The first seeds of the eventual eurodollar bloom, in domestic US terms, were sown all way back in sixteen – as in the year 1916. Believe it or not, the Federal Reserve Act, then only a few years old, had been modified so that banking syndicates (those able to raise the princely sum of $1 million capital) could form what were called agreement corporations.

What was the agreement? Like the arrangement in London many years later which would make the eurodollar into all it could be (and then some), US agreement corporations would be relatively free of regulation provided that their exclusive focus and customer base didn’t include any domestic Americans or American businesses.

These were given an upgrade, kind of, in 1919 after only three such corporations were incorporated in the first three years allowed. New Jersey Senator Walter Edge proposed and sponsored yet another amendment to the Federal Reserve Act permitting what would from then forward (until the early eighties) be called Edge Act corporations; or Edges.

Not surprisingly, these didn’t catch on, either, at least not until the late fifties. There were a handful set up during that decade, according to contemporary Fed sources, which grew to 38 by 1964. Fast forward to 1976, suddenly 122 were registered (just why was there a Great Inflation, again?)

In many ways, these were pure farce; to qualify, a bank or bank holding company needed only create what were originally labeled Nassau shells (after the city in the Bahamas). Open an “office” there, or somewhere else in the Caribbean (since the islands scattered throughout the region are some fine places located pretty close to the US mainland), throw a brass plate name on the door, put a few low-level staff inside connected by direct line to HQ, and, voila, a “foreign” bank.

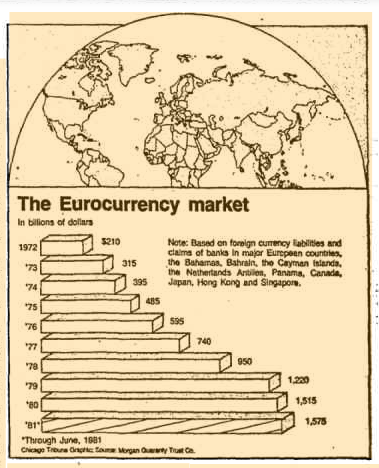

Once the shell was in place, the domestic institution could ramp up its offshore dollar activities, which by the late sixties had grown to become massive, even disruptive (for the Fed) money:

…eurodollar banks held no such restrictions and so large commercial banks ended 1968 and began 1969 with a huge deposit outflows. If that were the end of the story, the Fed might have been quite happy with the result (tightening, after all) but instead those large banks simply borrowed those deposits back from London (mostly) in the form of eurodollar liabilities. By the end of 1969, large commercial banks saw their liability balances in large CD’s decline by half, to $11 billion, while eurodollar borrowing balances grew by $13 billion (these were very large numbers for that time).

