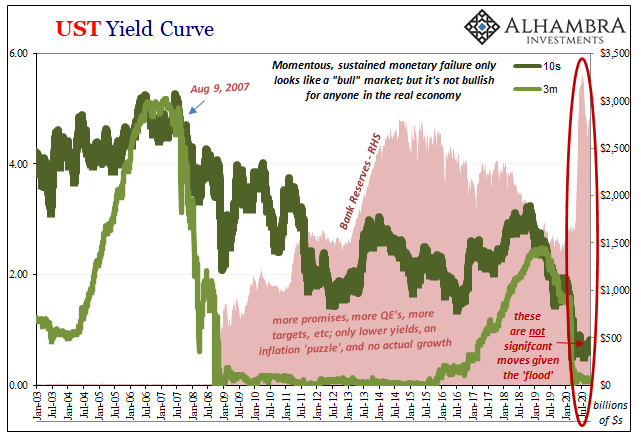

Think about it. For more than six months we’ve heard nonstop about “V’s”, the greatest global “stimulus” ever conducted, and on top trillions upon trillions in the latest grand LSAP’s. Not just one QE, either, also global and this one a huge, biblical monetary flood in every possible direction.

It’s going to run you over!

Utra-loose. Ultra-accommodative. Massive money printing. And on top, average inflation targeting which is Jay Powell saying he’s going to let it run, purposefully, just let it all overheat.

And you can see it right on the Fed’s swollen balance sheet; bank reserves have skyrocketed beyond anything in 2008. Massive money printing plus no new Lehmans. Who is stupid enough to bet against the Federal Reserve? Certainly not leveraged speculators!

For all these things, for constantly being reminded each and every day of all these gigantic, huge things, why haven’t yields moved more than they have? That’s the real question, the one everyone should be asking themselves as well as pushing to have asked of those people at the FOMC (and their cheerleaders). The highest (nominal yields) since June is actually a pitifully small change; it barely qualifies as a normal market fluctuation.

If any of this narrative has been true, these few basis points in all corners of the bond market would have been dozens of basis points – just as the start. Instead, you can barely recognize the small variability in any sort of meaningful context – even in just recent context, it’s conspicuously unimpressive.

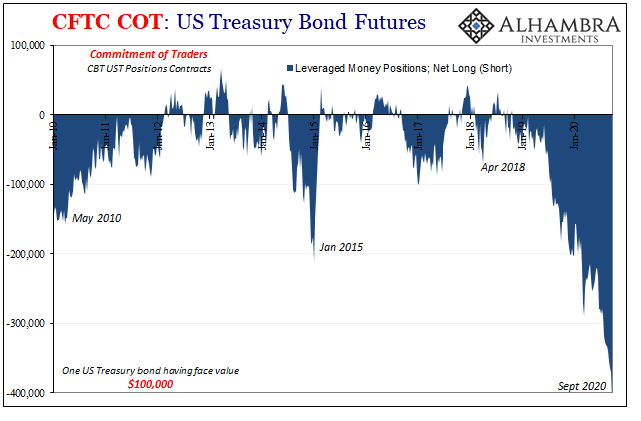

On the contrary, while this bond market continues to trade very cautiously, of course, it is in no way cautious over an inflation the Fed and its parrots have spent years predicting to no avail. Track record does still matter in some parts of the world.

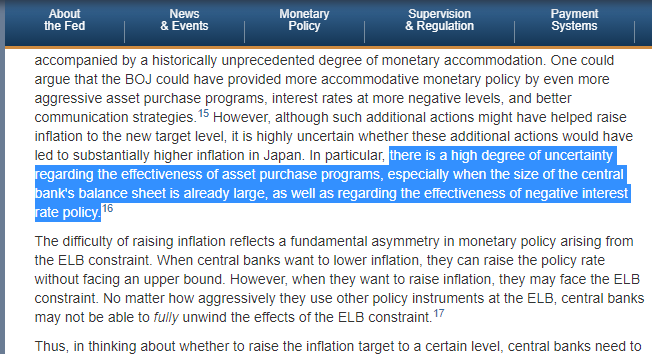

Unlike in most of the media, in these monetary markets there’s awareness of what QE (as one kind of LSAP) actually is; and it ain’t money printing. There’s even some broader recognition that central bankers themselves can’t find any evidence their programs are inflationary – and they desperately want to, even need to.

Once again, reality is the opposite; the evidence, including academic regressions, all comes down the other way. “Highly uncertain” is the most charitable you’ll see – and that’s directly from the Fed earlier this year.

“Highly uncertain” is their way of kindly praying: it hasn’t yet worked, but maybe someday it still could. Fingers crossed is no way to conduct serious monetary policy. Then again, as I keep having to write, these are not serious people.

