Two on the same day, likely not coincidence. The next stage of “dovishness” may be upon us. It won’t be rate cuts; those won’t happen until all other excuses have been exhausted first. Jay Powell’s confused gang won’t give in until kicking and screaming there’s really nothing else left.

The Fed “pause” isn’t working. To up the ante a bit, in speeches yesterday Fed Governor Lael Brainard and Minneapolis branch President Neel Kashkari extolled the virtues of symmetry. Inflation has been undershooting for so long (not transitory, then?) the Fed should allow it to accelerate to the upside for nearly as long. Symmetry.

The idea is the central bank will “grant” the economy license to overheat for an extended period. As Kashkari said, “For our current framework to be effective and credible, we must walk the walk and actually allow inflation to climb modestly above 2% in order to demonstrate that we are serious about symmetry.”

In mechanical terms, what they are really after is inflation expectations. Always expectations. By saying this, they hope the markets will begin to adjust current thinking to account for higher future CPI numbers. That in turn will, in theory, reduce real interest rates in the here and now. Stimulus, these people call it.

Puppet show, I say.

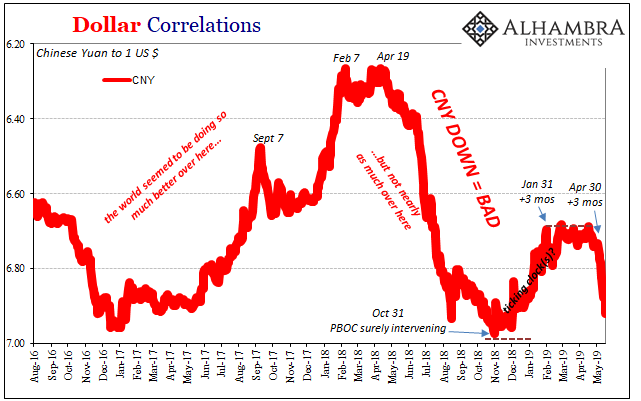

They are determined to do everything in their power to avoid the only topic that matters – which today just so happens to be CNY again.

To reiterate, CNY DOWN = BAD not because CNY is down rather why it is down. When China’s currency falls it’s not some PBOC-determined export stimulus nor is it “capital flows” adjusting to interest rate differentials as the bond market is massacred by recovery.

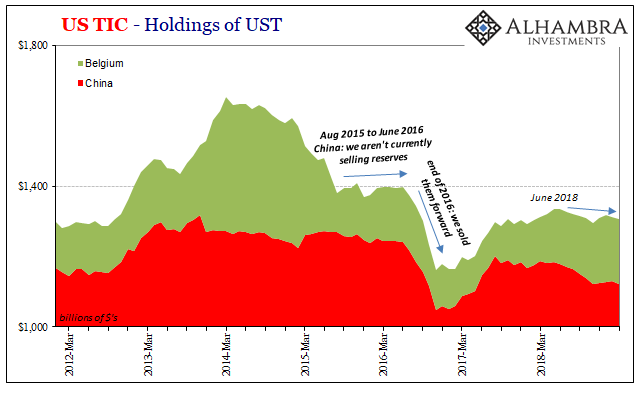

In fact, whenever the Chinese get to selling their UST’s two things will happen. First, the media will become filled with stories about how that’s bad…for UST’s. Back in November, “bond king” Jeffrey Gundlach was saying that very thing. Citing a mismatch between supply and demand, reduced foreign appetite for US debt was supposed to be another nail in the bond market’s deep coffin. BOND ROUT!!!!

The 10-year UST yield was about 3.19% when Gundlach reiterated his bearish thesis. It is a little under 2.40% today.

It seems counterintuitive if only at first, but when foreigners are apt to sell their US$ holdings that’s hugely positive for bond prices especially duration. That’s the second thing, which I wrote about also last November.

It was a global dollar shortage, another one, which in the end raised liquidity therefore economic risks. The “selling UST’s” was easily offset by, what was it the FOMC said earlier this year, “strong worldwide demand for safe assets.” The two things go together, are inseparable. Dollar shortage is UST positive (price).

And that gets us back to CNY. China selling (or otherwise mobilizing and disposing of) its stockpile of UST reserve assets is tied in with the same thing which makes CNY DOWN so BAD. Dollar shortage.

Therefore, no surprise when money is tight liquidity tends to be, too. Risk is way up. The safest and most liquid assets are bid, more than cancelling out Gundlach’s (and Jamie Dimon’s) presumed, but wrong, supply and demand mismatch. As I often write, long term people are right to be very worried about the fiscal state of the US government but you have to survive tomorrow’s potential collateral call from BONY first in order for that to matter to you and everyone like you.

