It is a long road to recovery, an actual one, if we are to be left to the pace of economists struggling to make sense of the analog world. They are truly digital creatures, who would look at information and make no judgment until the models tell them what to think. You or I would find troubling data and seek out reasons for the trouble; an economist sees troubling data and concludes that it isn’t troubling at all if the regressions still see the same positive future. It is why despite all the downdrafts and turmoil the past two years the opinions of policymakers above all continued to reflect an economy that “should be” instead of what it clearly was.

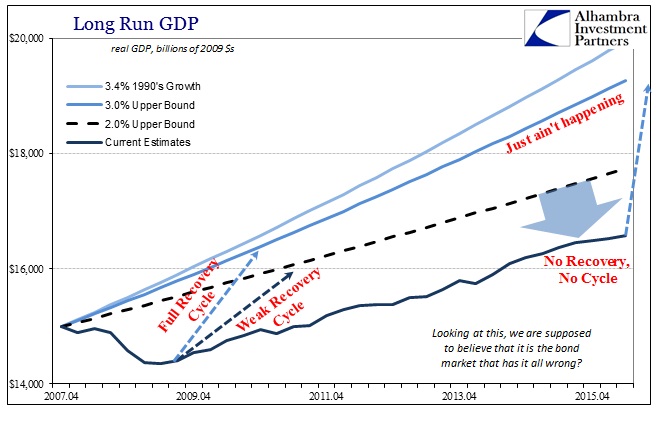

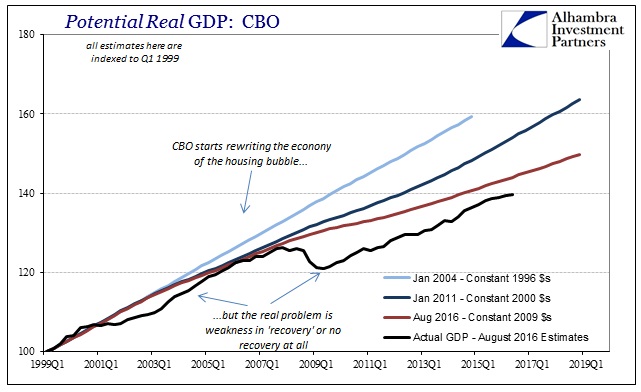

That has started to change this year because, as I showed previously, the math is being forced to reckon with inequalities. Greatest among them is the huge disparity between what is modeled of economic potential and where interest rates are now.

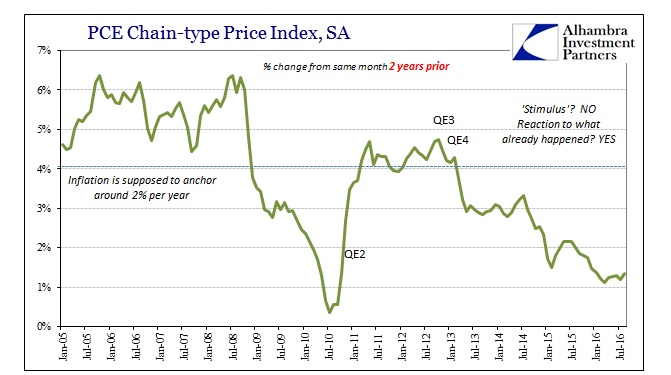

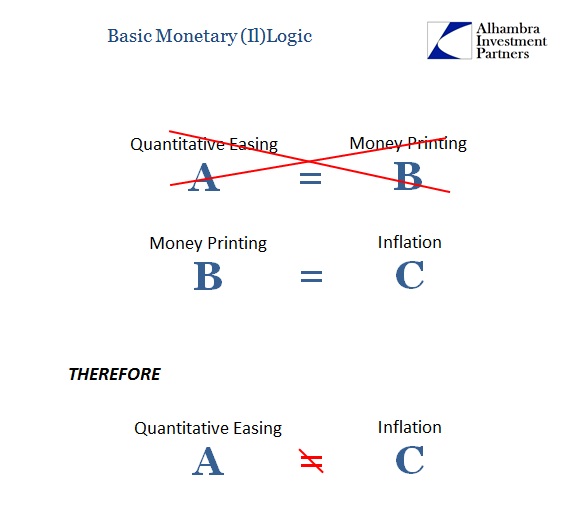

This was not supposed to happen, as the economy was thought to be long before now heading toward at least some appreciable acceleration. That it won’t for yet another year can only mean the increased likelihood that it never will (i.e., the Great Recession wasn’t a recession). The lack of inflation coincident to “never will” completes the monetary picture, including everything relating why “stimulus” isn’t.

We are finally at this late stage where the models from ferbus on out can no longer maintain any other future course except “never will.” And if the models say so, economists must recite it.

In trying to address what is truly a mammoth shortfall, they are (for now) left groping in the nonsensical. As I wrote at the outset, this is to be a long road to accountability if left politically unchanged because as Upton Sinclair once observed, “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” For Economics (capital “E”) and those who practice it, this is the literal truth; realizing that monetary policy is futile is to realize that central bankers and all the economists attached to them are just extraneous expenses.

