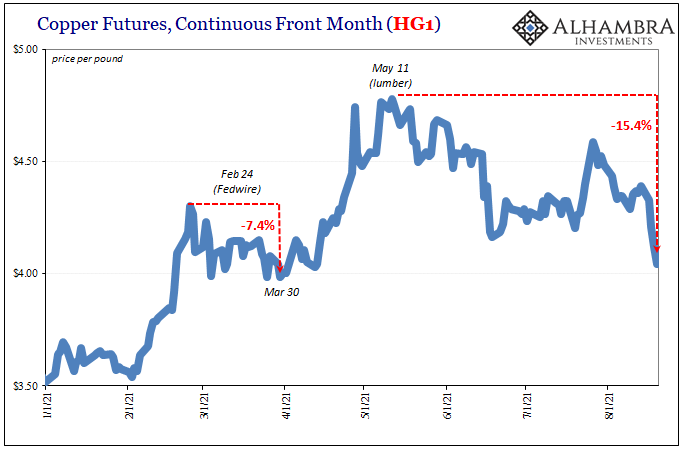

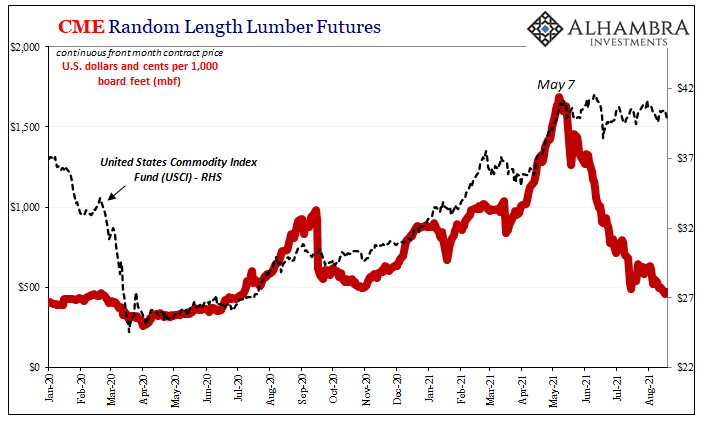

Copper, like lumber, had been the star of the space. Each had rocketed upward beginning last fall representing, for many, the leading edge of the inflationary wave sure to follow. The two garnered that much attention as well as given this much importance because the rest of the commodity class hadn’t really come close to matching their meteoric scale.

It was supposed to have been copper and lumber fronting the way and then all the rest of the “real” prices following behind. An inflation warning from the trailblazers then committed and backed up by everything else in due course.

This would only have been the case if real inflation was ever the reason for price behavior all around. More and more it is apparent this was instead a supply story, especially in the cases of our starry pair.

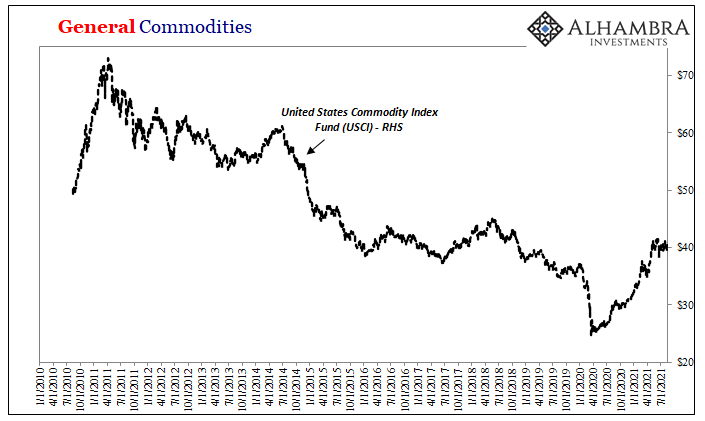

But it is no longer entirely about oversupply. There is always the other side to keep in mind, meaning demand. Supporting the price trends for these commodities as well as the others, if to a lesser degree, had been the imbalance drawn from both sides. Limited supply for rising demand, for some rapidly rising demand.

A little bit more supply comes on, and prices fall. Questions then begin to stir about demand, whether it is even going to be stable let alone still harried, and prices really then adjust.

In other words, these commodity leaders have suddenly become more like the bond market than they had been thought of just a few months ago when the unbreakable face of the coming Great Inflation #2.

Foiled by delta coronas?

It may be tempting to put the fate of our feature commodities in the hands of the politics of pandemic. By doing so, the inflation narrative is somewhat preserved in that this would mean once delta runs its course (if it isn’t already; see: UK) commodities can easily and quickly restore their demand picture and thereby go back on the side of seventies.

This growing growth scare of late, however, isn’t so much “of late.” In fact, it has been growing for quite some time, and in joining the bond side copper and lumber are the latest to be caught up in uncertainty which goes back far further in time than deltas and lambdas.

