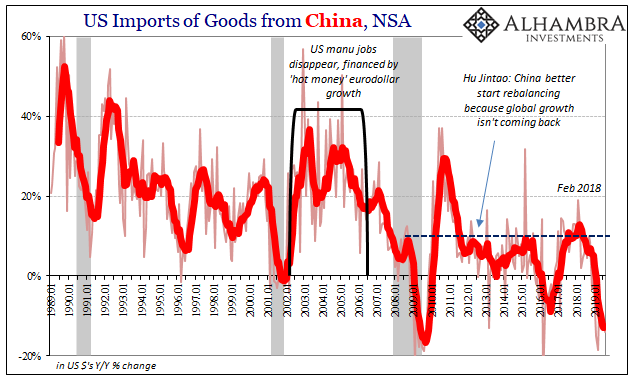

There is no doubt that US tariffs on Chinese goods have negatively impacted US imports of Chinese goods. According to this week’s updated estimates from the Census Bureau, imports from China were down 13.9% in August 2019 compared to August 2018. That was the fourth straight month of double-digit year-over-year declines, and six of the last seven months that bad.

For the Chinese.

These are some of the worst results in the entire series. Bigger declines for China than during Euro$ #3’s pronounced global trade suppression, and about equal to the depths of the Great “Recession.” On the narrow goal of making the Chinese suffer, and thereby forcing them to bargain from a weaker position, the President’s plan seems to be working.

In macro terms, that wouldn’t have much to do with overall US imports. Trade wars are redistributions; if Americans now don’t want to buy Chinese goods because they are more expensive thanks to increased duties, then, all else equal, those famous last words for Economists, Americans will find someone else to buy from. Demand soldiers ever onward.

China’s loss is someone else’s gain – so long as the American economy isn’t suffering, too. The White House’s goal is simply to redistribute production back in our direction, to bring a sizeable piece of the industrial base back home.

But that’s not happening, either. US consumers aren’t just consuming fewer Chinese goods, they are consuming fewer goods period. The manufacturing recession is on, and it’s already global.

These downward pressures are variable, meaning that for some it’s already been much worse (Germany) and not getting better while for others their economy is still scraping along with no upside and too many stubborn downside risks.

If the US economy was otherwise healthy, and not in that latter category as we keep hearing from officials like Jay Powell, there would be no reason total imports are now falling at substantial rates. Not only would US importers seek alternative routes for their supply chains, the “strong” US dollar makes goods produced anywhere other than China that much more attractive, too.

Indeed, that is the case for European imports. With the euro lower, and no strong “trade war” vibes being sent in that direction, inbound trade from Europe is still averaging better than +7% through August. But even that is down from where it was last year though the dollar has only moved higher.

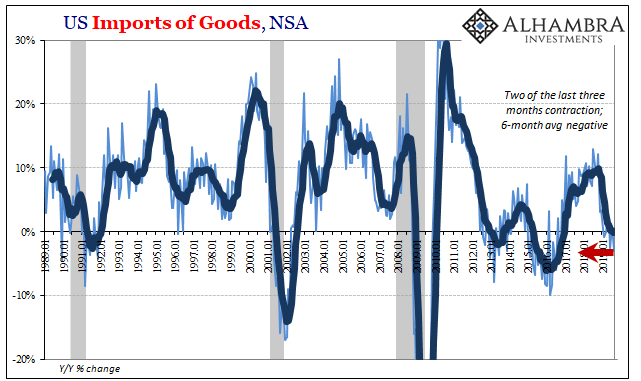

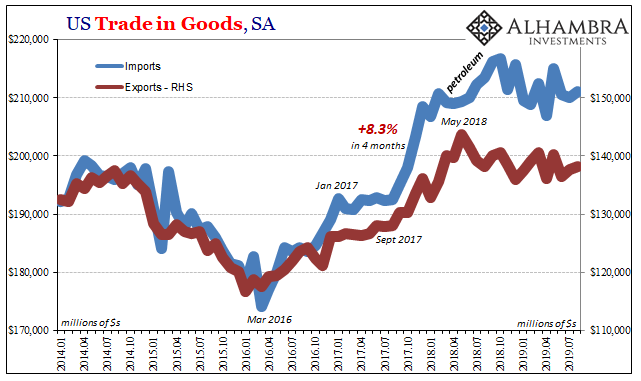

Total imports from everywhere around the world coming into the United States declined by 3% year-over-year in August. While certainly buying a lot less from China, in the aggregate the US is also buying less foreign products overall. Minus three percent may not sound like much, but it puts US demand on pace for at least Euro$ #3. The 6-month average for imports turned negative for the first time since December 2016.

Like everything else, it’s not just the direction it’s more so the rate of change – and from when the condition seems to have changed. Import growth, a pretty decent proxy of overall US demand for goods, peaked in October 2018. Once again, the landmine.