Because of this, economists are proceeding backward if still at the slowest possible pace. They now see that the recovery is gone, and are left to justify their existence within such a hugely reduced paradigm. Not only is that perfectly contrary to everything they had promised for years (meaning they were very, very wrong about everything) they have to somehow make it seem as if there is still a role for them to play in all this – when common sense and basic logic easily dictate that you fire all the people who could possibly be so incompetent for so long even if you believe that they are finally correct.

Federal Reserve Vice Chairman Stanley Fischer, he of “very close” consistency, gave a speech earlier this month that behind all the jargon and typical economist-speak attempted exactly that. He basically contends that the Federal Reserve is still necessary to harmonize the rate at which the economy balances savings and investment. But then he states the obvious about how weak investment has been one root cause of a bleak economic future he once declared unlikely but now is forced, by his own math, to concede. Apparently we are not meant to appreciate the obvious contradiction in this new formula, for if investment has been so atrociously weak as to endanger the long run trend and the Fed is the key valve that supposedly balances investment to saving, then immediately we should question everything about the Fed in that role.

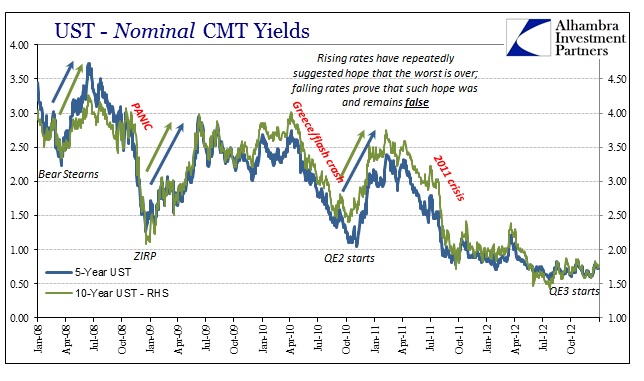

It starts with interest rates, where even Fischer now slams Beranke’s ridiculousness about them that not long ago was widely accepted among policymakers. In other words, where most still call them “stimulus” that was never the case. From Fischer’s speech:

First, and most worrying, is the possibility that low long-term interest rates are a signal that the economy’s long-run growth prospects are dim. Later, I will go into more detail on the link between economic growth and interest rates. One theme that will emerge is that depressed long-term growth prospects put sustained downward pressure on interest rates. To the extent that low long-term interest rates tell us that the outlook for economic growth is poor, all of us should be very concerned, for–as we all know–economic growth lies at the heart of our nation’s, and the world’s, future prosperity.

The fact that low interest rates are a very bad sign will come as a complete shock to almost all the media as, I suppose, to everyone who trusted economists and the media (redundant) to interpret financial factors. For year after year these people have claimed (and still do) that low interest rates are “stimulus”, but not just stimulus, the fruits of successful stimulus. Maybe “term premiums” are not all they were made out to be?

In short, the bond market was right all along that the unemployment rate was more fiction that useful. But why? Fischer claims four factors:

Among the factors affecting economic growth, gains in productivity and growth of the labor force are particularly important. Second, an increase in the average age of the population is likely pushing up household saving in the U.S. economy. Third, investment has been weak in recent years, especially given the low levels of interest rates. Fourth and finally, developments abroad, notably a slowing in the trend pace of foreign economic growth, may be affecting U.S. interest rates.

There is a whole lot of “it’s not our fault” that goes unchallenged in these word salads. Fischer’s main argument is that the Fed failed but for reasons they could not accurately project beforehand as if that would be an understandable deficit; the very short-coming of relying so heavily on statistics is that something new is but a “tail risk” that models cannot accurately predict even when they see the trends. The real problem is that all the defenses given sound plausible in the vacuum of Economics (capital “E”) that forces itself into what is really something like unnecessary reverse engineering.

As Sherlock Holmes fictionally said, once you eliminate the impossible, whatever remains, no matter how improbable, must be the truth. In 2016 Economics, it is instead that once you eliminate the obvious, whatever remains, no matter how absurd, might keep Economics relevant. Are we truly supposed to just believe that it is just one big coincidence that demographics and productivity suddenly and out of nowhere became major long run determinants (in an abruptly negative fashion) starting in 2008? Even the productivity statistics Fischer cites scream out in favor of contrary specificity:

One broad measure of business-sector productivity has risen only 1-1/4 percent per year over the past 10 years in the United States and only 1/2 percent, on average, over the past 5 years. By contrast, over the 30 years from 1976 to 2005, productivity rose a bit more than 2 percent per year.

