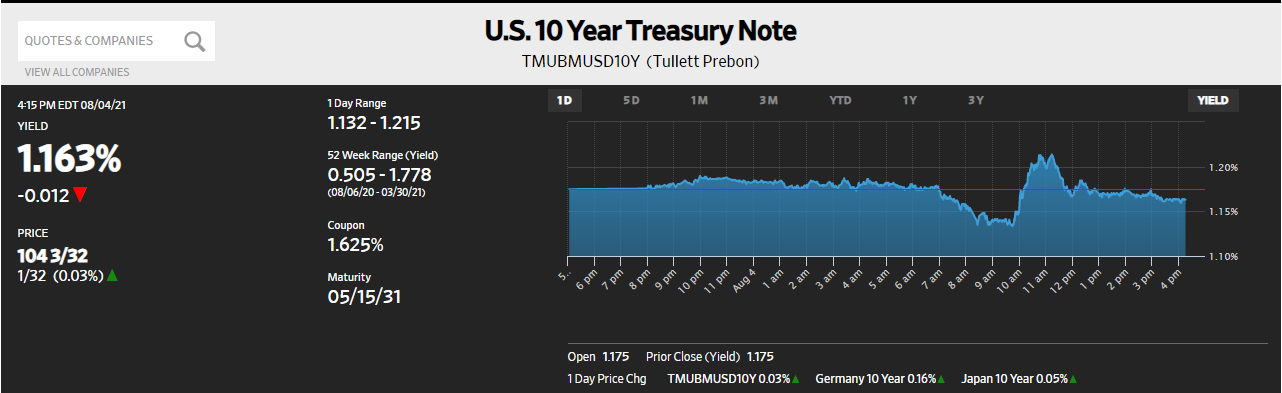

One good, one bad and by the end more the latter since the former simply bucked the trend, almost alone as an outlier (among outliers). The day started out with European deflationary pressures putting a spike on UST and related sovereign bond prices then quickly substantiated when ADP reported (830am EDT) its estimates for private payrolls during July (this was the bad).

Following an hour and a half later (10am EDT) the ISM released its figures for the non-manufacturing (services) sectors which just popped – in the good way. Suddenly, or a few minutes before the public got its hands on the ISM, the drop in yields reversed into a reflationary selloff of some decent substance.

It only lasted for a little over an hour before settling back into the pre-market tendency focusing more on the “growth scare” concerns than the lone ISM sticking out as to any possible upside argument against it. By the end of regular trading, this good news notwithstanding, punishing JP Morgan’s Jamie Dimon that much harder, yields at the long end, anyway, lower for the day.