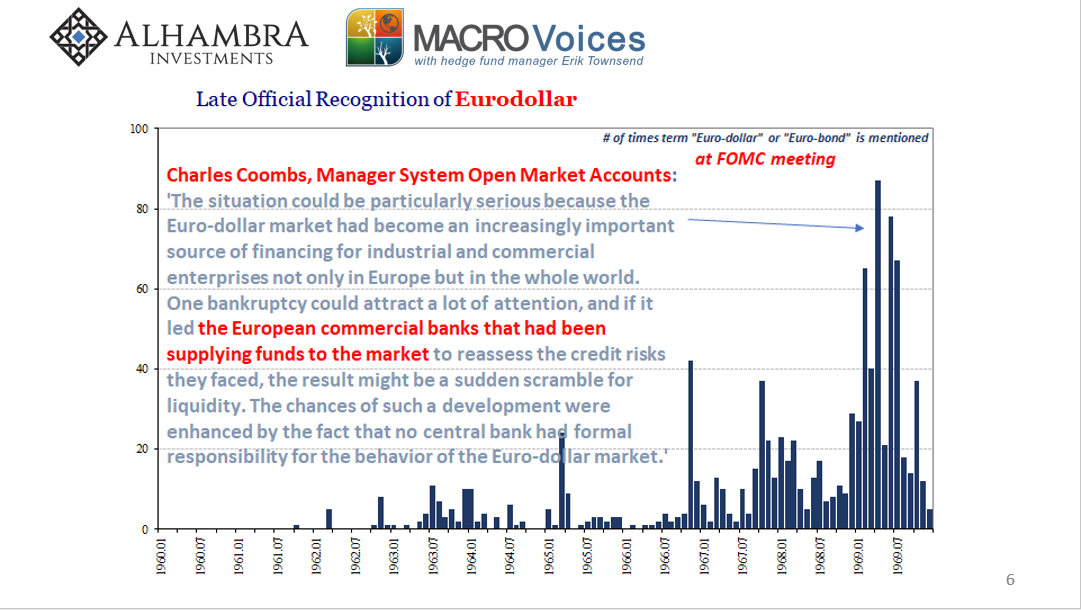

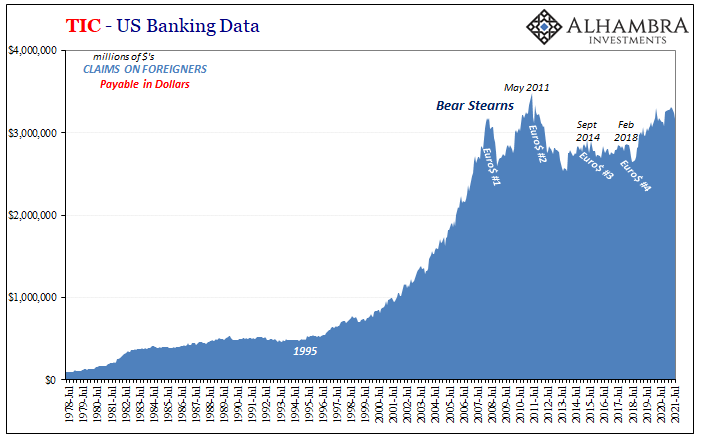

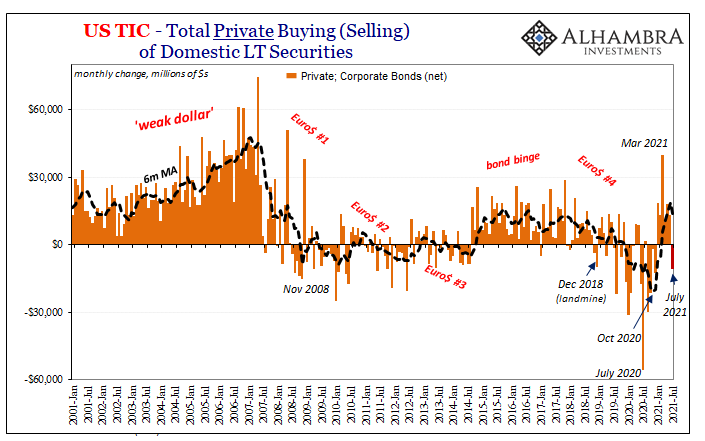

This right here specifically accounts for what you see on the chart below; officials were reluctantly forced to begin reckoning with this real money system even if a decade and a half after it first shot up:

The entire official story of the Great Inflation needs to be completely rewritten. Sadly, in large part because of the Paul Volcker Myth, a lot of good and actually honest scholarship – including much undertaken underneath the Federal Reserve’s banner – was just thrown away in the garbage and forgotten.

And not because it was bad research drawing improper or irrational conclusions; on the contrary, this stuff was discarded simply because it became dangerously inconvenient to the burgeoning (Volcker) myth of the all-powerful central bank which in reality wielding expectations policy rather than effective money. In other words, you were never told how central banks stopped being central banks.

One such researched taste from June 1975 comes from a fella named Richard Debs, who just so happened to be FRBNY’s Chief Administrative Officer at that time:

Finally, for the sake of logic, I should mention the legal framework of the Euro-dollar market, since I included the Euro-dollar market in my working definition of international banking from the point of view of the United States. However, I’m afraid that I can’t do much more than just mention it. The Euro-dollar market itself is not easily definable, and its legal framework, if any, is even less so. The market grew rapidly without the assistance, or burdens, of an integrated or even coordinated set of laws. It is an international—or multinational, or transnational—phenomenon, but it is regulated only to the extent that the Euro-dollar activities of the institutions operating in that market—the Euro-banks— are subject to regulation and supervision by the national jurisdictions in which they operate.