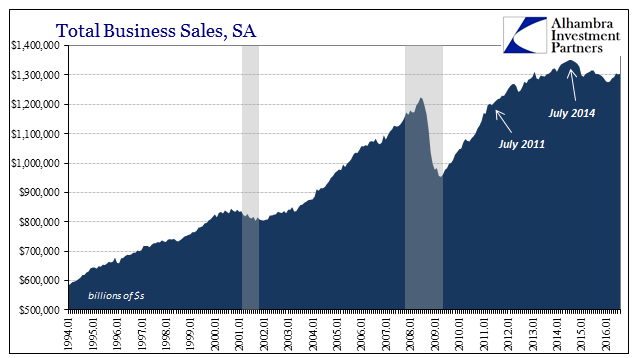

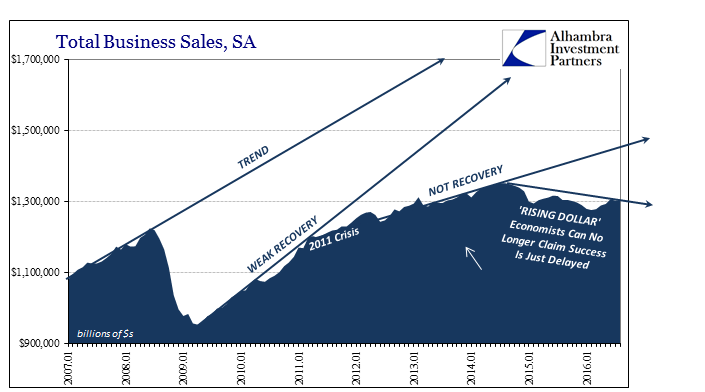

Productivity, like other broad economic accounts such as Total Business Sales, declares confidently that downward arc of increasing economic deficiency; there isn’t much doubt as to when these changes occurred. From “when” to “what” is a very short road.

Unless Baby Boomers decided in large, coordinated groups to retire in the summer of 2011 and then again in the summer of 2014, all after a much larger clutch in the summer of 2008, demographics is clearly not the reason for malaise, stagnation, or really depression. While economists were desperately downplaying the “manufacturing recession” that showed up in late 2014 as no big deal, just a “transitory” development “contained” to an unimportant 12% sector of the economy, Total Business Sales contracted and showed otherwise. Sales were $16.1 trillion in 2014, but only $15.6 trillion in 2015. Though that 2.7% decline isn’t recession, it was much more significant than that because it followed several years of obvious weakness that economists claimed had ended through the genius of QE. $15.6 trillion is not some small, irrelevant sector.

Worse, however, Total Business Sales so far in 2016 (through August) are down again, if only slightly. Adding up to $10.283 trillion in the first eight months of this year, it compares to $10.361 trillion in the eight months through August 2015. This is the reason for Fischer’s, as Yellen’s, small but important mea culpa. The economy did not liftoff, nor did it fall into recession, it only weakened in a manner that was not “transitory” but instead lingers on month after month, year after year. Not only did that end the fiction of recovery it raises much worse prospects than another single recession.

That these inflections take place at the precise moments (or at least months) where great and negative monetary changes occurred is almost too easy. From commodities to inflation to interest rates to economy, it all makes sense but to an economist it cannot because to admit the problem is money is to be out of a job. Instead, what should be easy recognition of a textbook case of “deflation” (or at least variable “disinflation”) is left to all sorts of ridiculousness; they have eliminated the perfectly logical in favor of the impossible.

It is an impediment to actual recovery because it obstructs reform in a wild goose chase of noise and gibberish. If the standing of economists is now greatly and rightly challenged by inappropriately holding to QE and ZIRP for years when it was clear it was wrong to do so, then they are wholly disqualified from what needs to come next. As I wrote in August when the Jackson Hole gathering practically announced all this absurd angst, this is but the first step and it really should be the final one that economists of their current persuasion are allowed to take.

There is a world waiting to be rebuilt and a growing realization from even the most recalcitrant orthodoxists, those stubborn elite who denied all this for decades, that such a job is going to get done. We are moving past “if” and finally toward “when.” They are not interested in litigating past liability, only ensuring that they have a voice in that outcome. That should never happen; they had their chance, squandered it, and proved themselves unfit for the huge task ahead that was left to us by nothing more than Lord Acton’s axiom about power corrupting. A republican democracy needs no such people in positions of influence. They couldn’t be trusted to do what was right, and now we are left still to tally the costs of such blatant immorality.

If Fischer had given this speech in 2009 or even 2012, maybe that would have shown some small hope that Economists were capable of something other than religious devotion to Economic ideology (especially through econometrics). In reality, however, economists disqualified themselves decades ago. The time for this monetary debate was at the latest June 2003, if not 1993 or really1968.

Welcome again to Keynes’ long run, where intellectually stunted economists take a decade of sneering at the ungrateful public in order to eventually join in their destabilizing frustration anyway. They really don’t know what they are doing; they never did. It is no small comfort that they are just now after wasting so much unthinkable time and economy starting to admit it. It isn’t the only problem, of course, but it is a primary one that the world’s monetary authorities don’t know a thing about money.

Stay In Touch