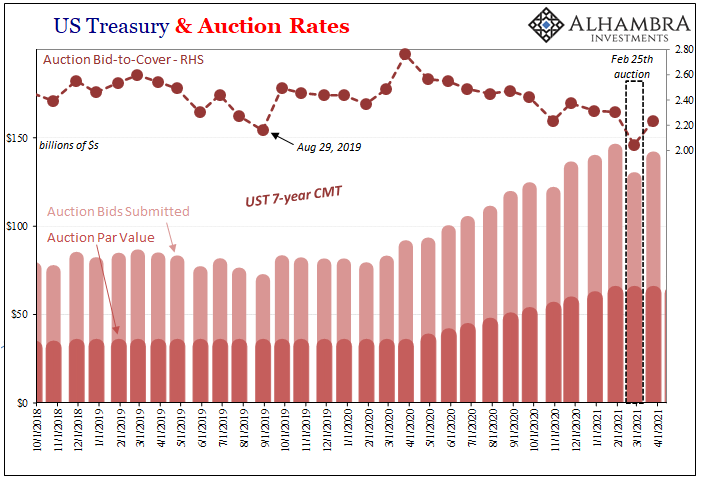

The US Treasury Department announced today that it has completed an auction of 20-year bonds. Quite unlike the one 7s auction – you know, that one – this particular bond sale was positively uninteresting. Like all the rest of the bills, notes, and bonds since February 25, there an overwhelming number of bank dealers and other participants some of whom seem hellbent on paying any price for the paper.

The low accepted yield today, which represents 5% of all bids, was practically zero, just 8 bps. Demand for long bonds yielding barely more than 2% continues to be thorough even as, discussed yesterday, US central government debt levels skyrocket. Making (debt) matters worse, the US economy only ever shows signs of slowing down as it has for nearly a decade and a half.

How can this be?

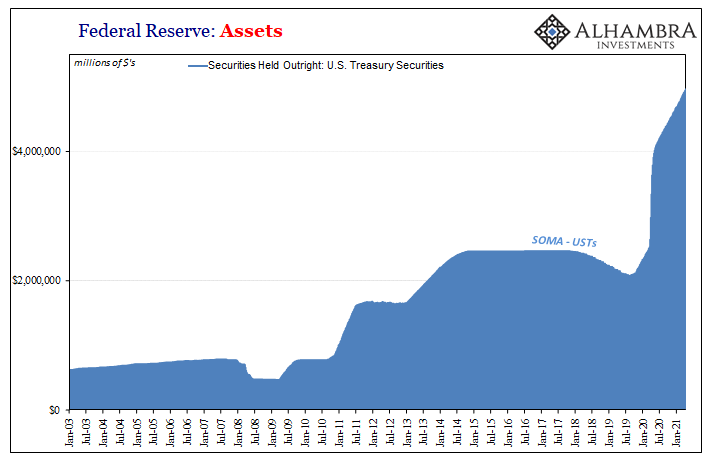

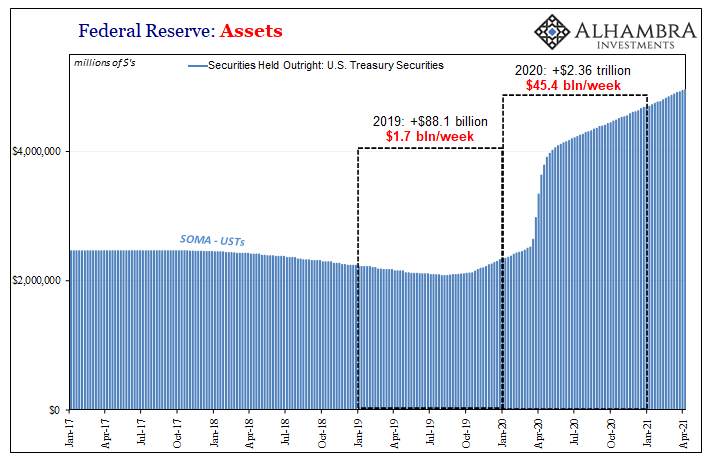

Some say that it is the Fed which is artificially inflating demand for Treasuries (and other asset classes) due to its own bond buying programs. This latest LSAP, or large scale asset purchase, otherwise known as QE6, has seen the central bank’s SOMA holdings of notes and bonds (though, curiously, very few bills) explode upward by $2.5 trillion since last March.

Yet, even the central bankers know this isn’t the reason for stubbornly low yields on these securities. As I’ve endeavored to point out as often as I possibly can, the academic literature, most of which has been sponsored and written by central bank staffs, is conclusive. I still love the way the Reserve Bank of New Zealand just comes right out with it:

Studies found the government bond purchases worth 10 percent of GDP have, on average, lowered 10-year government bond yields by around 50 basis points.

