The first half of 2021 was inundated with government helicopters, more QE’s, and then CPI’s put up with guarantees the “inflation” was going to continue for a long time. Jamie Dimon, JP Morgan’s often hapless CEO, proudly declared US Treasuries beyond the touch of any 10-foot pole. With the economy on fire, he “reasoned”, who would ever want safe and liquid instruments?

The Federal Reserve, ironically, since Mr. Dimon is always on the Fed’s side, provides us with a more than partial answer. As it turned out, the US banking system was high up the list of Treasury buyers – even as those same instruments were “routed” quite famously in Q1 2021’s “historic” selloff.

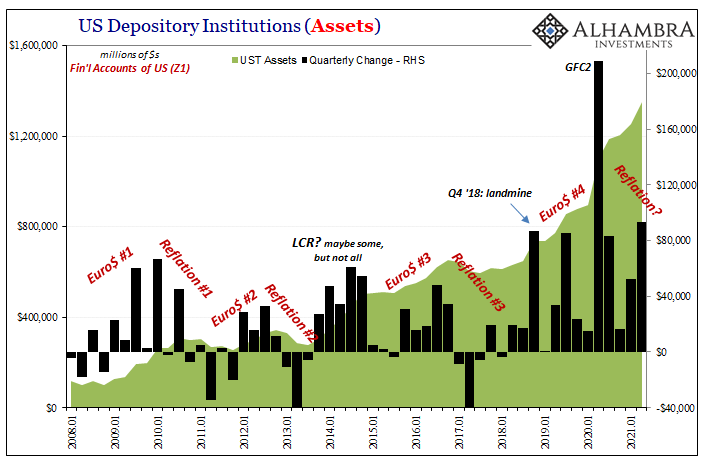

According to the Fed’s very own Z1 figures (Financial Accounts of the United States), during the first three months of the year, those most reflation consistent, depository institutions added another $52.2 billion to their already-huge holdings of the most safe, liquid securities. Before 2018 and Euro$ #4, this would’ve been among the highest quarterly increases in bank history.

Yet, the banking system outdid that the very next quarter. During Q2, they put in a further $93.4 billion. This just so happened to have been the second greatest positive quarterly change in history, behind only Q2 2020’s GFC2 aftermath!

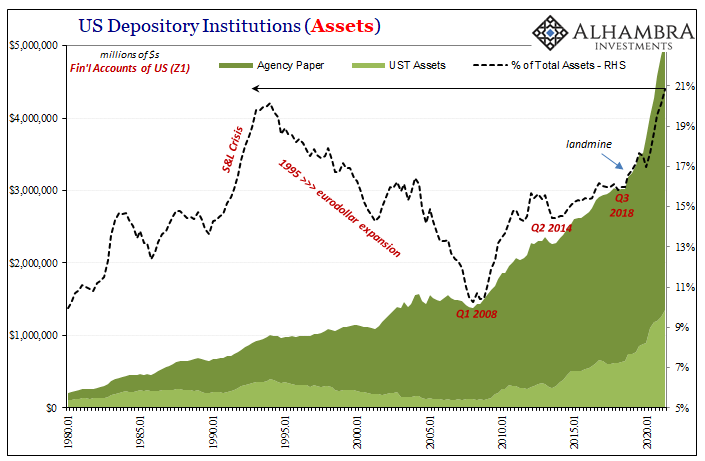

That’s not all, either. In addition to this $145.6 billion Treasury capture those momentous six months, the most hysterical inflation half-year yet, depositories also onloaded another $353.9 billion of agency debt. Yes, just barely shy of half a trillion in the safest, most liquid assets which were declared to be untouchable by all the “right” people.