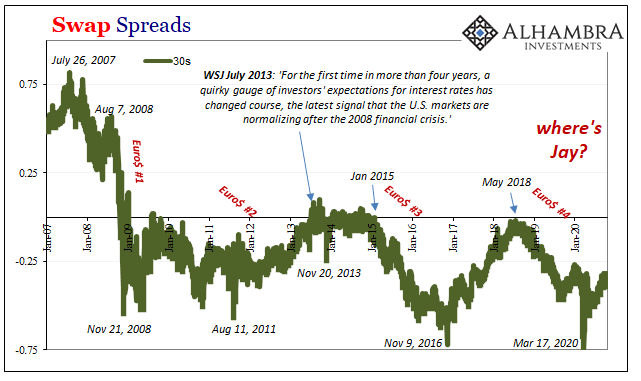

From this point of view, the narrowness of the trading range for yields (curve) makes perfect sense. While we are all taught to listen to the central bankers above everything else, the bond market and even the yield curve’s presumed “steepening” of late is very clear evidence where it actually matters QE’s and Fed officials are (correctly) being tuned right out.

This inflation nonsense is (appropriately) treated as nonsensical noise. It can make for a good story, but one that’s grown so boring and stale, perfectly, predictably fictitious.

The risks remain tilted heavily in favor of deflation. Why? Does anyone really need to ask?

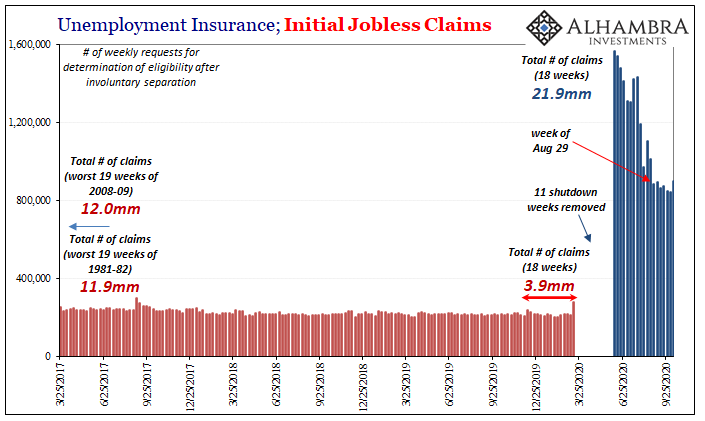

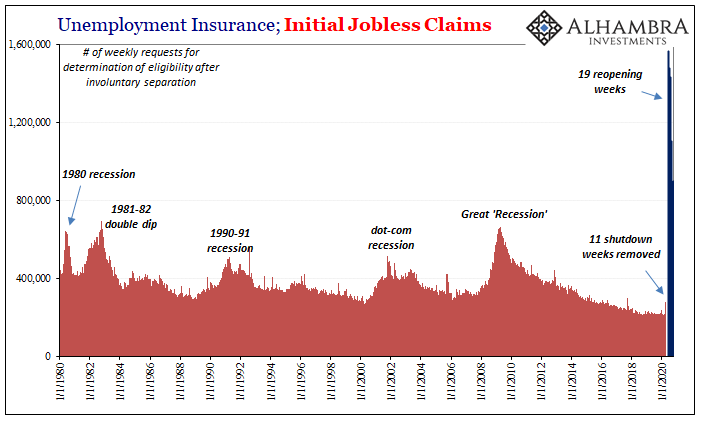

The labor market, already a disaster, has slowed and that slowdown more and more confirmed – it stopped getting moderately better leaving it immoderately deficient. Going back to the end of August, initial jobless claims six weeks later are around the same level; rising this week from last week (noting how California remains in its self-imposed pause).

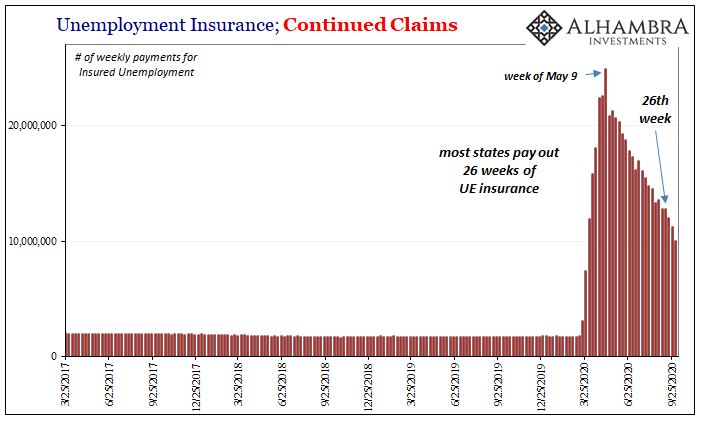

Continued claims are falling, though still remain above 10 million even as millions have exhausted their 26 weeks of payments. That doesn’t represent exclusively improvement any longer; it’s typical bureaucracy and faith in other parts of it to sort things out. You’d think 26 weeks, half a year, six months, would be more than enough time given what they always say about the Fed.

Beyond the US economy, the original “V” has already failed globally, too.

To spin this as somehow inflationary, the new “V” narrative simply views this bad news as some sort of good news because it will surely lead to more LSAP. And it certainly will; boring and fictitious, central banks therefore entirely predictable.

That’s the thing in these curiously, stubbornly low yields: the bond market has already factored this “more stimulus” by properly discounting it as anything other than what all the academic literature actually admits – waste of time.

And time, that’s the one thing we really can’t afford. QE’s, though, that’s all they do is take their time.

Stay In Touch