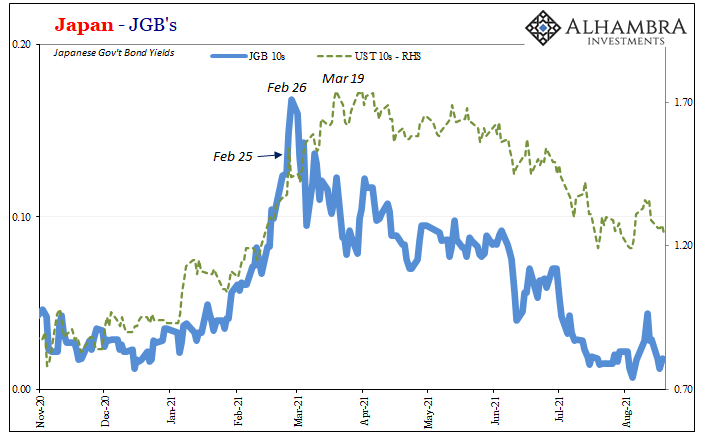

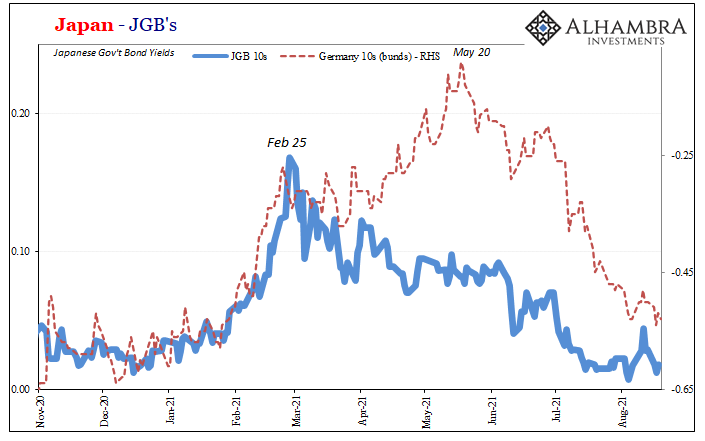

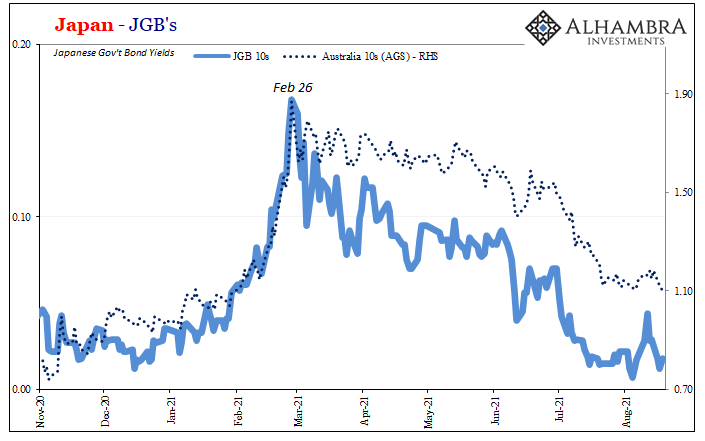

Going global, meaning global factors, the reflation inflection toward deflation and the lack of demand the latter would bring about, all that potential nastiness dates back to mid-March in UST’s and late February in a whole bunch of other places. Commodities, therefore, late to the party (supply factors superseding).

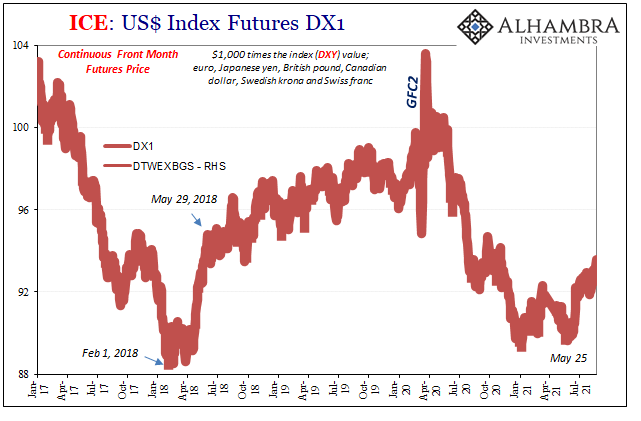

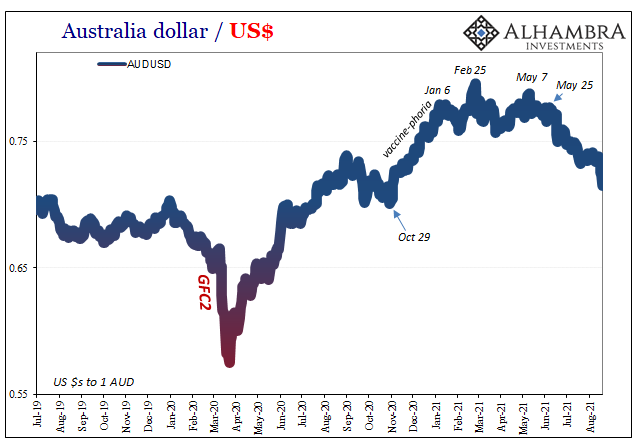

Now comes the dollar. I wrote in early July how it might have been a positive sign the dollar hadn’t yet “joined” yields.

On the flipside, though, this stubborn dollar along with the direction of global yields completely refutes any chances for inflation. That much is clear, with both bonds and currencies in agreement about the global (yes, global) factors underlying clearly still disinflationary/deflationary tendencies.

But not yet the wrecking ball; in a sense it’s good that the dollar hasn’t moved higher more than it has. Yields are down, and maybe things turn around before the dollar joins them in repeating the rollover pattern taking everything down again.

Nuts to that now.

With the dollar renewed in its bid (meaning growing monetary tightness), throw in these leading commodities now leading the way down toward deflationary again, and the signposts on the road to that more determined deflation are expanding and becoming more numerous as well as significant. It’s not that copper like lumber is now a different thing, they’ve joined the big thing already long in its progress.

Six months is more than long enough to raise more serious suspicions because it reduces the chances of random noise. Despite this half year of begrudging belittling, what stands out are both the length of time as well as the constant near-uniformity during the period. Assets and data are more and more getting pulled into this post-February downturn orbit, rather than in the direction suggested by something like recent headline US labor data.

Commodities not so much COVID as merely the latest to succumb to a much deeper and more structural demand and eurodollar problem. Now with the dollar on the move higher, the chances of “maybe things turn around” even after delta dissipates are looking less likely by the day – balance of probabilities being priced this way in these more numerous markets.

Stay In Touch