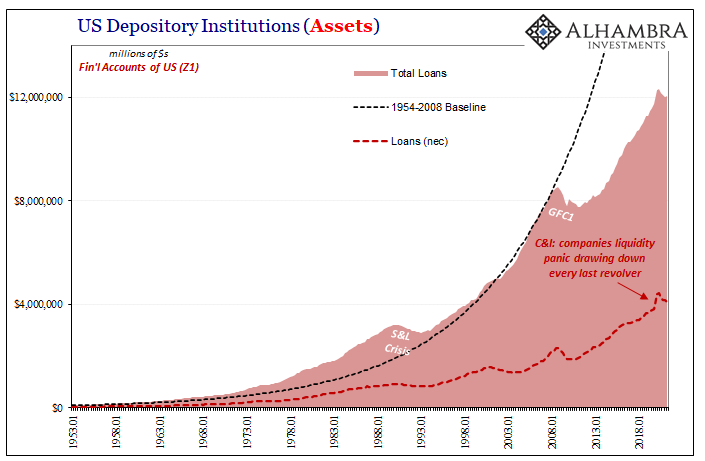

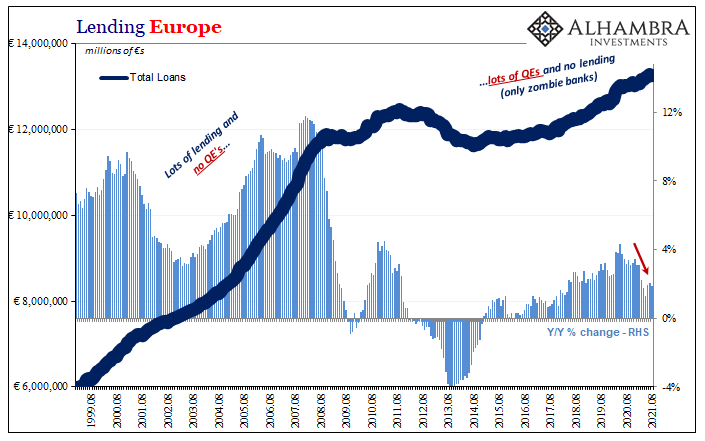

As this was being raked into bank asset portfolios, you can already guess what wasn’t. Lending declined by a further $25.5 billion, and has since last year’s corporate liquidity panic which involved drawing down every last penny of available bank revolver credit while they could.

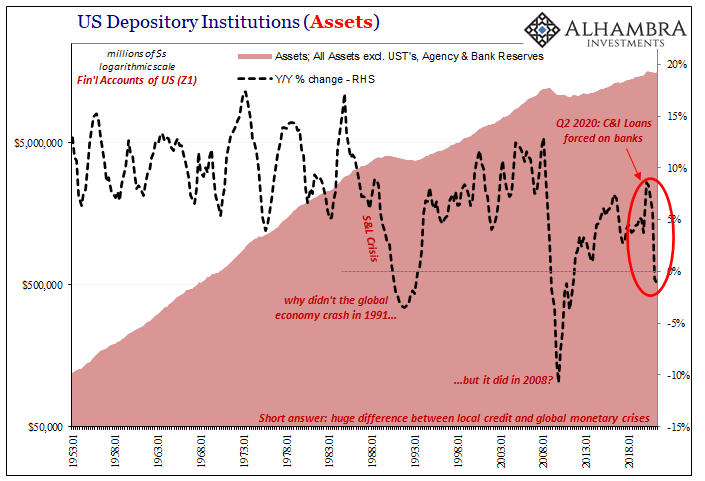

Outside of the revolvers and Treasury/GSE’s, banks are shying away from risky activities (and once more demonstrating there are no portfolio effects from QE).

The upshot is that bank assets are the safest and the most liquid they have proportionally been since…1962. On the flipside, lending is below 50% of total assets in each of the first two quarters of 2021, this for the first time since…1955.

Too many Treasuries? Not for banks (and their hedge fund offloads).

