Blame Milton Friedman for this one, too. The economist made many significant contributions to the advancement of economic understanding, but perhaps an equal number of extreme errors. For one thing, that whole bout with bank reserves and “high powered money” (what became QE) recommended in the late nineties to cure Japan of its obvious monetary illness. This followed from the conceit that monetary policy and central banking would always offer positive, meaningful contributions.

The biggest blunder of them all, however, was Positive Economics. Begun long before Friedman, there had always been this idea that as a discipline Economics could fashion itself in a way more familiar to the hard sciences like physics. An economy can be precisely clocked, standardized, and then studied. This has been believed from before the time of Irving Fisher, going all the way back to Simon Newcomb and even John Keynes – Neville (father), not Maynard (son).

Once all the relevant factors are chosen and dissected, these could be watched regularly and then manipulated in order to transform economic aggregates in predictable fashion. Powerful mathematical equations then designed to govern both the choosing and predicting, taking the “artwork” out of this often-tortured study.

Friedman merely took things a step (or five) further in the fifties.

In 1953, Friedman published perhaps his most scholarly book, Essays in Positive Economics. While including other authors, the lead essay was Friedman’s The Methodology of Positive Economics which remains his most cited academic piece of inside baseball. The first sentence of the essay quotes John Neville Keynes’ 1890 Scope and Method, recognizing the substantial “confusion” between positive science, normative science, and art that has been “the source of many mischievous errors.”

Buoyed by further “advancements” in the sixties and seventies, particularly Robert Lucas’ rational expectations equations, the result was neo-Keynesian (Maynard) econometrics – that which today governs all mainstream opinions on any topic even remotely associated with economy or finance.

And it did not take very long for some quite astute observers to recognize how it had all gone very wrong. Positive Economics had intended to be the set of guiding principles to lead the transformation into a true science but instead had gotten itself entangled in other matters only tangential to what was supposed to have been the focus of the whole damn effort.

Don’t take my word for it, here’s Nobel Laureate Ronald Coase saying exactly this while accepting that very prize.

This neglect of other aspects of the system has been made easier by another feature of modern economic theory – the growing abstraction of the analysis, which does not seem to call for a detailed knowledge of the actual economic system or, at any rate, has managed to proceed without it.