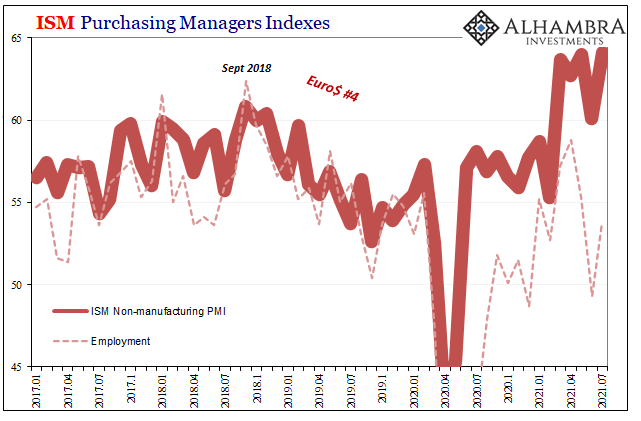

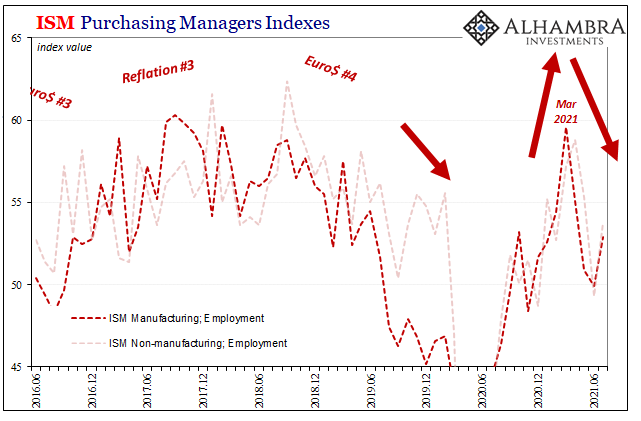

The ISM’s Non-manufacturing PMI rose sharply in July 2021, four big points, up to 64.1 and handily beating estimates. This was in opposition to the slowdown trend which the other ISM (for manufacturing) had two days ago displayed only too well.

But while the employment component managed to increase (it for the manufacturing PMI, too) there remains inside of it a huge gap between possible employment conditions and the headline which directs our attention to how these things actually work. If, say, the prices paid subindex goes even higher, getting to 82.3 last month (from 79.5 in June), which one is actually influencing that upward headline number the most?

While some might be tempted to say this is the expected disparity created by an inflation monster, no, “actual” inflation – a broad-based and sustained consumer price increase – would produce nominal economic gains absolutely requiring a huge employment jump to keep up and maintain that in something like the ISM would mean employment far closer to the headline.

Instead, going back to the (NBER brief) 2020 recession, employment and the headline have ended up suspiciously in very different parts of the charts; employment, in fact, even after July’s small uptick still down around the 2019 downturn low point. These two are actually at odds, which may be one reason why the good ISM ended up nothing more than a fleeting impact (though, admittedly, no one really knows what moves markets in the short run).

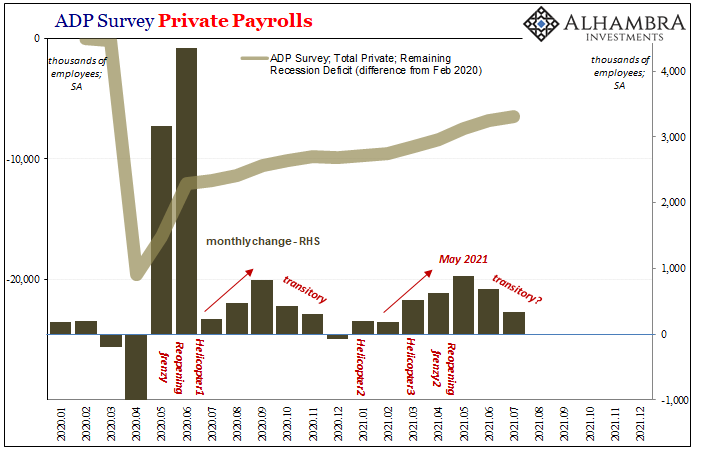

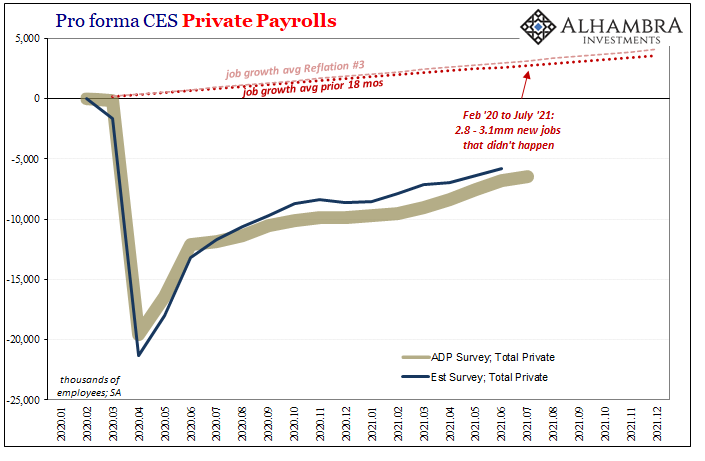

This point had already been driven home, impactfully, by the earlier ADP estimates. According to their survey of the private job market, the economy added something like 330,000 during July. This would be a relatively decent number if it was 2019; in 2021, it’s woefully inadequate.