And just to emphasize and clarify, US economic demand hasn’t shifted in this direction, either. At the same time, in the same way, and pretty much to the same degree, US-based manufacturing has turned lower, too. The second part of Trump’s plan isn’t coming to fruition. The Chinese are getting hammered but there’s no evidence that has pushed production back inside the US borders.

US manufacturing isn’t suffering near as much as the Chinese, but as we see in sentiment surveys there’s a lot more wrong than right in 2019 than 2018. It’s as if the entire global economy, regardless of tariffs on Chinese goods and Chinese retaliation on US agriculture, has suffered a downturn.

Perhaps a synchronized one.

That explains the inconsistency between exports and imports as far as the dollar’s exchange value goes. Again, a “stronger” dollar might explain the inflection on the export side (as well as the timing, May 2018) but not imports. But it’s not really a strong dollar, rather it is the sudden eruption of the dollar problem, the global dollar shortage, that banged the foreign sector before it eventually began to affect the domestic economy, too.

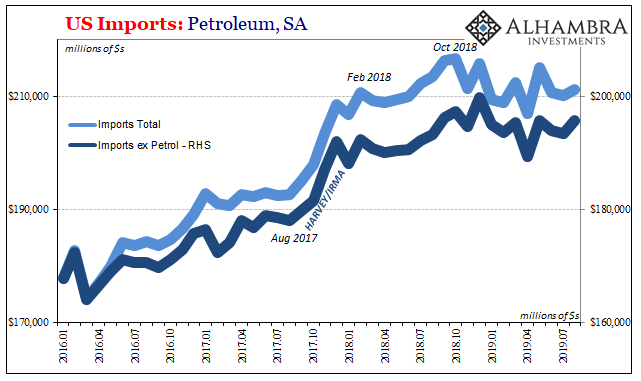

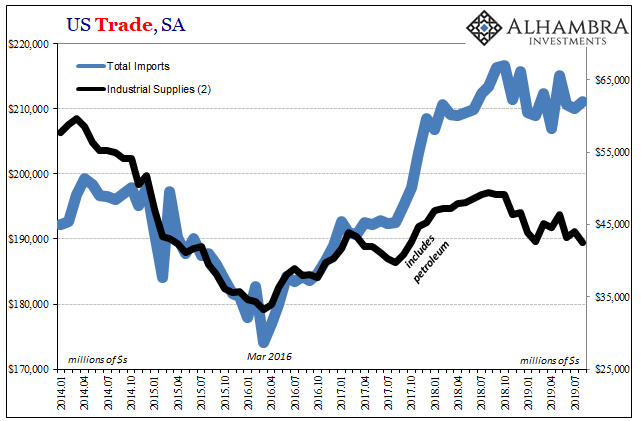

The way in which that seems to have happened, meaning imports, is through the oil patch first and foremost. Not only does the lower oil price mean a lower value of what crude the country still brings in from the outside, it is also disrupts (again) one of the few positive supply side trends in the economy. The only place actually booming and building is now retreating and spawning liquidity questions (collateral).

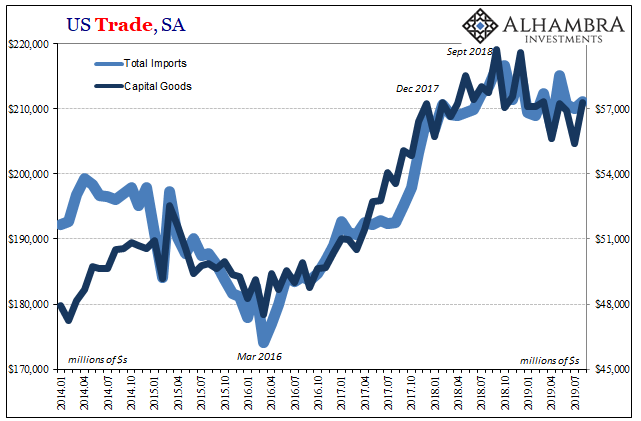

Imports of industrial supplies, which includes petroleum, are lower this year but so are imports of capital goods. These, too, date back to the landmine.

Recall what happened in the early parts of the landmine, right in October 2018 at the peak. I wrote about it then, how everyone at the time wanted to pretend it wasn’t happening:

We’ve seen this all before. The oil curve shifted to contango last on November 20, 2014. It was ignored then, too, and after catching some reluctant notice immediately dismissed as a supply glut in favor of data showing the “best jobs market in decades.” The payroll reports four years ago were just too lovely to set aside for this impossible, according to Economists, ugliness.

Guess which one proved more valuable in assessing the way the global economy was headed, US most definitely included.

History doesn’t repeat, but it sure does rhyme. The WTI curve moved out of backwardation right at the top of the landmine in October 2018, and like Euro$ #3 it hasn’t been the same since. Trade wars are happening and are having their effects, but it’s really been Euro$ #4.

That’s the only way to bring in all three dimensions: global, downturn, and synchronized.

Stay In Touch