Underwhelming, isn’t it? Pitiful, actually.

The Federal Reserve’s purchases over the last thirteen months are only a bit larger than 10% of GDP, thus, best case, bond yields are just 50 bps lower than perhaps where they otherwise would have been – if you take this average view at face value. Arguably, and there’s much data to support significantly less than this, the reason why most of these papers use “term premiums” as a standard for measuring QE impacts, the effect on yields is negligible.

Even if we account for somewhere between zero and 50 or so bps, that still means US Treasury rates are ridiculously low otherwise; demand easily sustained (as the auctions results demonstrate, one after another with the single exception).

What is this demand?

As usual, we’ll leave it for Richard Fisher (of all ex-FOMC officials) to explain:

MR. FISHER. In summary, I want to mention that, as I said earlier, most of these variations that have been suggested are very un-Bagehot-like. And what I mean by that is, twisting [or QE and yield caps] entails purchasing assets that investors are fleeing toward, not assets that they are fleeing from. [emphasis added]

This is why the studies show only limited effects directly on yields – because the market has reduced them far, far more than QE ever would, will, or can by itself. The questions, therefore, are who and for what purpose(s) are doing the “fleeing toward.”

Rather than being a possibly neutral proposition, here we begin to see and appreciate its rather insidious downside. What I mean is, even if the bank reserves that QE creates as the accounting leftover of what is nothing more than an asset swap don’t really help (and they don’t), that doesn’t necessarily mean it can’t hurt to try anyway. It absolutely can hurt, and more recent investigations are starting to clue in on this as-yet unacknowledged aspect.

A recent one of these, published late last year, claimed the following:

…a $33 billion dollar increase in weekly Fed purchases leads to a 0.5 increase in the collateral chain.

What that means is, understanding how QE removes bonds from dealer inventories as its part of this asset swap, these kinds of LSAP’s strip the marketplace of valuable and usable collateral. More bonds for the Fed, more bank reserves for the banks, less collateral out there in the world overall. We’re only supposed to think about the reserves.

Since we don’t live in a static, ceteris paribus world the dealer system must somehow overcome this policy-enforced contraction. Collateral is repledged, re-hypothecated, and reused in any number of ways anyway, so what the study quoted above found is that those methods tend to increase in the wake of QE-forced removals.

These activities include (I’ll let Morgan Stanley list them for you, as it does in its 2020 annual report buried way down in the footnotes on Page 117):

The Firm receives collateral in the form of securities in connection with securities purchased under agreements to resell, securities borrowed, securities-for-securities transactions, derivative transactions, customer margin loans and securities-based lending. In many cases, the Firm is permitted to sell or repledge this collateral to secure securities sold under agreements to repurchase, to enter into securities lending and derivative transactions or for delivery to counterparties to cover short positions.

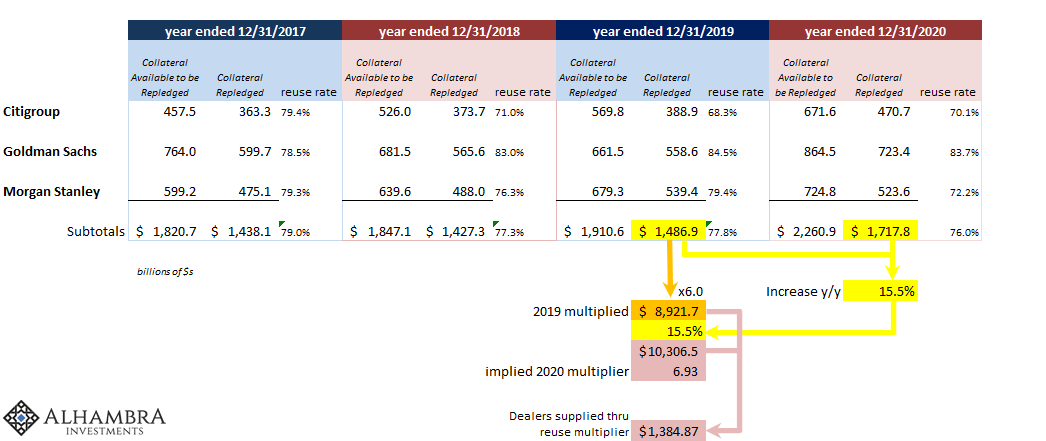

Surprising even shocking to most people, the numbers are just enormous: a/o December 31, 2020, Morgan Stanley reports $724.8 billion in collateral it has received with rights to reuse in some way, of which $523.6 billion – half a trillion – it actually did. Only Morgan Stanley.

The balances are similar across the big banks and in each case you have to go deep into the footnotes to find them.