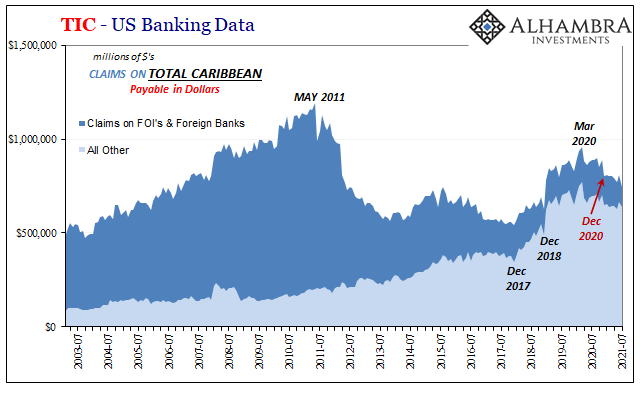

The train had been set in motion way back in 1916 but only gained serious steam when the eurodollar market itself reached a critical mass forty-some years later. While London predominated, there was always a significant eurodollar center in the far sunnier Caribbean right next door.

This only began to change after May 2011 – the devastation of Euro$ #2. In some cases, “banks” (brass plates) were relocated while many others, from what I can tell, just disappeared as operations were scaled down or shut entirely once the offshore money world realized Euro$ #1 wasn’t going to be the only one; QE’s were for the suckers.

Caribbean redistribution, however, regained some of its luster ironically during 2018’s Euro$ #4 – though the nature of this rebound remains shrouded in data discontinuity and further mystery to this day (if you’re interested, it had to do with CLO’s and repo collateral, the Treasury Department curiously, suddenly interested in island custody and the alleged weaknesses in the data collection surrounding all that).

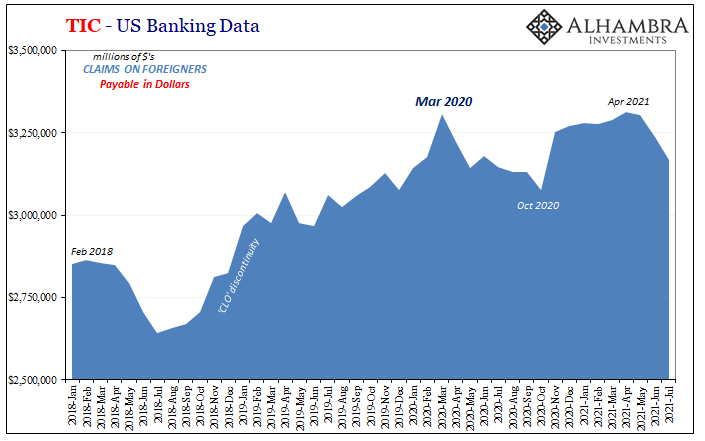

The renewed love affair with Caymans et al was short-lived (though it remains as firm as ever, from what little I can tell, for Mr. Emil Offshore Slickster). Ever since March 2020, that GFC2 for which Jay Powell can’t congratulate himself enough as to his janitor skills, again the diminishing island dollars.

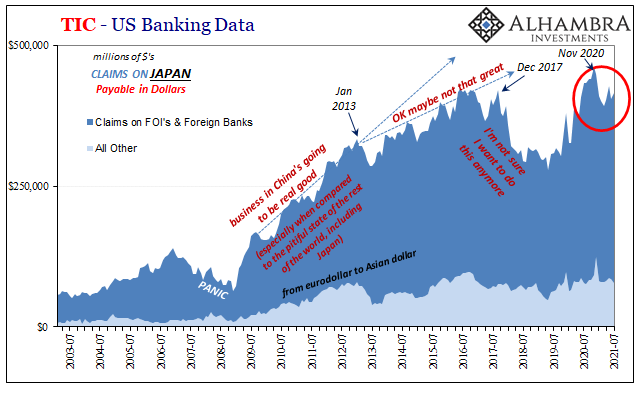

This retreat took a more determined turn back in December 2020 just as everything was ready to get going perfectly the right way. And not just Caribbean, also Japanese (another key non-European offshore dollar center).

Two considerable offshore nodes turned sharply the wrong way – just in time for the dollar to stop “crashing” early in January.

It is, oftentimes, difficult to see and appreciate these things and not just from a data (lack thereof) standpoint. For the vast majority of the public, even all these decades later: there’s stuff offshore? Huh?

This is the real legacy of Volcker (who was himself totally fooled).

As noted a few months ago, going along with the Caribbean/Japan TIC from late 2020, dollar shortage type warning signs have only escalated ever since despite reflationary then inflationary hysteria gripping pretty much the entirety of financial commentary along the way. Yes, 5% CPI’s and whatnot, but there’s a reason they likely have peaked already as well as when they may have.