Inadequate and therefore a little too much like the growing, more assertive deflationary confidence. This ADP corroborates this sense of another economic slowdown. Not only is +330,000 about half of what “analysts” had been expecting for July, these other were figuring private employment to have accelerated last month instead.

This updated estimated is also less than half of the revised +680,000 in June as well as way less than May’s +882,000. It didn’t just miss on acceleration, in doing so it seems to be following an alarmingly familiar pattern:

In other words, we’ve seen this before, not really all that long ago. Reopening begins a frenzy into which Uncle Sam pours trillions of borrowed dollars and, for a time, it begins to look like a robust economic situation moving briskly in the direction of real recovery.

As with any scale reflation, this is enough to get extrapolated into something it never is; fed by those who uncritically believe in the idea of “stimulus”, both fiscal and monetary. Yet, as the months go by, and as the last fed “helicopter” fades into memory, the positive impact wears right off and does so shockingly fast leaving little of longer run economic value.

On the contrary, it exposes the underlying weakness as the artificiality dwindles.

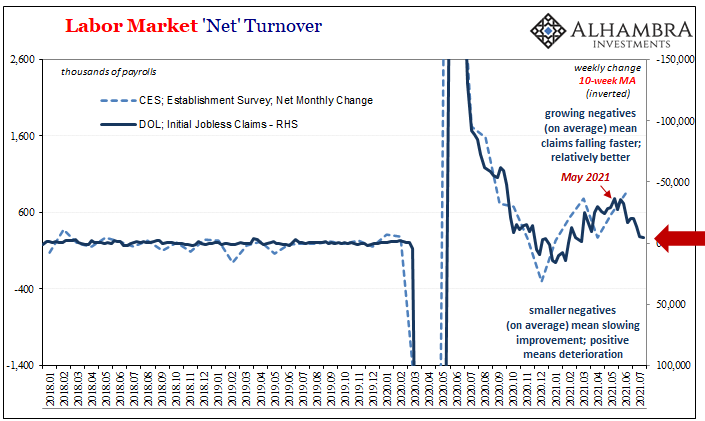

And it isn’t like the ADP is the only piece of data or evidence going along in this particular way; for the labor market, importantly, there are any number of corroborating series that each circle the month of May as a recent high point. Among the most visible of those is jobless claims.

The tally for the final week in July will be released tomorrow by the Department of Labor, and it is expected (by “analysts”) to be near 400,000 yet again. If so, or even quite a bit better, the 10-week average weekly change will have dropped down to about zero.

That average had peaked, you guessed it, back in May. Since then, the rate of improvement in jobless claims has declined to now becoming next to no improvement. This does not sound like an especially healthy situation in jobs supporting this widely expected (to many, outside of bonds, foregone conclusion) inflationary acceleration toward full and complete recovery if not more.

Putting it into the BLS Establishment Survey terms, it suggests something like April’s “disaster” of +269,000 (+266,000 private) which, you’ll notice, is much closer to the current ADP than not.

Despite all this trending in the opposite direction, Friday’s payroll figure is still anticipated at around +900,000 (which would be very pleasing to, among others, the taper talk of Governor Waller).

It doesn’t really matter the exact figures here (for monthly changes in labor data, there is an unappreciated lack of precision in them). The trends suggest one thing, with the recent exception of the ISM’s Non-Manufacturing headline.

Other than that one (or IHS Markit), particularly where it comes to the all-important labor market, recent data adds to the list of indications pointing toward not just a slowdown but one predicated more so on the transitory and increasingly likely inconsequential effects (after all, this isn’t the first time it might end up this way) in the real economy from even the largest of the federal government’s helicopters.

This is then added to a global picture in which all the above is actually, by far, the best situation within it.

If the Friday Payroll Ritual does end up disappointing, as these things suggest, it won’t really be about the specific headline monthly change (even as I expect the Household Survey to rebound from last month’s negative). While we really don’t know what moves markets intraday, the ISM made Treasury shorts like Mr. Dimon happy but not for very long because, at the end of “the day”, employment, more than anything, is what truly moves the real stuff in economy as well as finance.

Stay In Touch