Physical cash vs. bank reserves. Quality growth vs. quantity. Xi Jinping vs. everyone not onboard with Xi Jinping. All three contests are actually very simple and straightforward – once you let go of the strong economy, money printing Federal Reserve nonsense. As to the last of the trio, Emperor Xi has been awfully keen this year to redo government flags.

Communists are big into such symbolism.

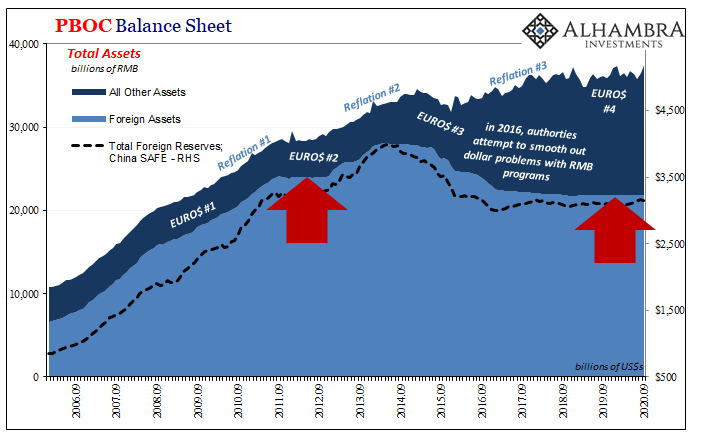

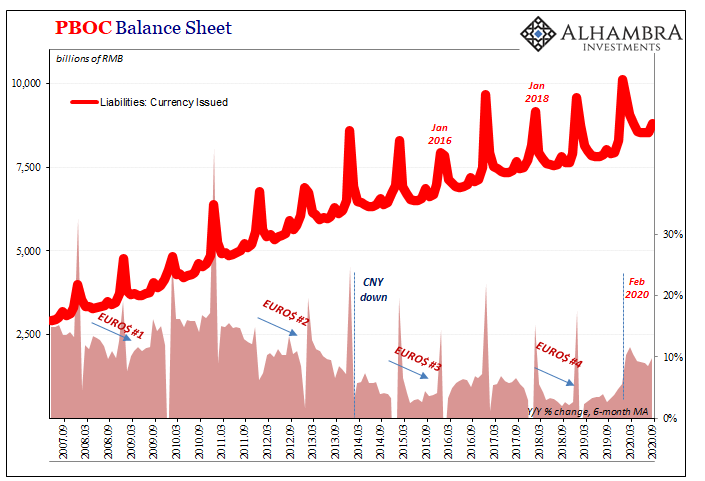

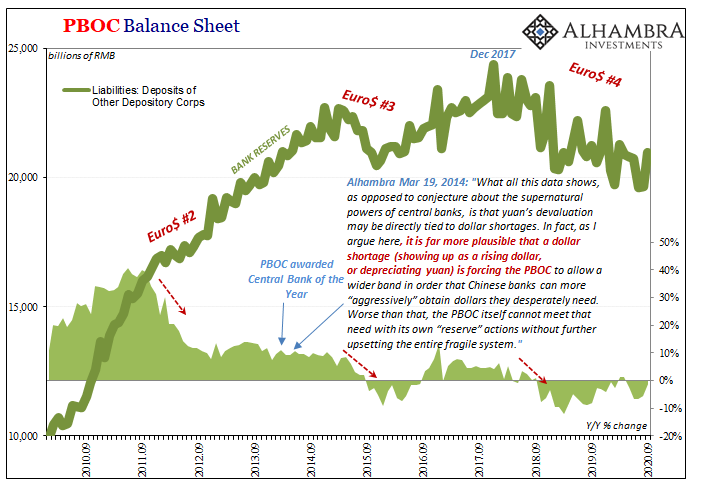

What isn’t mere symbol, at least not in the same way, is Chinese cash. Renminbi seems like it should start with the People’s Bank of China (PBOC) but it actually doesn’t. Big Mama, as she’s sometimes called, has been experiencing big problems for more than half a decade. What that has meant for the central bank is suddenly fewer “dollars” show up on its balance sheet’s asset side.

It’s been a difficult and serious setback that belies the banality of my description. Unlike the dollar system which depends exclusively on private money creation, the Chinese monetary system actually does have a central bank. And the lack of money creation throughout the eurodollar without a central bank has meant for China a lack of money creation options left to its.

Monetary systems throughout the world during the (benign neglect) eurodollar era had been heavily dollarized; this is why there even is a Brazil strategy to begin with. Foreign reserves are not strictly reserves; they are the monetary basis for local currency regimes, China’s more than anyone else’s (the nightmare scenario).