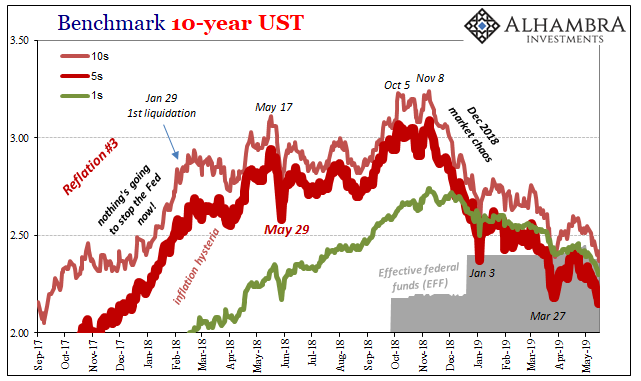

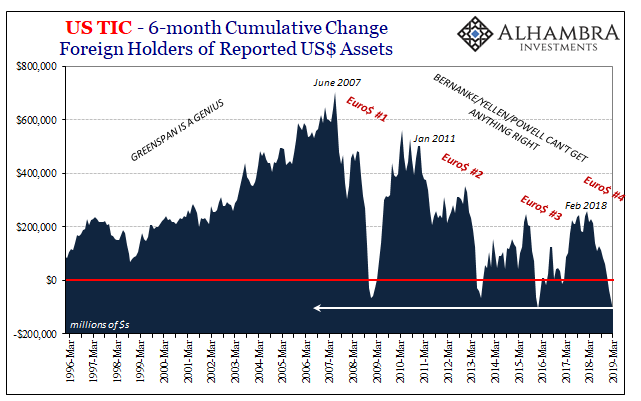

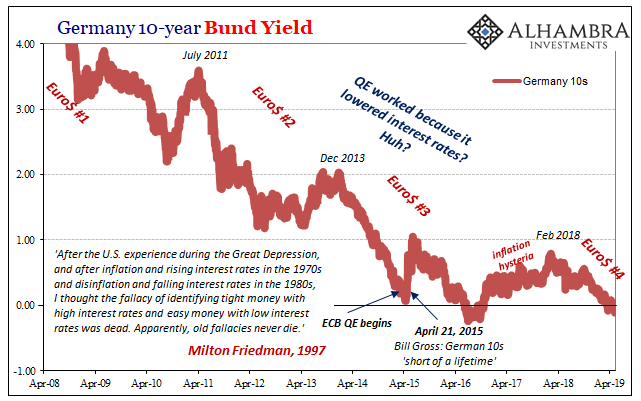

Demand isn’t a problem for bonds in these times – or bunds, as noted earlier today. While Germany and Japan’s government bonds have been trading higher in an almost unbroken trend since last October, the US equivalent faces an important obstacle to joining them.

Back to November:

The only wild card in 2018 is the Fed’s limited influence on the short end. The long end is disagreeing with Jay Powell’s sunshine, unemployment rate optimism; has been for more than a year. There’s enough gathering monetary evidence (and now economic evidence) for a (of a) renewed systemic dollar shortage in 2018 to do so – especially after May 29.

Regardless of dollar shortage, a 10-year yielding about the same as federal funds or IOER means bond market participants have more choices than normal. You can put money in 10s or maybe lend instead in federal funds (perhaps even alleviating some of the recent severe dryness in that barren place).

What that means is for the long end of the UST curve to join the middle of the curve as well as its German and Japanese bond counterparts, the dollar shortage will have to become more severe so as to make the choice between buying 10s or investing in EFF no choice at all.

We already see some of that happening, again, in the shorter maturities. The 5-year at 2.17% is an abomination to every dovish concept. It’s eight basis points less than the RRP. The 52-week bill has been flirting with 2.30%, perhaps even more of a severe indication about strictly monetary policy (meaning, ultimately, rate cuts as the final, futile dovish gesture).

The dollar shortage must therefore already be severe if not yet overwhelming. How it gets to this later stage is the self-reinforcing nastiness typical of these money-driven downturns. Eurodollar squeeze takes hold of the global economy, it slows which only confirms the negative impression which brought out the squeeze in the first place. This leads to further monetary tightening (non-policy) and therefore even more of a drag on the global economy. Rinse. Repeat as needed.

CNY can be an important indicator along those lines, where dollar shortage is first seen as bad but not overwhelming then transitioning toward HOLY SH&%. That’s when everyone piles into the 10s (2s, 7s, 20s, 4-week bills, and everything in between) no matter what Lael Brainard, Mario Draghi, or Larry Kudlow says about whichever labor market statistic.

Right now, according to TIC, the Chinese are moving UST’s around – not a particularly good sign. About $10 billion left China in March, but $4 billion showed up in Belgium and another $5 billion or so in Hong Kong. Still ticking that clock, perhaps, even as the last two appear to have run out together (the driving force behind CNY’s current move).

All of this stuff is connected. Brainard and Kashkari can’t figure out inflation so they offer a slightly reworked puppet show than the one that’s been acted before. Meanwhile, the Chinese aren’t signing up to be mildly entertained, they need dollars the eurodollar system won’t supply which the presumed stewards of the US dollar won’t admit actually exist. In a nutshell, that’s how you lose an entire decade and more of global economic growth.

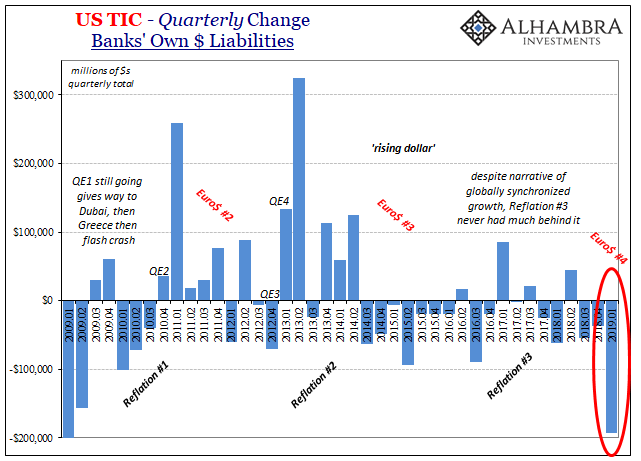

It’s also how you get a nastier fourth eurodollar squeeze.

A world starved of the monetary resources does only what it can, the very thing the technocrats and bond kings can never seem to grasp: strong worldwide demand for safe assets. If you aren’t an Economist, you are free to surmise how nothing good happens from there no matter how many doves of all different species are haphazardly stuffed into the puppet theater.

Milton Friedman deserves a lot of crap, but also a ton of credit. This is definitely one he got right. If only monetary policymakers would spend their time figuring out money.

Stay In Touch