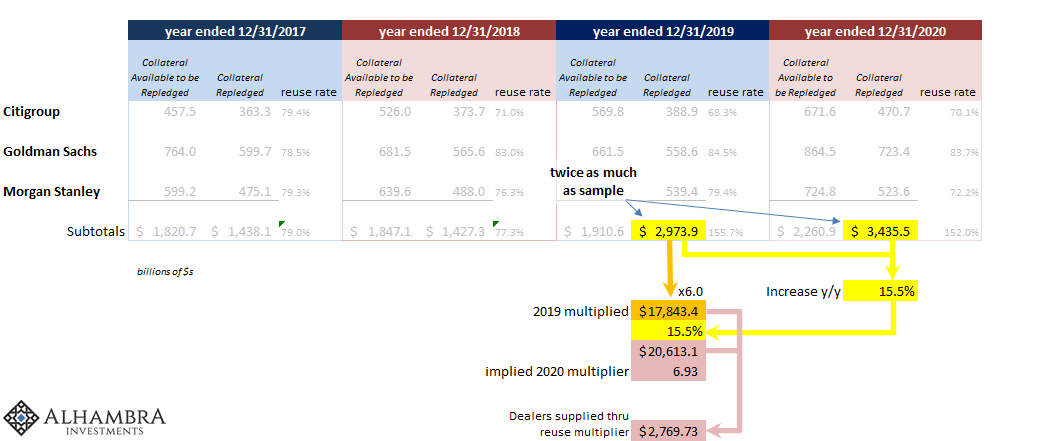

Having done so with a small sample of three, Morgan Stanley, Citi, and Goldman Sachs (the latter two chosen at random; I already had the figures from the first so it didn’t require that I go back to Edgar and look them up; sorry), I want to go through a stylized thought experiment so that we might better be able to conceptualize the answers to the above questions. This is not an attempt at accuracy or precision; on the contrary, I don’t believe such a thing is possible in our current state of data and understanding.

Even the paper’s estimates are, to me, rather uncompelling though others have found similar proportions using data and reports regular researchers such as myself could only dream of getting our hands on. In terms of reuse and repledging overall, we’re told that typically there is a collateral multiplier of somewhere between 6 or 8 depending on the data used (and time period in question).

On the contrary, those who have done it whisper that the “real” multiplier might be 20 or even higher.

We’ll start with what we do know, and that’s the collateral repledged at each of our sample firms. To begin with, none of the banks tell us much about it other than report the gross balance – we don’t even know which kind(s) of collateral they refer to. Obviously, some if not most are UST’s, but there’s definitely other types included. We just have no idea what or by how much.

What’s most interesting – and relevant – is that over the prior three years (2017, 2018, 2019) before last year (2020) these three institutions had in the aggregate reported about the same total amount of collateral repledged: a bit more than $1.4 trillion (still a staggering amount given that this survey includes only the three banks).

Suddenly, however, in 2020 the total leaps by 15.5%.

If we assume that is all UST’s (again, this is just a stylized illustration) and that the “regular” multiplier is 6, the low end of estimated ranges, this might suggest the $1.49 trillion in reused collateral by the trio in 2019 represented the starting point (or midway point) for something like $8.9 trillion throughout the entire global US$ system.

Thus, the 15.5% increase in collateral reused would equal $10.3 trillion on a like basis. Here I mean that we are going to assume the entire 2020 increase was entirely due to multiple expansion, more reused and repledging in existing collateral chains, rather than having been induced by additional collateral being posted and supplied to these firms.

Why presume no big supply change? QE, for one big reason.

Remember the paper’s estimates: for every $33 billion in additional weekly purchases by the Fed, the dealer system had to increase the collateral multiplier by around 0.5 points just to stand still – just to support the same level of repo/derivatives to make up for what the Federal Reserve unwisely took out in order to create trillions more (largely) useless bank reserves.

As you can see above – being forced to use round calendar yearly totals to match like terms with the bank reporting periods – Jay Powell’s crew went from a purchase pace of almost nothing weekly in 2019 (and it was less than nothing before not-QE introduced in October 2019) to a whopping $45.4 billion weekly rate for all of last year (obviously, the tempo changed partway through it).

Raw numbers, using our reference paper’s findings, we would expect then that the collateral multiplier might have had to increase by about 0.66 points given what the Fed reports (if $33 billion in weekly purchases means a 0.5 collateral multiplier expansion, then a $43.7 billion increase in QE weekly in 2020 would translate roughly into 0.66). Using my numbers on the table already shown above, and then below, the very simple, rough calculation I made using just these three banks was…6.93.

That’s remarkably close: starting with 6.0 then adding the 0.66 calculated using the paper’s methodology, we’d expect something like 6.66 (how appropriately evil-sounding) given the amount of QE activity during 2020.