Simple accounting, then, if there aren’t the same amount of “dollars” flowing in, which the PBOC had taken into its accounts and converted them into RMB cash or bank reserves (actually both pre-2014), then the liability side must suffer the same fate. That’s where those bank reserves and physical cash come from.

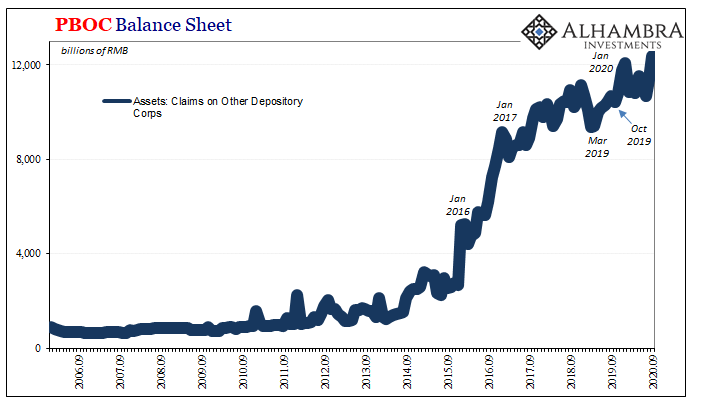

This leaves China’s monetary authorities with only the one choice, and it has been activated exclusively on a single central bank asset-side line item: Claims on Other Depository Corporations. Included within are liquidity programs like the MLF and SLF, direct lines to the banking sector. Why isn’t a whole lot more going into them?

It had never been used so much (the MLF, for example, wasn’t put in place until 2014; just in time) until around 2015 when Euro$ #3 began wrecking Chinese monetary circumstances. Trying to “supply dollars” to local Chinese corporations (financial and non-financial) the eurodollar market (from Tokyo) increasingly would not necessarily had meant a form of real (as opposed to the Fed’s imagined) quantitative tightening.

The net result was depriving the banking system of reserves (hoping that RRR cuts would offset these; spoiler: they didn’t) at the same time substantially straining the growth rate of physical cash available. The combination of these things along with the lack of recovery in the eurodollar system for China (as well as the rest of the world; the rest of the world would need a little longer to figure this out) had meant 2017’s globally synchronized growth was never more than hollow boilerplate sloganeering.

Xi Jinping responded accordingly: at the 19th Communist Party Congress that October, he promised China would change its ways, following a course set for “quality” growth instead of pursuing the highest “quantity” as the country had since Deng Xiaoping’s famous Southern Tour.

Translation: without a recovery in the global economy, the same bubble strategy pursued by his predecessors amounted to suicide. No more huge “stimulus” through either fiscal or monetary channels; 2016 was the last go-round. Those had proved little more than wasteful and quite a lot potentially dangerous (the Japan 1989 fear).

In that sense, the lack of monetary growth while a huge curse in some ways it had been a blessing since it fit with cracking down on bubble possibilities. There will be no runaway money creation even through the MLF or other windows on that one asset line. The PBOC will have to be creative and restrained, do just enough to keep China afloat.

And afloat means quality growth – and a whole lot of fingers crossed that such quality in economic progress ends up being “enough.” Look at the charts above and ask yourself why aren’t the Chinese going gangbusters in their banking system?

Xi’s status as unchallenged leader cements this doctrine as unchangeable.

Therefore, anyone who was thinking China was going to bail out the world economy with massive “stimulus” in 2020 hadn’t been paying attention. This isn’t about to change in 2021, either. Dual circulation, as we discussed previously, is a further nod to more of the same heavier “discretion” in fiscal and monetary settings.

What the latest batch of numbers from the PBOC’s balance sheet (September 2020) show are three things: still no reflation, dollar-wise; cash bumped up to aid struggling real economy; leaving bank reserves down yet again meaning Xi is purposefully avoiding the kind of “stimulus” favored still in the financial media’s imagination.