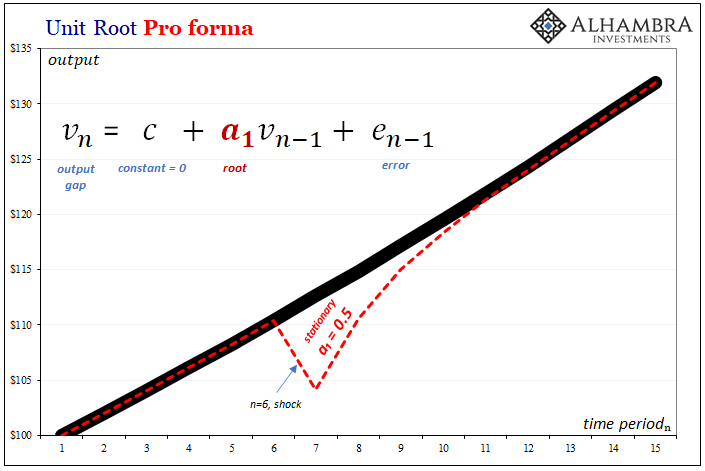

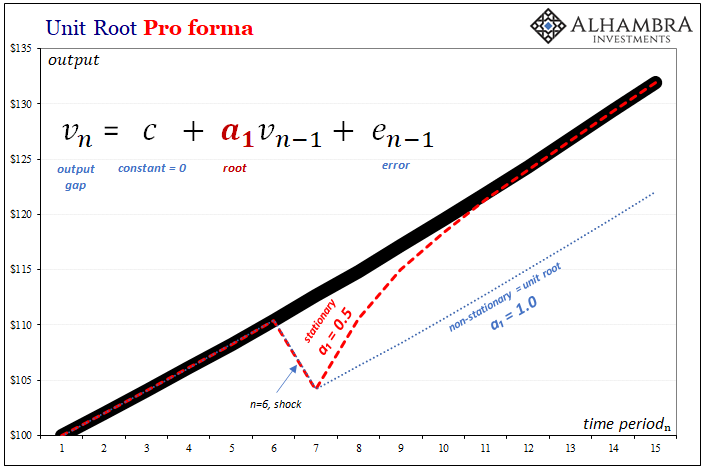

Thus, the father of modern monetarism, Friedman, had come to believe (plucking model), violating his own principles, that permanent shocks to any industrialized, central bank-guided economy had been eliminated from even consideration. Hard-wired into econometric equations, there would (could) be no unit roots among the variables – as a matter of rationalization rather than rational science.

This has had practical as well as statistical effects; of the latter, econometric models that, since around, oh, 2008, can’t get much right; of the former, the public at large left largely in the dark about why this is and more importantly what it truly has meant.

We’ve been left with the impression that the economic situation is always binary; the economy is in recession or recovery/growth. No other choices. Believing this, everything becomes a simple matter – including the most important part. In other words, all you have to do during contraction is wait for it to end. If there are only the two options, once an economy’s reached its ultimate trough all worries can be set aside.

Because it can’t be anything other than recovery leading to growth from then on.

Introduce unit roots, however, or go back and think about what they really mean, and the entire situation can become permanently screwed real quick.

Permanent shocks upend everything.

Inflation is only the first clue. As I write often, it’s not really about consumer prices so much as the assumptions behind why they’re often supposed to rise – and when. In most situations, including our own, this means what’s actually going on in the labor market.

Back when Inflation Hysteria #1 was really starting to fall apart, in September 2018 just before the deflation of the landmine erupted and inevitably ended its influence, you could already tell by an honest reading of labor and economic conditions that a permanent shock (2008) explained everything Federal Reserve Chairmen one after another failed to time and again:

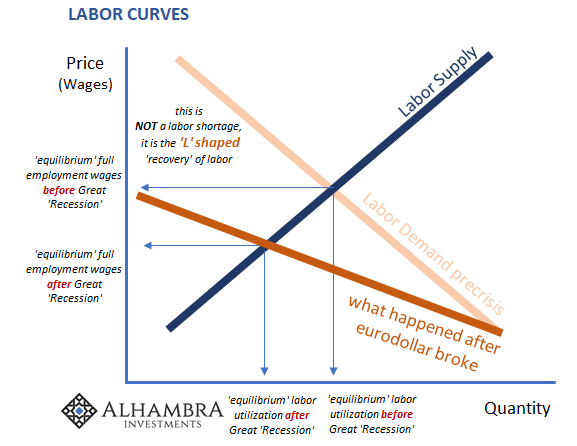

Is it a shortage of workers, or a shortage of work? Structural issues with Americans and who they are, or macro issues about which Americans have been fed a load of crap for more than a decade? You can see why those who may have been manufacturing raw manure might have an interest in swaying the debate toward the structural. Or preventing the debate from happening at all.

A shortage of work manifests itself very differently than a shortage of workers. In the former, employers take a languid approach to securing employees. They are in no rush because there is no rush. Business is tepid so in most cases, why bother?

Though the media howled (on first Yellen’s and then Powell’s behalf) about some LABOR SHORTAGE!!!! there was never any evidence for one – apart from an unemployment rate that month after month failed to be corroborated by anything even as it sunk lower and lower.

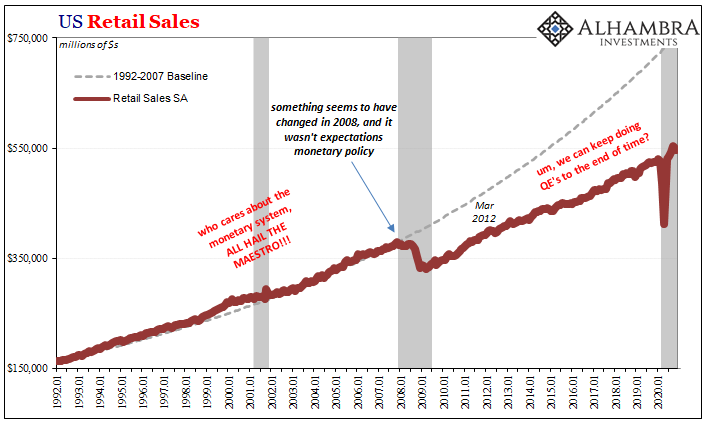

A big part of the issue misidentifying the truth comes back to Positive Economics and econometrics, this assumption that there can’t be permanent shocks. The last recession had clearly finished up years ago, and from the very moment it ended (Bernanke: “green shoots”) the official narrative played up the idea recovery was guaranteed. If there was any variation, it could only be in the time it might take to be completed.