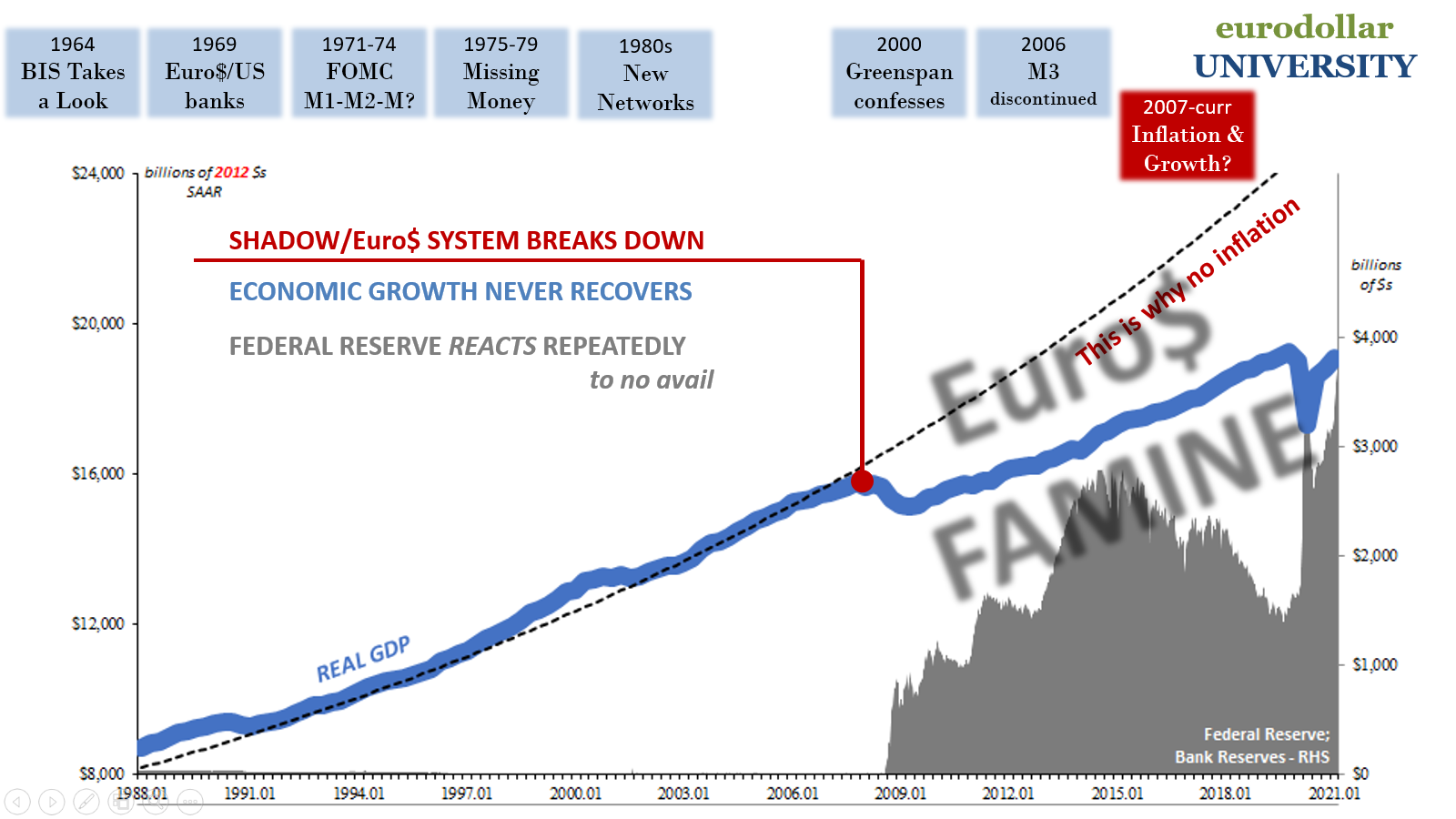

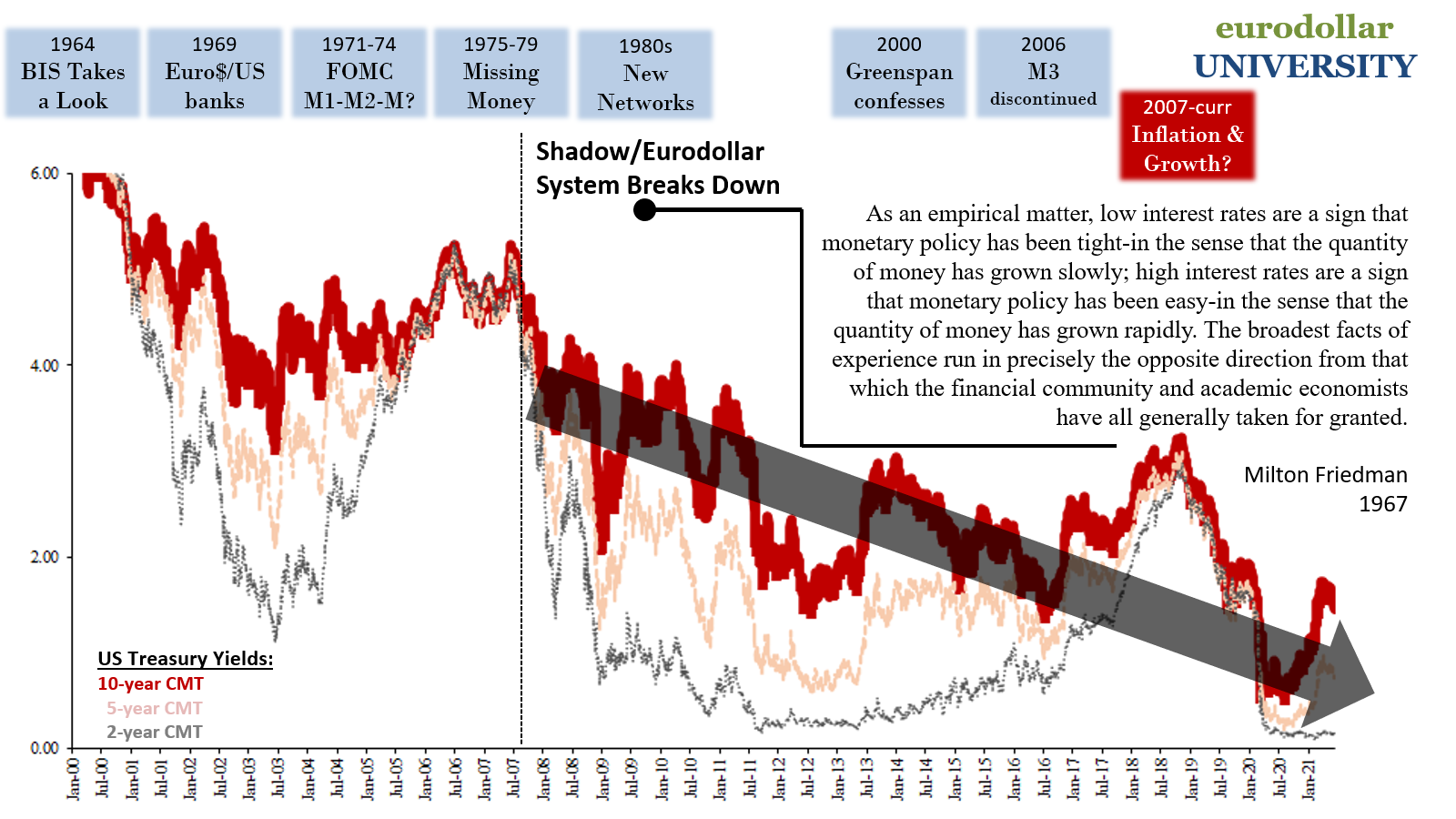

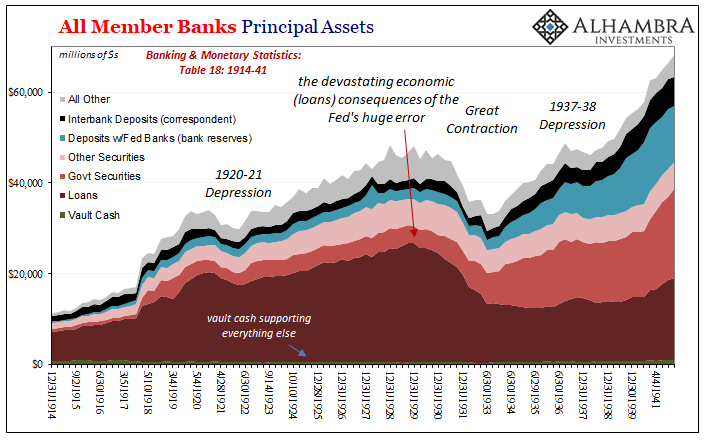

Banking was in a very different place back in the fifties and early sixties, still slowly de-risking the leftovers from the Great Depression when lending had near completely disappeared from depository actions. Like now, the depression banking system was crystal clear about its preferences and therefore identified the very problem behind money, market, and the continuous economic dysfunction and decay produced by the monetary tightness (the interest rate fallacy).

Quite simply, banks eventually shed this deflationary profile and eventually got out of the safety, high liquidity classifications and into the lending business. And it was the latter, overdone by the eurodollar’s arrival, which then led to the Great Inflation of the seventies.

The current banking profile is, obviously, nearing the same as the fifties and sixties but now heading in the opposite direction back toward the thirties. And almost certainly for the very same reasons. I’ll even let Ben Bernanke tell you what they are from his own frigid February 2010 mouth. In front of Congress, he meekly confided:

Liquidity pressures in financial markets were not limited to the United States, and intense strains in the global dollar funding markets began to spill over to U.S. markets. [emphasis added]

Subprime mortgages? Nah. The whole crisis started overseas (eurodollar), as even the former Fed Chairman was forced to acknowledge. He responded to them with TAF Auctions (which were mostly taken up by US subs of overseas banks) and ultimately useless overseas dollar swaps. Bernanke claimed, in February 2010, and still claims to this day, these were effective at “reduc[ing] stresses in global dollar funding markets.”