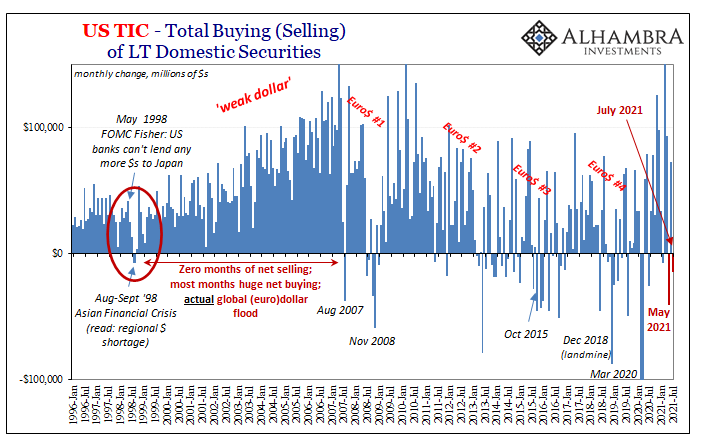

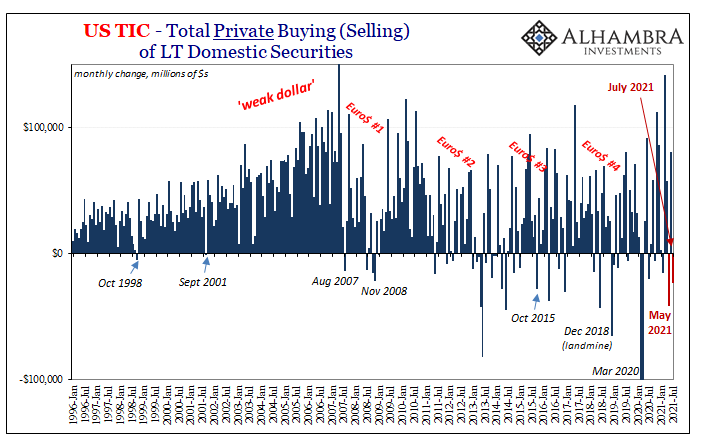

By May 2021, a rare net negative in total monthly transactions for LT US$ assets – foreigners reported to Treasury that, on net, they had sold more LT US$ assets than they had bought. This deflationary warning discussed in great detail here (the correlation is historically validated and obvious, a deep history of “selling Treasuries” that goes back to those earliest days of Bahamian brass plates).

While the net rebounded in June, I wrote last month this wasn’t unusual following a decline and didn’t really mean much unless more net buying continued forward. Instead, Treasury reported yesterday another net negative for July, making it two out of the last three:

A world actually flooded with effectively useful money (see: before August 2007) just doesn’t produce such TIC negatives, especially not regularly.

Japanese and Caribbean players suddenly get pulled back to end last year, dollar goes up, TIPS breakevens invert and then the amplified aftermath of the otherwise little trivial Fedwire. Reflation dies in the bond markets. RRP. T-bill collateral shortages and now two of the last three months (same months as when, for example, bond yields declined the most, most recently) indicating that a huge chunk of this shadowy offshore system is experiencing some kind of non-inflationary spasm.

Renewed, non-inflationary spasm.

The chain predates, obviously, delta COVID as well as any of the other mainstream excuses running around. And it fits, equally obviously, with the monetary background behind what is shaping up to be transitory price pressures, therefore not inflation.

Unfortunately, everything I’ve written up here would be shocking news to the vast majority (99.999999%) of the public who quite understandably looks at these 5% CPI’s and thinks, well, Jay Powell said he printed a ton of money. On the contrary, that’s the post-Volcker myth being stretched as far as it possibly can stretch.

It’s not what you can see which matters in these money (meaning economy) matters. It’s what you can’t, or for what don’t even know you should be looking.

Central bankers had a choice in the late seventies and early eighties: either do their job and follow the offshore money by diving headfirst down the rabbit hole to try to sort it all out; or, ignore it entirely, pretend none of this exists, and then hope by stroke of luck it won’t matter that central banks gave up on money all those decades ago.

Their luck didn’t run out in August 2007, ours did. We’re still paying – in deflationary offshore currency – for the ignorance and dereliction.

Stay In Touch