Now Positive Economics has stacked one egregious error on another; having yet come clean about what really happened in 2008 and why (it hadn’t been a Lehman problem really at all), this binary belief remains pervasive in the public mind.

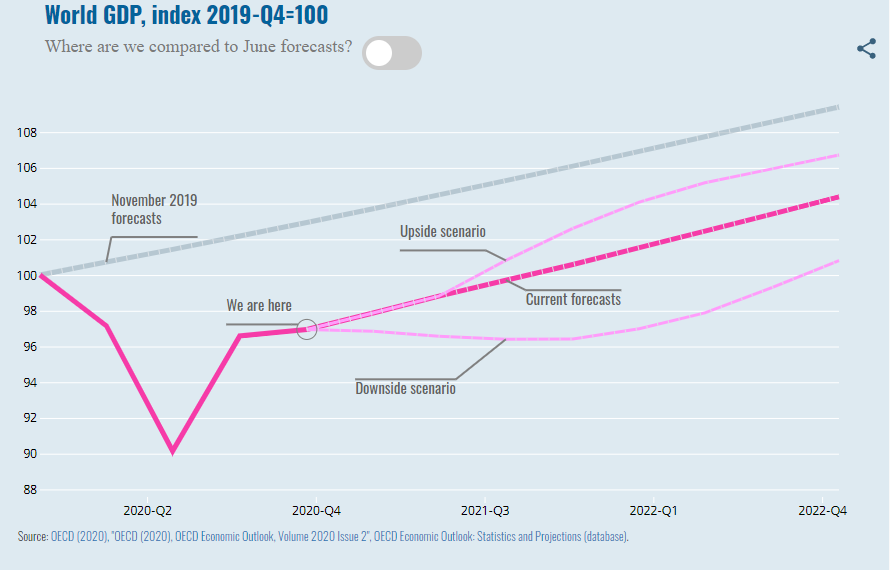

For 2020, then, same huge mistake; the contraction ended back around May or so, therefore it can only be recovery from here on. This belief permeates everything even after the decade and a quarter we just experienced had already disproved the thing.

Thus, inflation is widely believed the only way forward because the “business cycle” has turned, a bottom had been reached meeting the binary requirement; with this inflationary inflection having taken place more than a half year ago. The bad stuff, apart from pandemic, the negative economic factors must have all been put comfortably in the rearview.

Have they, though?

COVID gets all the blame, a convenient out for officials still unwilling to answer for more than the economic devastation now obvious this year. I missed our sadly regular Thursday ritual last week, so here it is just in time for the holidays and yet more grossly ineffective and misguided fiscal “stimulus”:

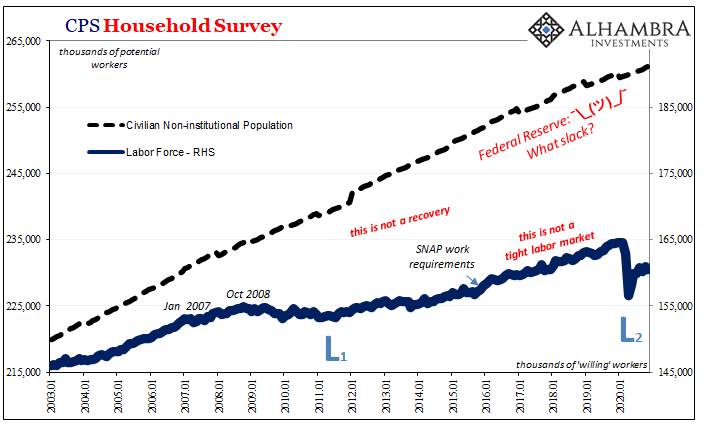

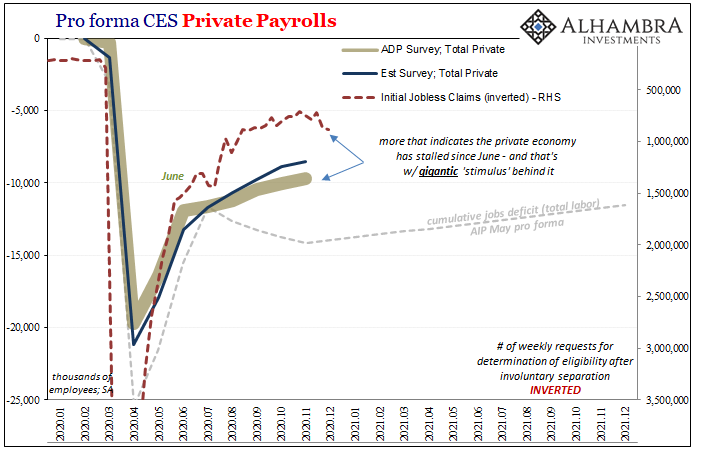

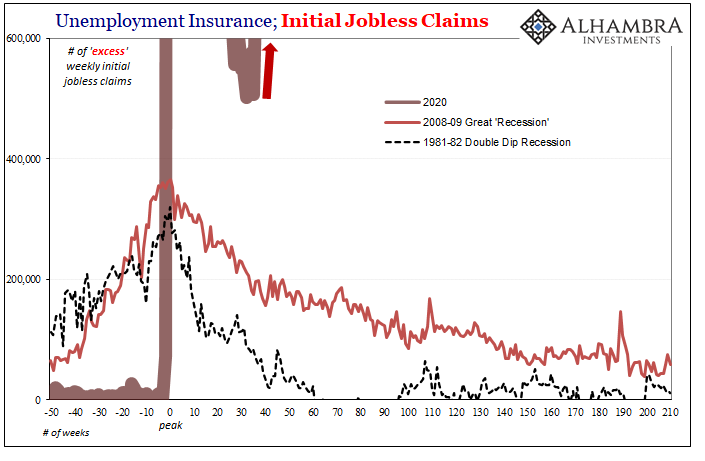

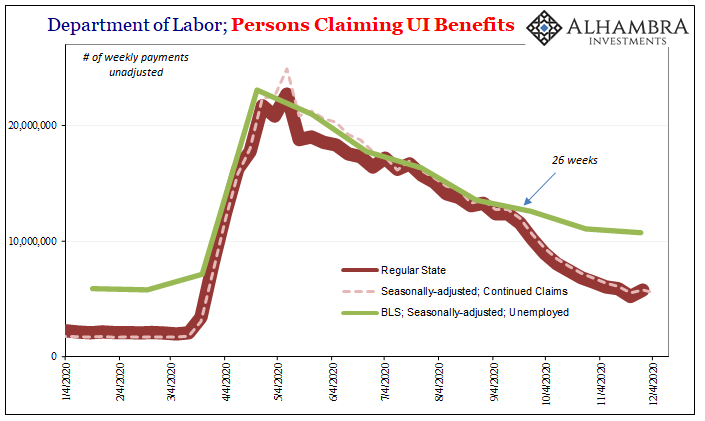

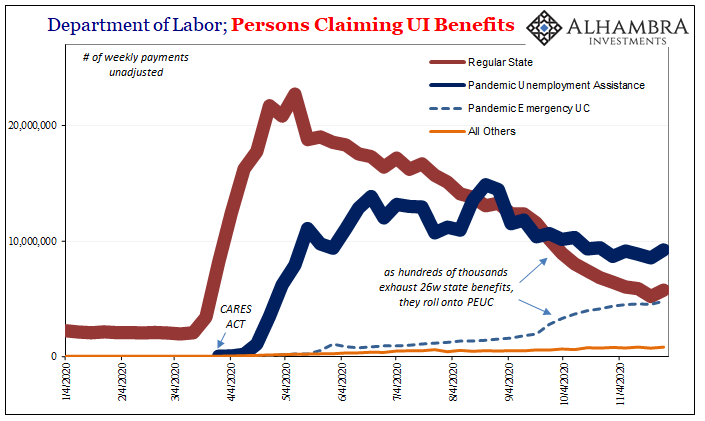

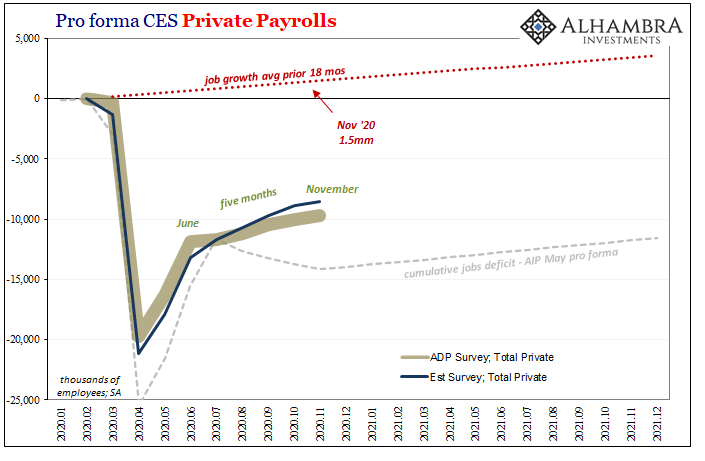

The level of destruction in the labor market continues to be unfathomable, and not just because of the huge absolute figures. More to the point, the amount of time nowhere near anything remotely recovery-like is staggering. And that’s just not pandemic and hyper-reactive governments.

Is it a shortage of workers, or a shortage of work? Structural issues with Americans and who they are, or macro issues about which Americans have been fed a load of crap for more than a decade?

More crap. Recognizing this, and all the tell-tale signs (GFC2) of another permanent shock, it wasn’t exactly a difficult leap to have written back in late March:

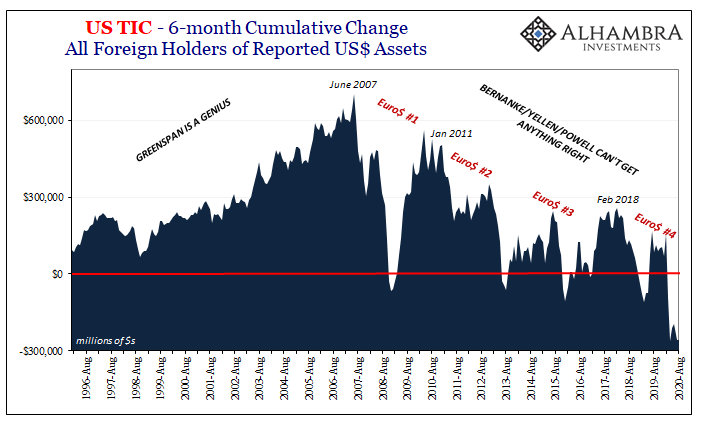

The Federal Reserve has shot all its bazookas, from endless QE to unlimited “repo” operations and finally overseas dollar swaps. Doomed to failure, all of it; the dollar swaps supposedly such a big piece aimed at fixing the global part of the dollar shortage have been open and operational this whole GFC2 just like GFC1. What good were they?

Once this thing is over, American workers need to realize…they’re going to get back to work more slowly and, unless something meaningful changes very soon, ultimately fewer of them will.

Friedman was wrong as have been all his, and John Maynard’s, disciples. Permanent shocks were never defeated by technocratically competent central bankers adhering to the noble but futile (see: Mandelbrot) attempt at Positive Economics. Instead, they rode a eurodollar wave for as far as it would take the globalizing world; taking credit for it the entire time (Greenspan put? Come on!). Without that exogenous monetary wave, a permanent shock of epic proportions, it’s workers who suffer the deflation.

The worst of this latest contraction did indeed end more than half a year ago. The common assumption says – hooray!!! – it’s all recovery from there. Nope. The evidence demonstrates conclusively otherwise.

For now, Inflation Hysteria #2 will dominate the headlines and nothing else. Again.

Stay In Touch