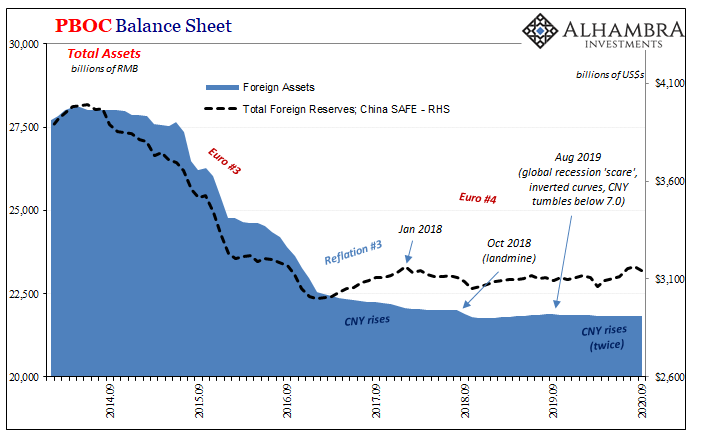

First, the balance sheet figures are absolutely clear how there are no “dollars” coming in which there absolutely would be if the eurodollar system was expanding beyond the most modest reflationary conditions (like those in 2017). Instead, September saw yet another minimal change (though down to the lowest in a year and a half) in forex assets which can only mean being engineered (not necessary if the “dollars” were flowing in).

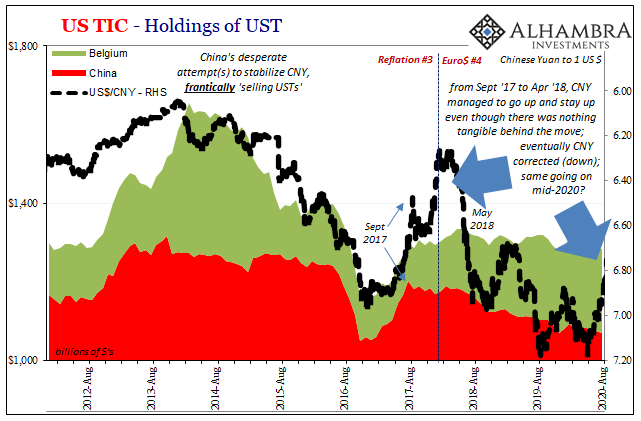

It leaves CNY’s recent rise as exposed as it had been late in 2017.

Second, without growth in “dollars” and forex, the central banks must operate given the same constraint on the liability side which monetary authorities clearly will not surmount via Claims on Other Depository Corporations. They are only raising the level of total assets (RMB plus external) just enough based on whatever minimum amount is necessary and nothing more.

The increase in growth rate for currency only to just barely double-digits is an acceleration but a suspiciously modest one (amounting to seven months now, so it’s pretty clear there’s a limit imposed). In 2010 and 2011, by contrast, currency growth averaged mid- to high-teens.

Third, what that has meant post-February is physical currency growth at the continuing expense of bank reserves; very clear priorities. The former has been bumped up in response to China’s economic woes this year while the latter continue to contract despite that same background which has strained the banking system.

Even in cash vs. bank reserves, in the troubled year 2020, you can still observe Xi’s mandate for quality vs. quantity. Prioritizing a small bump in cash growth – even when it comes through ostensibly bank windows like the MLF – shows that China is mostly interested in supporting the real economy (quality) where physical cash gets used rather than bank reserves for the financial economy where those can be amplified into the bubbles (quantity).

One final note, it should be perfectly clear by now how there’s absolutely no possibility whatsoever for RMB to replace the dollar as any kind of even regional currency bloc let alone full-blown global reserve. This goes way beyond Triffin’s Dilemma; the PBOC just won’t create near enough currency, nor will it allow the banking system onshore (forget offshore) to create any RMB. Case closed.

And that’s why Yi Gang and other PBOC’s officials have been arguing instead for SDR’s this year. Chinese money has no shot. None. I wrote more than a year and a half ago:

Chinese monetary authorities are telling us that not even they believe RMB is ready for anything like a reserve currency role. If it was, they would start to break out of these eurodollar-imposed constraints and print RMB as necessary. A lot of RMB printing would be necessary. The very fact that they did (2016-17) and now don’t (2018-) demonstrates how China’s central bankers have come to believe domestic money constraint (sharply declining bank reserves and slow to no growth in currency) is the lesser of the two evils.

They might be wrong about that, of course. Still, if yuan was poised to take over a more central role in global money you would definitely expect those closest to it to be a hell of a lot more confident about it than this.

Nothing has changed since I wrote that. Not just about RMB and the global reserve, also cash vs. bank reserves, quality vs. quantity, and Xi’s increasingly unchallenged status. These all uniformly point in the same direction since 2017. As does, not coincidentally, the global economy. Still synchronized and global, of course, just not growth.

COVID and 2020 didn’t alter the plan one bit. If anything, it appears the greater shocks and challenges which have arisen have only emboldened and confirmed (for Communist authorities) these choices. It is, sadly, still the eurodollar’s world.

Stay In Touch