And if we assume that the world is greater than Citi, Goldman, and Morgan Stanley, even accounting for any double counting (collateral repledged between these three) as well as other types beyond UST’s, then the absolute figures are even more astounding:

At twice the sample totals, assuming all the same proportions, this would indicate something like $2.8 trillion in collateral having been made up by this one factor alone – dealers stretching the limits of reuse and rehypothecation, being forced to adjust because the Federal Reserve isn’t really a central bank. It does bank reserves which aren’t money in the face of collateral usage which actually is.

To reiterate: this is not meant to convey any accuracy nor places too much emphasis on these specific calculations/estimates. On the contrary, I merely wanted to show that: 1. There is a reasonable basis to conclude much the same as this Fed paper, not that this is in any way solid corroborating evidence or anything more than theoretically consistent starting from real world numbers; 2. It doesn’t take much to get to huge and quick, and quite realistically that’s what is really going on in the shadows – trillions.

Tons of raw assumptions buried in the numbers above, numerous caveats all throughout. Even so, there isn’t much of a leap to see QE as the main suspect, or one of them, in why bond yields remain so low. These numbers are all huge (also giving us a sense maybe why a seemingly huge increase in depository money like M2 isn’t the whole story).

But that does not mean what everyone seems to believe, or what they are told to believe, and this is a key mistake or misinterpretation. The mainstream version is: bond buying increases bond prices, resulting in lower yields which are stimulus. All good things. The data says it isn’t bond buying directly that has any impact, but rather how removing collateral raises demand for currency-like instruments that instead raises several negative factors and conditions; harms not helps.

One of these acknowledged in last year’s paper:

These observations combined suggest that the central bank can effectively reduce the interconnectedness of the financial system by reducing the size of its balance sheet.

Get what they are saying here; if the Fed was truly interested in risks (and this being a major contributor to tight money) then it wouldn’t just opt for less bond buying, less forcing dealers to stretch already tenuous collateral chains, it would outright sell (“reducing the size of its balance sheet”) some of its holdings back to the marketplace to take out some of this serious risk introduced into the monetary system (very real potential for a bottleneck).

The negative effects on collateral availability with collateral chains stretched that much further to make up for what gets locked away in SOMA (the Fed’s reverse repo is beyond useless), it doesn’t take much imagination to figure out why dealers would pay so much for especially the best of the best collateral at auctions. And then some premium in the secondary markets.

In short, the Fed’s bond buying doesn’t lower yields, the negative impact of it buying these bonds does. One key way of forcing even more market demand (the “fleeing toward”).

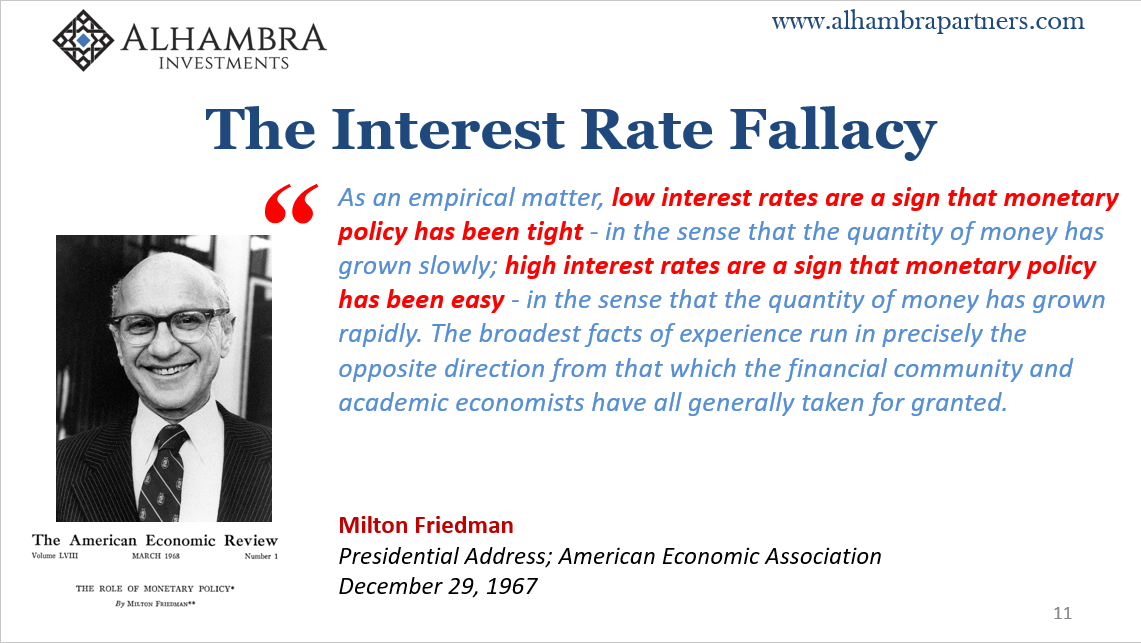

The QEnundrum, in every way consistent with the interest rate fallacy.

Stay In Touch