Yet, again February 2010, in the very next instance after calling these swaps successful he then immediately confessed:

As the financial crisis spread, the continuing pullback of private funding contributed to the illiquid and even chaotic conditions in financial markets and prompted runs on various types of financial institutions, including primary dealers and money market mutual funds.

No one seems willing to put all these simple pieces together, both to account for the first financial crisis as well as why the depository banking system ended up broken for good by all of it. I pointed this out earlier today in light of the anti-inflation Treasury/GSE buying frenzy in 2021:

From “helped to stabilize” to “as financial crisis spread” without anyone calling him on this obvious coverup. Just how effective were these swaps if what he said ended up the result anyway? This is, of course, a rhetorical question. And it is the only question for us today.

Uncertain about actual liquidity in this global dollar funding market(s), banks face no other rational choice given the ridiculously ineffective response (time and again, remember their were five QE’s just in the US before 2020) and unsuitability of bank reserves to meet actual monetary needs (including as these overseas dollar swaps).

The banking system quite naturally, as historically, shies away from the illiquid and uncertain. They don’t lend, and that’s our deflation and the whole problem.

Without lending – as during the aftermath of the Great Collapse – at best partial recovery which isn’t nearly good enough. Absent redistribution via bank intermediation, too much of the economy is left without monetary resources which then congregate in too narrow spaces; such as the bond market for government issues financing wasteful, inefficient government spending that would be better directed elsewhere but can’t be without lending.

Unless and until this all changes, and banks reverse their asset portfolios in the direction of the seventies rather than further back toward the thirties, you won’t see inflation – other than the transitory “inflation” caused by other factors like a supply shock.

And because this was all global money for global banking, de-risking continues in global banks leaving global inflation (really growth) potential also heading in the wrong direction.

When huge premiums continue to be paid for the safest and most liquid assets by the very institutions the world is counting on, and told it can count on, to do the opposite, what must this say about safety and liquidity?

Too much money? No, put that idea into the same trashcan as subprime mortgages.

Some things never change (see: abundant reserves). Global dollar markets and the Fed don’t mix, which Bernanke sort of tried to lean on as an excuse in February 2010 (why the small bit of unusual honesty). Thus, this global dollar market is one thing the Fed will never fix. Safety and liquidity all around.

Though you’ve been continuously harassed into thinking otherwise, the same goes for 2021. Worldwide.

Stay In Touch